Kimberly-Clark (KMB) is set to report earnings on January 25th, and while it isn’t our thing to preview earnings, we think the timing of the KMB and PG earnings releases (also scheduled for the 25th) makes for an interesting short duration pair – long PG/short KMB.

KMB on the short side

KMB will report Q4 2012 EPS and provide an initial look at 2013 EPS – consensus for Q4 is $1.36 (we are modeling $1.34), bringing the full year 2012 EPS result to $5.23 versus company guidance of $5.15 to $5.25. We see more risk to the $1.36 than upside. The company will likely provide 2013 guidance consistent with its longer-term goal of EPS growth in the mid-to-high single digit range. For reference, 2011 vs. 2010 was 6.3% EPS growth at the mid-point, while 2012 vs. 2011 was 5.7% growth. Consensus for 2013 ($5.59) already contemplates 6.9% growth, so we don’t think a short position gets hurt with guidance.

Further, at 15.5x ’13 consensus, we don’t see much upside to the multiple, given our view of the company as a 3-4% top line grower.

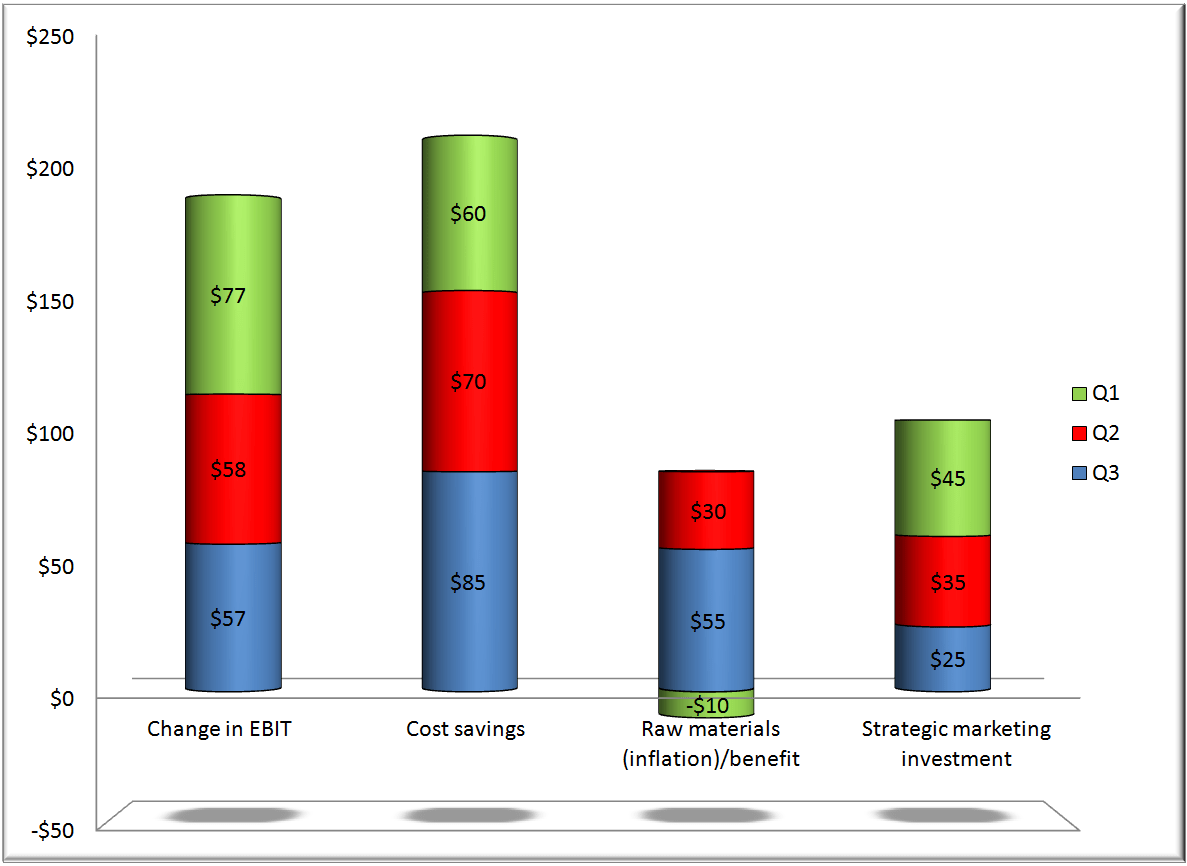

We believe that the quality of KMB’s earnings have declined through 2012. In Q1, $77 million of year over year EBIT gains were driven by cost saves ($60 million) and hurt by $10 million of input cost inflation, so operations accounted for $27 million of the year over year EBIT gains. KMB reinvested $45 million in strategic marketing. In Q2 and Q3, year over year EBIT gains slowed while cost savings increased and raw materials moved from a headwind to a tailwind and strategic marketing investments slowed. As we move into 2013, raw materials appear to be set to move from a tailwind to a headwind once again.

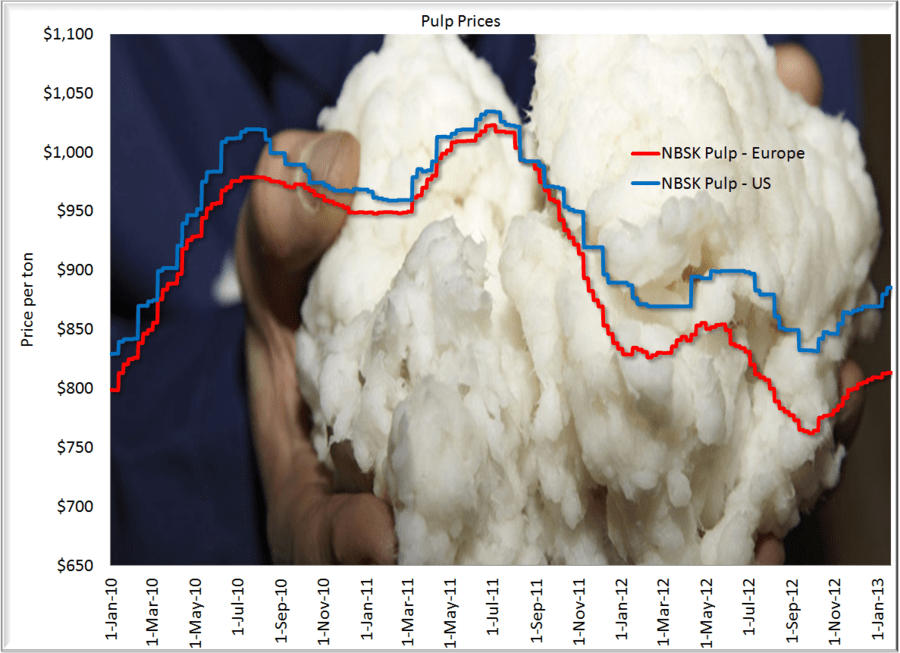

Finally, the key commodities of crude and pulp have moved against the company over the last quarter of 2012. Now, the company does have some flexibility year over year as we have seen increases in the strategic marketing spend through the first three quarters of 2012 (+$45 million in Q1, +$35 million in Q2 and +$25 million in Q3). However, we are of the opinion that the company has seen its multiple expand precisely because it has increased investment and any reversal of that trend is unlikely to be greeted kindly by the market.

PG on the long side

PG will report Q2 EPS on Friday, with consensus looking for $1.11 versus a guidance range of $1.07 to $1.13 - the growth versus 2012 is not heroic at all, with core EPS in the year ago quarter at $1.09. Our estimate is $1.13 and we can model an increase to the full-year guide as well. Our experience is that names that beat and raise go higher, particularly in the case of mult-year laggards such as PG.

While top-line trends at PG have been lackluster, the company has significant income statement flexibility from its restructuring program. EPS stability sans top line momentum isn't likely to garner multiple expansion, but we at least have some comfort that the earnings base can be sustained while we wait to see what materializes on the top line for PG. We may be waiting for Godot, but we don't think we are paying a substantial premium for the show.

PG's valuation isn't particularly compelling to us (16.9x calendar '13), but we think the name can be defended lower if our math happens to be wrong (just as we think investors can stick with the KMB short if Friday doesn't emerge as a catalyst).

Have a good week.

Rob

Robert Campagnino

Managing Director

HEDGEYE RISK MANAGEMENT, LLC