“What if this is as good as is gets?”

-Melvin Udall

That’s what Jack Nicholson asked a bunch of depressed psychiatric patients in one of the great scenes in American comedy (As Good As It Gets, 1997). Melvin Udall should be re-casted as a modern day money manager.

Obsessive-compulsive about this market, anyone?

Back to the Global Macro Grind…

I don’t yet require psychiatric help, but with each passing day I am feeling more and more like a shrink. “Keith, do you really think growth is stabilizing?”… “This market can’t go higher with all this debt, can it?”…

Trust me, it goes on and on and on. I don’t get up at this hour every day to not tell you what I think. The last 2 months have been nothing short of fantastic for stocks – and, this time, the global growth fundamentals actually supported it.

Everything has a time and price. So the question remains, with the SP500 up double digits (+10.2%) now from where you could have bought just about anything lower (November 15th, 2012), is this as good as it gets?

Let’s start with Global Growth… “I’ve got a really great compliment for you, and it’s true.” –Melvin

- ASIA – high frequency growth data has been stabilizing for 3 months

- EUROPE – high frequency growth data stopped slowing in November

- USA – employment growth has been stabilizing for 3 months and Housing is ripping

What about inflation?

- ASIA – most CPI and PPI readings were relatively benign in October-December, but should pop up in January

- EUROPE - since they are still dealing with stagflation, it’s all relative, but Brent Oil was cheaper in November

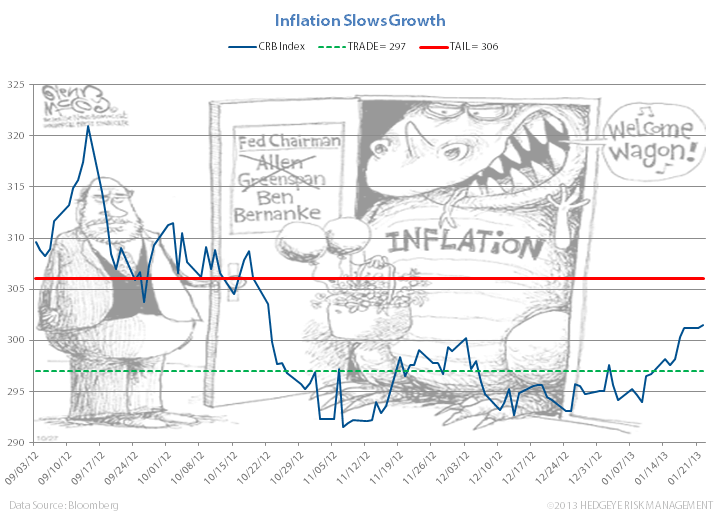

- USA – follow the CRB Index - down hard from SEP to NOV, heading higher, faster, now in January = #headwind

So, if policy perpetuated Inflation Slows Growth… and Food/Energy prices continue higher from here until whenever that whenever is, you have yourself the 1st major macro headwind to growth in the last 2-3 months.

If you think you are going to get sustainable (real inflation adjusted) economic growth with $115-130 Brent Oil, you might want to check the tapes on how that consumption growth movie ends.

Isn’t it appropriate and ironic, then, as our bailed-out overlords descend upon Davos this week, that the manic media no longer looks to broken sources for “growth forecasts.” They’ve enlisted JP Morgan’s Jaime Dimon this morning instead. He doesn’t have a macro model but is insinuating that the “foundation is set for 4% growth.”

Right, right…

To be clear, there’s a better chance that hockey is banned in Thunder Bay, Ontario than the USA seeing a sustained 4% GDP growth rate when Oil is above $100/barrel.

To Review: there are 3 stages of growth and inflation in our GIP (Growth/Inflation/Policy) Macro Economic Model:

- Slowing

- Stabilizing

- Accelerating

You don’t have to be a brain surgeon to get Muckernomics – it’s all about time and space. Try it on skates (or with a car) and you’ll get it. Cycles are processes, not points. And there are certain levels of inflation that slow growth inasmuch as there are others that help stabilize it (see our Chart of The Day).

Accepting this as truth would eviscerate the academic credentials of most Keynesians hanging out on your tax-payer dollars in Switzerland this week. Central planners of the Global Currency War still think that if you debauch the Dollar, you’ll see a meteoric rise in export demand (even though exports are only 9% of the US economy, and falling).

Back to Melvin’s Market… higher-highs (and in the case of the Russell2000, all-time highs) are flat out bullish, until they aren’t. If your catalyst shorting this market was Earnings Season, so far that’s what we call being wrong. The Financials led off with borderline excellent results, and now we’re seeing Tech (the market’s worst performer YTD at +2.15%) deliver some early morning bacon.

Since Apple (AAPL) is 17% of Tech (as a % of the Tech ETF, XLK), what it does tomorrow on earnings day really matters; especially after Google (GOOG) and IBM ripped last night in the post. Our quantitative signal on AAPL says to do nothing. It’s still in a Bearish Formation (bearish on all 3 of our risk management durations, TRADE/TREND/TAIL), so waiting and watching for the print is a choice.

In the meantime, the SP500 is immediate-term TRADE overbought at 1496 inasmuch as the VIX is oversold at 12.19. So a big AAPL surprise to the upside might just give you what Melvin called his last word, “freak” – to the upside. And if they miss, people might just freak-out on that too.

If you think this market is crazy, join the club. There hasn’t been anything normal about this for years. Not seeing growth stabilizing when it did might be as crazy as buying is on green is crazy today or tomorrow.

“Sell crazy someplace else, we're all stocked up here.” –Melvin Udall.

Our immediate-term Risk Ranges for Gold, Oil (Brent), US Dollar, EUR/USD, USD/YEN, UST10yr Yield, AAPL, and the SP500 are now $1, $110.93-112.95 (Bullish Breakout for Oil), $79.41-80.14, $1.32-1.34, 87.71-90.61, 1.82-1.91%, $482-528, and 1, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer