TODAY’S S&P 500 SET-UP – January 14, 2013

As we look at today's setup for the S&P 500, the range is 26 points or 0.89% downside to 1459 and 0.88% upside to 1485.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.60 from 1.62

- VIX closed at 13.36 1 day percent change of -0.96%

MACRO DATA POINTS (Bloomberg Estimates):

- 11am: Fed to purchase $1.25b-$1.75b in 2036-2042 sector

- 11:30am: U.S. Treasury to sell $32b 3M bills, $28b 6M bills

- 11:55am: Fed’s Williams speaks in Half Moon Bay, Calif.

- 12:40pm: Fed’s Lockhart speaks in Atlanta

- 4pm: Fed’s Bernanke speaks in Ann Arbor, Mich.

GOVERNMENT:

- Senate not in session, House in session

- White House to push for comprehensive immigration plan

- Agriculture Sec. Tom Vilsack speaks at American Farm Bureau Federation annual meeting

WHAT TO WATCH

- UPS prepares to end $6.9b TNT Express takover as EU wants to block deal

- JPMorgan said to weigh releasing Whale rept faulting Dimon

- Transocean says Icahn acquired 1.56% of shrs, wants more

- Hostess names Flowers as lead bidder for bread business

- Evans says Fed support needed while govt tackles deficit

- Hedge fund leverage rises to most since 2004 as margin grows

- EnCana CEO Eresman steps down, takes advisory role

- Lockheed’s F-35 falls short of testing goals

- Japan Airlines probes Dreamliner fuel leak as FAA holds review

- BlackRock profit seen accelerating as ETF sales rise to record

- China’s unexpected export surge spurs skepticism

- Swatch buys Harry Winston jewelry brand for $1b

- Saint-Gobain sells U.S. jar unit to Ardagh for $1.7b

EARNINGS:

- Corus Entertainment (CJR/B CN) 7am, C$0.62

- PPG Industries (PPG) 8:11am, $1.53

- Cogeco Cable (CCA CN) After-mkt, C$0.88

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

CORN – fast short squeeze in Corn (+7% off the lows, up +2% this morning) after a bullish supply report from WASD (World Ag Supply/Demand) on Friday. Supply is a lagging indicator here, but with the long-term Commodity Bubble popping, volatility is much higher here than that implied by an oversold 13.36 VIX.

- WTI Oil Trades Near Four-Month High on Seaway Pipeline Expansion

- Hedge Funds Cut Bets to Six-Month Low Before Rally: Commodities

- Gold Gains in London as U.S. Stimulus Signal Weakens Dollar

- Crop Prices Advance After U.S. Supply Shrinks More Than Expected

- Copper Rises as U.S. and Japan Signal More Stimulus Is Possible

- Raw Sugar Falls in as Goldman Cuts Price Forecast; Cocoa Rises

- Rebar Rallies Most in Three Weeks as China’s Economy May Rebound

- Wilmar Boosts Africa Expansion With Palm Oil Refinery in Ghana

- Goldman Sachs Turns Neutral on Commodities Seeing Advance of 5%

- Argentine Corn Output May Rise to Record 24 Mln Tons, FAO Says

- Russia’s Yuriev Opens U.S. Shale Fund as State Dominates at Home

- Cotton Seen Climbing to $1 on Elliott Wave: Technical Analysis

- Fish & Chips Battered in U.K. as Deluge Leaves Soggy Potato Crop

- Chinese Steelmakers Boost Use of Domestic Iron Ore, Mysteel Says

CURRENCIES

YEN – getting very newsy here all of a sudden as A) the Yen hits my immediate-term TRADE oversold signal at $89.41 and B) Abe steals the top one-liner in the monetary policy world this morning stating he wants a “Bold new leader” at the BOJ (read, Money Printer who wants to live large in the Political Media spotlight like Bernanke).

EUROPEAN MARKETS

ASIAN MARKETS

CHINA – Most Read stories on Bloomberg this morn are all about Chinese growth and Japanese devaluation; Shanghai Comp ripped another +3.1% move to higher intermediate-term highs and the rest of Asian equities followed their lead (Indonesia +1.8% after leading losers at -2.4% last wk; Vietnam +12% is the best stock mkt in the world YTD).

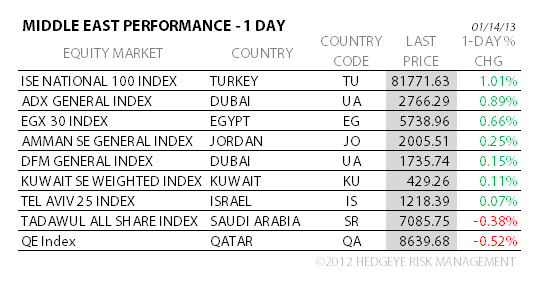

MIDDLE EAST

The Hedgeye Macro Team