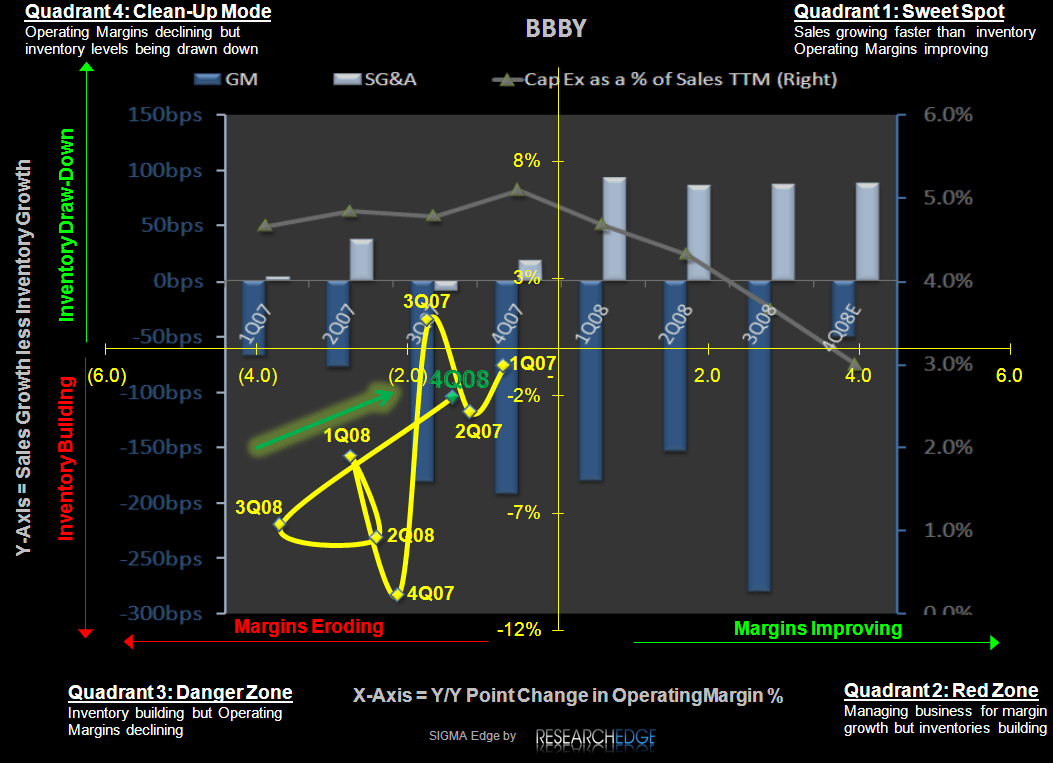

Great quarter from one of our favorite names - Bed, Bath and Beyond, which crushed my above-consensus estimate by over 15%. The SIGMA chart below speaks a thousand words here. We're seeing both inventory/sales spread get more favorable while gross margins are coming in ahead of expectations. With compares for the upcomming few quarters increasingly easy and the trajectory looking good, I continue to like this one.

Rather than go on about the merits of BBBY's quarter, I want to hit on a few thematic notes, as well as company-specific divergences within the Home Furnishings space.

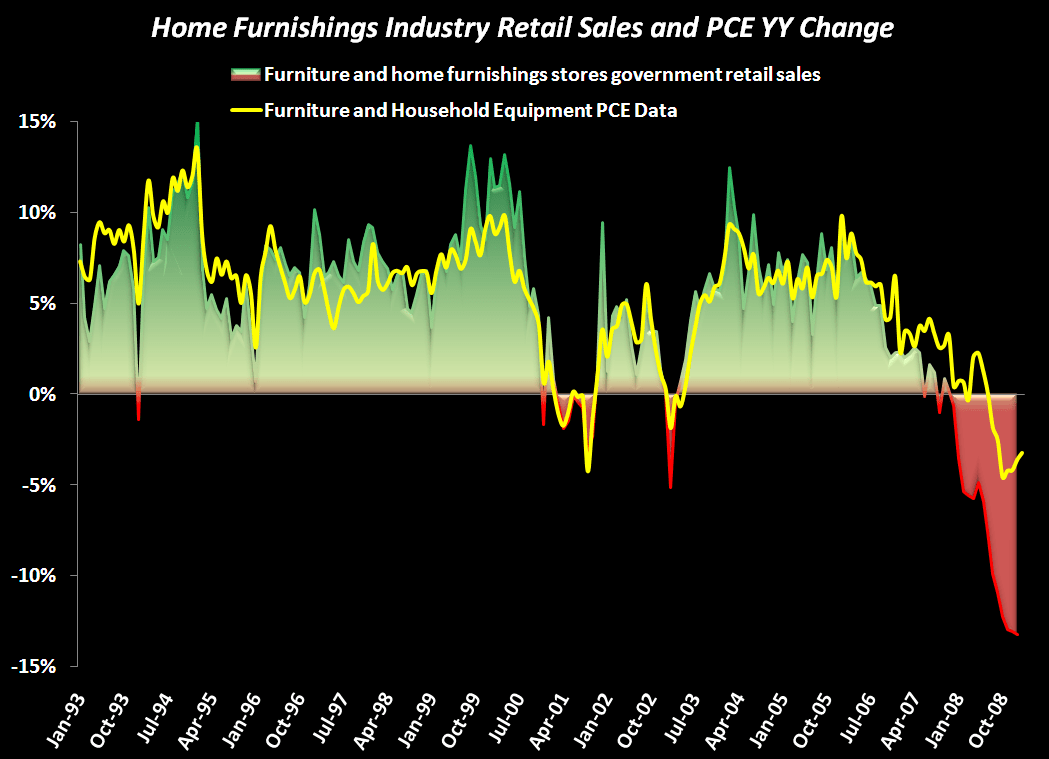

Looking at retail sales and personal consumption, we're seeing a positive inflection point in each (keep in mind that ‘less bad' is good in our model). There is a bullish call to be made in this space based on the emerging macro-economic trend of employment turning and a housing bottom. No, we're not saying you should run out and buy Toll Bros. Quite the opposite, actually. We like companies that will benefit from consumers staying put in their existing homes, with plans of doing so for a while. That usually means sprucing up one's home, and catching up on deferred capex.

Who will capitalize? If you listened to any conference calls on the fourth quarter, you heard some good mixed with the bad on the home furnishings front. JC Penny, Williams-Sonoma, and Wal-Mart mentioned the increased time spent at home eating and entertaining as a cause for less bad home furnishing sales. Then others like Target (that can't seem to get out of its own way) highlighted the risks they face as well as the efforts they are taking to consolidate SKUs to fix the business. .

Here's an overview of what different management teams had to say about the home furnishings space this quarter.

"There is one major behavior change we have seen during the past year that has had a significant impact on our home business. Families are definitely eating more often at home. While we expect this to have a positive impact on grocery, we also have seen increased comps in home categories for cooking, dining and entertaining at home," Eduardo Castro-Wright - WMT Vice Chairman - Q4 CC.

"From a merchandising perspective, we had negative growth in all key categories, although bakeware, electrics and cookware were less pronounced. Exclusivity and perceived investment value continued to drive these categories as people are eating out less and entertaining at home more," Dave DeMattei - WSM Group President - Q4 CC.

"Another bright spot was our home business that has experienced stability over the last few months," Ken Hicks - JCP President, COO - Q4 CC.

"We're seeing a little bit of life in the home business as we start the spring season. I think that may be the bottoming effect of home furnishings over the last two or three years. We may be seeing a better trend going forward. Although until the housing crisis is more or less fixed on a macro basis, it's going to be hard to see great increases," Mike Ullman - JCP CEO - Q4 CC.

"In our retail segment our results were characterized by a fundamental change in consumer spending patterns that negatively impacted both our traffic and sales, particularly in higher margin discretionary categories like seasonal, apparel and home," Gregg W. Steinhafel- TGT CEO - Q4 CC.

"On the highly discretionary side in home and [...] we're looking at mid double digit comp decreases [for 2009]. We are very conservative in apparel, home and seasonal categories where there is significant markdown risk," Gregg W. Steinhafel- TGT CEO - Q4 CC.

Zach Brown