TODAY’S S&P 500 SET-UP – January 23, 2013

As we look at today's setup for the S&P 500, the range is 21 points or 1.18% downside to 1475 and 0.23% upside to 1496.

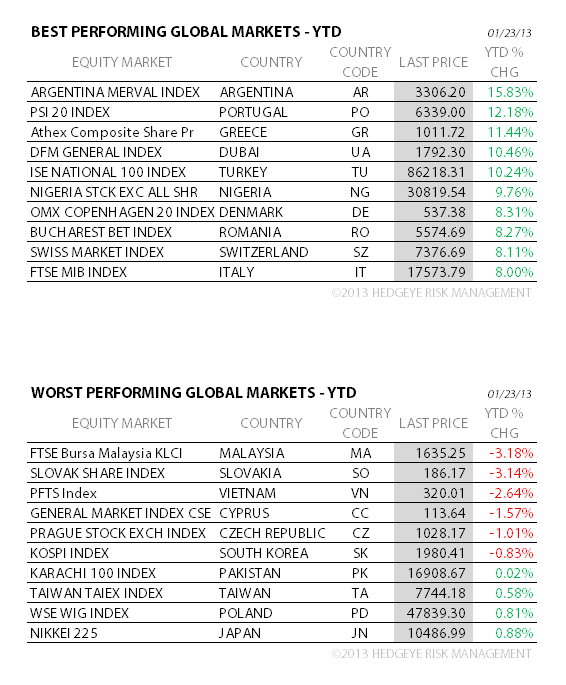

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.60 from 1.60

- VIX closed at 12.43 1 day percent change of -0.24%

MACRO DATA POINTS (Bloomberg Estimates):

- 7am: MBA Mortgage Applications (prior 15.2%)

- 7:45am: ICSC/Goldman weekly sales

- 8:55am: Johnson/Redbook weekly sales

- 9am: FHFA House Price Index MoM Nov. est. 0.7% (prior 0.5%)

- 9:45am: Revision of Chicago Purchasing Managers Index

- 10am: IMF releases World Economic Outlook update

- 11am: U.S. to purchase $1.25b-$1.75b notes

- 11:30am: U.S. to sell $30b 4-week bills

- 4:30pm: API energy inventories

GOVERNMENT:

- IMF issues update to 2013 World Economic Outlook, 10am

- Congressional Gun Violence Prevention Task Force holds

- meeting, 1pm

- Sec. of State Clinton testifies on Benghazi before Senate

- Foreign Relations, 9am; House Foreign Affairs, 2pm

- ITC scheduled to announce decision to uphold/review a trade

- judge’s finding that Samsung infringed on 4 Apple patents, 5pm

WHAT TO WATCH

- Apple reports earnings after close; 47.8m iPhones expected

- Allergan to buy Map Pharma for $958 million in cash

- Google profit tops ests. on year-end advertising gains

- IBM 2013 EPS beats estimates as software boosts profit

- Texas Instruments forecasts sales that miss some estimates

- McDonald’s qtr global comp sales may drop; first since 2003

- Siemens profit beats estimates on energy, health-care units

- Unilever sales growth beats estimates on emerging markets

- Draghi says ‘Darkest Clouds’ over euro area have lifted

- Netanyahu vows broad coalition as Lapid surprises in vote

- U.K.’s Cameron promises to hold referendum on EU by 2017

- U.S. budget discord is top threat to global economy: poll

- Microsoft said to weigh Dell investment in buyout

- World Economic Forum in Davos continues

EARNINGS:

- Wellpoint (WLP) 6:00am, $0.94

- Air Products & Chemicals (APD) 6:00am, $1.29

- Baker Hughes (BHI) 6:00am, $0.61

- TE Connectivity (TEL) 6:00am, $0.64

- Praxair (PX) 6:05am, $1.38

- Textron (TXT) 6:30am, $0.56

- Quest Diagnostics (DGX) 6:30am, $1.04

- Coach (COH) 7:00am, $1.29

- Motorola Solutions (MSI) 7:00am, $1.02

- United Technologies (UTX) 7:00am, $1.03

- RPC (RES) 7:15am, $0.25

- Rollins (ROL) 7:30am, $0.17

- First Niagara Financial (FNFG) 7:30am, $0.18

- Molex (MOLX) 7:30am, $0.39

- St Jude Medical (STJ) 7:30am, $0.89

- Allegheny Technologies (ATI) 7:35am, $0.15

- Abbott Laboratories (ABT) 7:44am, $0.46

- McDonald’s (MCD) 7:58am, $1.33

- US Airways Group (LCC) 8:00am, $0.19

- General Dynamics (GD) Pre-Mkt, $1.89

- Texas Capital Bancshares (TCBI) 4:00pm, $0.83

- Bancorp South (BXS) 4:00pm, $0.24

- RLI (RLI) 4:00pm, $0.45

- Swift Transportation (SWFT) 4:00pm, $0.26

- Cubist Pharmaceuticals (CBST) 4:00pm, $0.48

- Stryker (SYK) 4:00pm, $1.13

- Varian Medical Systems (VAR) 4:00pm, $0.87

- Greenhill & Co (GHL) 4:01pm, $0.72

- Amgen (AMGN) 4:01pm, $1.38

- Crown Castle International (CCI) 4:01pm, $0.13

- LSI (LSI) 4:01pm, $0.14

- Hexcel (HXL) 4:03pm, $0.38

- Umpqua Holdings (UMPQ) 4:05pm, $0.23

- InvenSense (INVN) 4:05pm, $0.17

- Polycom (PLCM) 4:05pm, $0.15

- F5 Networks (FFIV) 4:05pm, $1.15

- Netflix (NFLX) 4:05pm, $(0.13)

- SanDisk (SNDK) 4:05pm, $0.75

- Symantec (SYMC) 4:05pm, $0.38

- Lam Research (LRCX) 4:05pm, $0.44

- United Rentals (URI) 4:15pm, $1.05

- Altera (ALTR) 4:15pm, $0.39

- Western Digital (WDC) 4:15pm, $1.82

- Raymond James (RJF) 4:19pm, $0.67

- Cathay General Bancorp (CATY) 4:30pm, $0.33

- Cohen & Steers (CNS) 4:30pm, $0.42

- Susquehanna Bancshares (SUSQ) 4:30pm, $0.23

- Apple (AAPL) 4:30pm, $13.56

- FNB /PA (FNB) 4:35pm, $0.21

- East West Bancorp (EWBC) 4:45pm, $0.48

- Hill-Rom Holdings (HRC) 5:00pm, $0.44

- Noble (NE) 5:00pm, $0.67

- Parametric Technology (PMTC) 5:25pm, $0.33

- Teradyne (TER) 6:00pm, $0.01

- Jacobs Engineering (JEC) Late PM, $0.75

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

OIL – Both Brent and WTIC have re-captured their respective long-term TAIL risk lines of $92.04 and $111.48 support. There’s as important a difference b/t global growth slowing and stabilizing as there is stabilizing and accelerating – and it’s real tough to see consumption accelerate if food/oil prices reflate (from here); something to noodle over w/ Energy (XLE) +6.7% YTD.

- Gold Near One-Month High Before Lawmakers Vote on Debt Ceiling

- Leon Black Follows Denham in Buyout Firm Mine Push: Commodities

- Physical Gold Purchases Seen by Standard Bank as Unusually High

- Copper Trades Near One-Week High Before U.S. Debt-Ceiling Vote

- Oil Trades Near Four-Month High Before Vote on U.S. Debt Ceiling

- Soybeans Gain as Brazil Dryness May Cut Crop Amid Rising Demand

- Rice Exports From Thailand Drop to Decade Low, Losing Top Spot

- Cocoa Swings as Ivory Coast’s Crop Spared Damage; Coffee Gains

- Galena Energy Hedge Fund Chief Lixi Said to Leave Company

- Algeria Attack No Outlier as Oil Targeted 3 Times a Week: Energy

- Chile Billionaires Propel CSAV to First From Worst: Freight

- Traders Plan Gasoline, Diesel Freight Swaps as U.S. Drives Rally

- Rubber Drops for Third Day as Delayed Stimulus May Curb Demand

- Rebar Futures Rise for Second Day on Optimism Demand to Improve

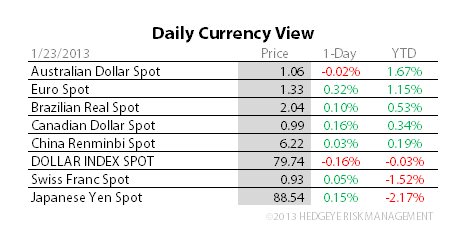

CURRENCIES

EUROPEAN MARKETS

RUSSIA - +0.8% leads European majors this morning and is more of the same on the reflation point. Treasury Bond Yields don’t like Oil ripping either, down a few bps d/d to 1.84%. Always interesting to study macro moves on the margin.

ASIAN MARKETS

KOSPI – a leading indicator in our model works both ways and its interesting that the KOSPI (down -0.81% last night) just broke my immediate-term TRADE line (1985) out of nowhere (despite “Tech” news being solid after the US close). Nikkei punishing the Johnny come lately consensus crowd who came into the short Yen/long Nikkei trade late, down -2.1% through 10,733 TRADE support.

MIDDLE EAST

The Hedgeye Macro Team