Are Bad loans buried in Chinese banks going to be the next blow up?

We recently received a question from one of our macro subscribers about the threat posed by non-performing loans (NPL) to the banking sector in China, and whether the there was sufficient transparency and regulation among financial institutions there to accurately gauge the risk. The question struck a deep chord with us; from our perspective the development of the banking system has been a lingering Achilles heel in the explosive Chinese growth story of the past 15 years.

Our conclusion is, ultimately, that the full extent of the potential losses there is unknown, but that this does not undermine our overall thesis on China’s recovery potential. I wanted to share some of the bullet points that we are focused on:

The Bullish factors for Chinese financials seem clear enough: High savings rates, the strict restrictions of international capital transactions due to a closed capital account and the lack of alternatives in China have helped the banks to increase deposits at a rapid rate. Total capital, increased by the government capital injection, IPOs and the introduction of foreign strategic investors also provide opportunities for the banks to increase lending in a global environment where large internationals have seen their lending ability hobbled. What we are left to wrestle with are questions of asset quality and risk management.

Through accounting system reform and public listing, the transparency of the major commercial banks has improved in recent years, making some international comparisons of bank financial results possible, with the caveat that detailed differences do exist in accounting systems. While some Chinese banks have become competitive with the large internationals (state-owned commercial banks/SOCBs, and joint-stock commercial banks/JSCBs) in terms of assets and capital size, they still lag in terms of asset quality and profitability.

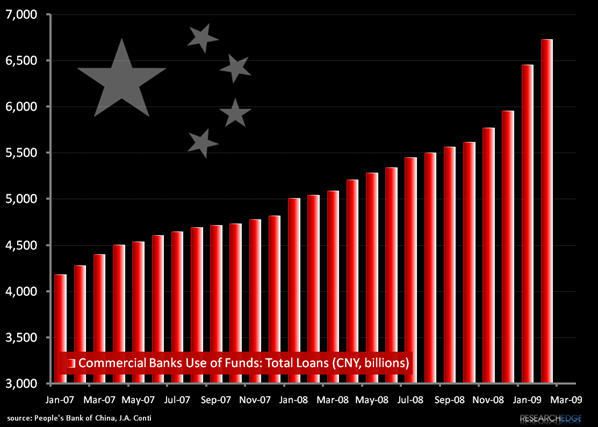

The reported average NPL ratio at the recapitalized SOCBs declined to 3.28% at the end of 2006 from 20.62 at the end of 2002. During the first two months of 2009 the level of bad loans in the Chinese banking system decreased by 17.5 billion Yuan, to 1.53 trillion Yuan, with commercial banks’ non-performing loans totaling 553.5 billion Yuan, a non-performing ratio of 2.2%, down from 2.44% at the start of 2009, according to the CBRC. It is assumed that the four-trillion Yuan stimulus plan, accompanied by credit extension of 1 trillion Yuan in new loans on average, each month, will drive the level- and ratio of non-performing loans higher with a long lag before the numbers reflect this increase accurately. The blind spot in these equations is the large number of “special mention” loans on the balance sheets of Chinese banks, a category that is not regarded nonperforming but that is deliciously defined as “the repayment of loans that might be adversely affected by some factors.” This definition leaves a very large carpet to sweep problems under.

The capital adequacy of the SOCBs improved, when measured by their amount of Tier 1 capital, after the CBRC established a regulation requiring commercial banks to keep their capital adequacy ratios above 8% after January 1, 2007, in accordance with the Basel Capital Accord. The central government subsequently committed to providing the Agricultural Bank of China with capital injections but took a harder stance with the JSCBs since most of their shareholders are local governments and state-owned enterprises (SOEs), reluctant to offer a direct bailout, pushing them to seek new money from local governments and the private sector.

In recent years the government has begun implementing a series of reforms to improve the efficiency and profitability of the state banks given the impending opening of the domestic financial sector to foreigners under the WTO. A large percentage of bad loans have been transformed from the wholly state banks to fully state-owned asset management corporations (AMCs) in return for bonds guaranteed by the Ministry of Finance. Given the weak cash recovery rate of less than 25% reported on these bad loans, these transfers are effectively government recap transactions, in some cases with direct cash injections directly from the pool of foreign reserves.

Three of the SOCBs have been transformed from wholly state-owned to corporations owned by shareholders, although the state remains the largest shareholder, listed on Hong Kong. Now most commercial banks must dispose of NPLs out of their own provisions or profits, which could be problematic due to the banks’ low profitability. In the first quarter of 2006 it was estimated by Fitch that the deposit taking institutions had US$271 billion of NPLs, which were classified as “special mention,” -the above mentioned purgatory category hovering between normal and nonperforming. Officially, the total amount of NPLs was US$206 billion, of which US$164 billion are held in commercial banks and US$42 billion in noncommercial banks. UBS Securities Asia estimated that Chinese commercial banks might have new NPLs as high as US$225billion of the loans extended during the boom period of 2002 to 2004, with a rapid increase in property loans, a focal point of the Chinese government. Large amounts of NPLs remain on the balance sheets of the AMCs, with the purchasing of US$330 billion NPLs from the four SOCBs and the Bank of Communications (BOCOM). The State Development Bank has also transferred NPLs to the AMCs. The four AMCs were originally designed to be closed within ten years but are now expected to continue under a market-oriented business model and transform their organizations into commercial entities resembling investment banks and establish securities companies with joint-venture asset management companies with foreign banks (The joint-venture AMCs were established, in part, to introduce market-oriented mechanisms into the NPL secondary market).

Having said all this, the immediate conclusion is hardly satisfying: Considering the questionable reliability of existing data, the recent rapid increase of lending and the remaining huge NPL pools held by AMCs, is still difficult if not impossible to judge whether the NPL problem in China has actually moved toward a significant resolution.

Our bullish thesis on China does not ignore these concerns, we just think that the sustainability of the national budget must also be considered within the context of the NPL issue.

We are betting that massive foreign exchange reserves and a relatively modest fiscal deficit (111billion Yuan in 2008 although with the current contraction in economic activity and the level of stimulus the fiscal deficit will expand rapidly in 2009) leave the Chinese government with the capacity to manage the issue in the short-term while progressing with banking sector reforms (another critical focus for us), capital market development and opening the capital account.

Please keep the questions coming.

Andrew Barber

Director