“The time had come for the Anglo-Americans to fight; to not fight was to lose the war…”

-William Manchester, The Last Lion

In the summer of 1942, Hitler “finally moved fourteen divisions against Sevastopol… and took the city in twenty-three days.” Since Sevastopol was the “largest Soviet naval fortress on the Black Sea” (The Last Lion, pg 546), this mattered to the Americans, big time.

Big is as big does, and the world’s Currency War (Rickards) is getting big. While I am not trying to equate the human devastation of WWII with what’s being driven by economic central planners today, I think it’s fair to use historical metaphors that draw on global conflict. In today’s case, every country’s politicians are fighting for themselves.

Whether these academic bureaucrats want to admit the scope of their experimentation or not, Keynesian Policies To Inflate via sovereign Currency Debauchery are both causal in their intentions and correlated in their impacts on real-time market prices.

Back to the Global Macro Grind…

This morning I woke up to one of those aha moments where the German enemy was on the ground (snow in CT) and the Russians were coming. Well, sort of. I actually love all types of snow, other than the yellow kind.

What the Italians and Russians don’t like is their currency going straight up into the right. South Koreans don’t like it either. Maybe the only country that loves it is Canada – maybe that’s because they are one of the few that recognizes it as winning.

Russian Central Bank First Deputy Chairman (fancy titles over there), Alexei Ulyukayev, explicitly called this a “Currency War” today in Moscow and went on to add that “Japan is weakening the Yen and other countries may follow.”

Ya think?

This isn’t new. It’s going to be a new global consensus however. And I think that’s what makes 2013 as exciting (and trade-able) a year as I can remember. If you don’t have a multi-factor process that incorporates countries, currencies, policies, etc. built into your process however, you might think I am right out to lunch.

Well, if you trade currencies and bonds like you trade stocks, your lunch might get eaten too. These markets are much more glacial than the high-frequency insider trading networks that have developed in small cap equities. Maybe that’s why some of the largest macro hedge fund gurus have retired. The Global Macro game of risk doesn’t really have the inside trade anymore.

When it comes to leveling the playing field and democratizing access to market edge that is legal, I am all in. What is your edge today isn’t what it was 5, 10, and 30 years ago. I think today’s market edges live and breathe at the intersection of Behavioral Economics and Chaos Theory (math).

How do we risk manage this?

- The process starts and ends with Embracing Uncertainty – anything can happen, literally, any hour of the day

- We let the signal (market price/volume/volatility) tell us where to swing at high probability pitches

- We then either confirm or disconfirm the quantitative signal amidst #OldWall’s qualitative research noise

Any hour of the day? Yes, of course. If you have half of America begging for centrally-planned markets, what kind of market do you expect? So don’t whine about it – understand it, and play the game that’s in front of you.

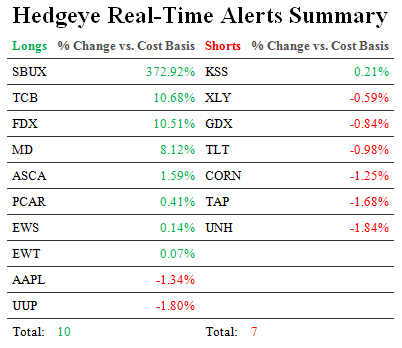

Yesterday’s intraday signal (on the selloff to the lowest intraday price we have seen in a week) was to cover shorts and buy Best Ideas on the long side. So this is what we did on the cover/buy front:

- We bought Apple (AAPL) at immediate-term TRADE oversold

- We covered Metals (XME) at immediate-term TRADE oversold

- We covered Phillip Morris (PM) at immediate-term TRADE oversold

- We bought Singapore (EWS) at immediate-term TRADE oversold

That doesn’t mean we love Apple (AAPL) long-term here (see chart). It just means what it means – we are at war with consensus and our quantitative process was signaling immediate-term exhaustion on the sell side of a stock that we risk manage like an ETF.

Before I get AAPL geniuses in a heat about that, here are the last 3 big signals our process has delivered:

- June 1, 2012 at $571.86 = BUY

- September 28, 2012 at $677.74 = SELL

- December 17,2012 at $502.50 = BUY

No research. Just math, and some behavioral context.

How many people in our profession thought/think that it’s their own unique, non-inside info, qualitative research edge that made them “smart” being long AAPL? I don’t know. All I know is that a lot of hedge funds have gone away for doing the inside info thing, and a lot more research-only funds that don’t have a quantitative risk management overlay get mad at me.

That’s progress.

So is fighting for something you believe in. I believe in evolving this profession. I believe in playing by the rules. I believe in transparency, accountability, and trust.

Keep fighting the good fight.

Our immediate-term Risk Ranges for Gold, Oil (Brent), US Dollar, EUR/USD, USD/YEN, UST 10yr Yield, and the SP500 are now $1 (Gold fails at TRADE resistance), $109.33-111.48 (Oil broke its TAIL line again), $79.29-80.08 (USD holds TAIL support again), 1.31-1.34, $88.06-89.88 (Yen oversold), 1.81-1.85% (Treasuries overbought), and 1, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer