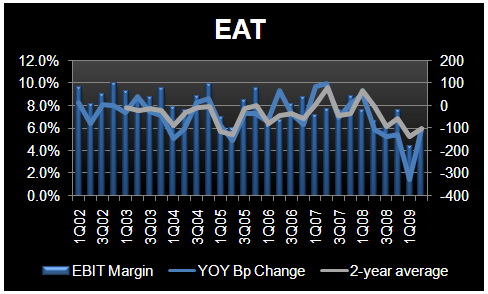

I recently commented on EAT’s CFO Chuck Sonsteby’s bullish view on margins following his presentation at an investor meeting in mid March. Specifically, he said he was optimistic about margins because EAT is benefiting from slower unit growth, improved labor productivity, lower employee turnover and better food cost control. At the same time, commodity costs are coming down. EAT’s controlling what it can combined with the fact that it consistently outperforms the industry on a same-store sales growth basis as measured by Malcolm Knapp, particularly at Chili’s, causes me to maintain that the company is one of the better positioned casual dining companies. That being said, despite Mr. Sonsteby’s more bullish sentiment, I continued to question how much fat could still be cut out of the system. The company reported better than expected 2Q09 earnings as a result of better cost control and better margins, but I remained concerned about the company’s ability to maintain its margins without a lift in top-line results.

After taking a more in depth look at EAT’s recently announced organizational changes, which it says will “create additional synergies across its portfolio of brands,” I am only more convinced that the company’s margins will not only withstand the current sales environment but also improve significantly once sales growth returns. The most important organizational change, in my view, was the announcement that the current president of the Chili’s concept, Todd Diener, will now also serve as president of On the Border, overseeing operations for both concepts. CEO Doug Brooks said, “These changes will help us to streamline organizational efficiencies and elevate the guest experience across all brands.” Although I agree with the first part of that statement in that by increasing Mr. Diener’s span of control, the company will be able to streamline its costs, this type of organizational change or cutting of brand-specific management does not typically bode well for a concept’s operations and/or guest experience. The company’s franchisees have had success with this dual brand management approach, but I think increasing management’s span of control could possible hurt the company’s ability to operate efficiently at both Chili’s and On the Border. Time will tell!

The next obvious move would be for the company to reduce its number of area directors across the two concepts, particularly where there is some overlap of brands on a geographic basis. Again, although I don’t necessarily agree with this change to the company’s business model, this could be where the real bulk of fat remains in the system. The company could easily cut people and costs out of the system across these two concepts. These reduced costs along with the company’s continued focus on labor and food costs, which are already rolling over, will provide a big cushion to margins despite sales performance. Of course, growing same-store sales would help!

It is this margin cushion that leads me to the paradigm shift…I have been talking a lot recently about the market share shifts between QSR and casual dining. Here is what we all know: The QSR players upped their quality, which helped them to become more competitive with casual dining restaurants. The restaurant industry is a zero sum game so the QSR companies grew their market share at the expense of the casual dining industry as a whole. The challenging economic environment then perpetuated this market share shift to QSR as more people sought lower priced, value menu offerings. The casual dining operators began playing the discounting game in order to try to drive traffic regardless of the impact to margins.

Now, selective QSR players are continuing to drive value (at times giving away food) but also offering more premium-priced menu items to try to compete with casual dining. So the question is, will casual dining restaurants have to maintain its current low prices in order to compete with QSR? Are lower priced casual dining offerings just a sign of the times or are they here to stay? Brinker is making structural, lasting changes to its business model. The company cannot easily or quickly reverse these recently announced organizational changes once sales improve, which leads me to believe that Brinker is permanently resetting its cost and margin structure to adjust to these lower prices and maintain the current, reduced price gap with QSR.

In the past casual dining companies operated on the basis that more is better. To drive incremental revenues restaurant companies would add more food to the plate and take prices up. This strategy works in good times but does not work when nearly every consumer is looking for ways to save money. This strategy also works when you don’t care what you are eating. As the industry is faced with the need to tell consumers how many calories they are eating, adjustments to the menu are required.

The result is a further evolution of the new paradigm in casual dining - less is more. New menu items are being introduced, with less food on the plate (fewer calories), at lower price points that are designed to maintain margins and improve traffic. Given the decline in commodity costs, it’s a great time to be reinvesting in driving new occasions.

We continue to see more price points on the menus at casual dining restaurants in the $7-$8 range. I see these price points as a big challenge for QSR operators, especially for those concepts with average checks near $6 and for those with new products geared toward trying to capture the casual dining customer. In our March 26 post titled “Is Market Share Shifting?”, we highlighted new menu items from EAT that are being introduced at $7 (• Chili's. On April 6, the chain will offer a "10 meals for under $7" deal). Regardless of the potential industry paradigm shift, EAT’s changes to its business model will definitely boost margins in the near-term.