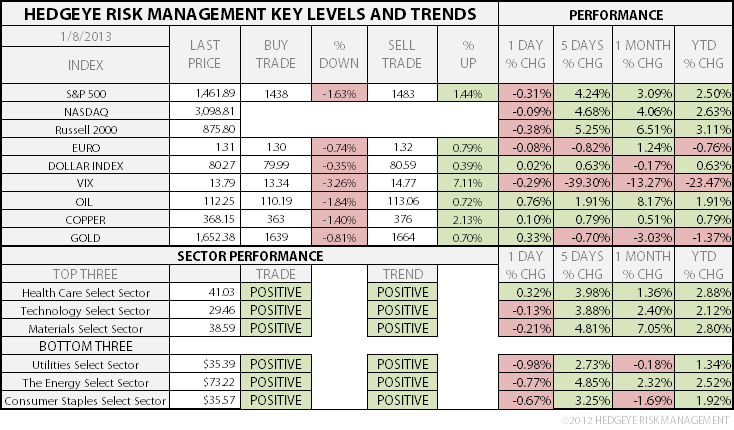

TODAY’S S&P 500 SET-UP – January 8, 2013

As we look at today's setup for the S&P 500, the range is 45 points or 1.63% downside to 1438 and 1.44% upside to 1483.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.63 from 1.63

- VIX closed at 13.79 1 day percent change of -0.29%

MACRO DATA POINTS (Bloomberg Estimates):

- 7:30am: NFIB small bus. optim., Dec., est. 87.6 (prior 87.5)

- 7:45am: ICSC weekly sales

- 8:55am: Johnson/Redbook weekly sales

- 10am: IBD/TIPP economic optim., Jan., est. 46.5 (prior 45.1)

- 11am: Fed to buy $3b-$3.75b in 2018-2019 sector

- 11:30am: U.S. to sell 4W, $25b 52W bills

- 12pm: DoE short-term outlook for Jan.

- 1pm: U.S. to sell $32b 3Y notes

- 3pm: Consumer credit, Nov., est. $13b (prior $14.16b)

- 3pm: Lacker speaks on economic outlook in Columbia, S.C.

- 4:30pm: API weekly inventories

GOVERNMENT:

- House, Senate not in session

- Obama said close to picking Jack Lew for Treasury Secretary

- API’s Jack Gerard speaks on state of oil industry, 12:30pm

- Supreme Court to hear arguments in case brought by two Gabelli Funds LLC officials seeking to block SEC claims they improperly let client engage in market timing, 10am

WHAT TO WATCH

- Alcoa profit seen recovering after output cuts as aluminum gains

- Japan to buy ESM bonds using forex reserves to help weaken yen

- Barrick ends talks with China National to sell African unit

- German exports fall more than forecast as Euro crisis cuts European demand

- Consumer Electronics Show continues: GOOG, IBM, DIS on tap

- CES roundup: Nvidia Shield, 3D Systems CubeX; QCOM

- Qualcomm upgrades mobile chip lineup fending off Intel

- JPMorgan Healthcare Conference continues: ILMN, WLP

- Samsung profit beats estimates as Galaxy fends off iPhone 5

- International Game targeted with proxy fight by ex-CEO

- GM beats Ford in U.S. government sales in first since bailout

- HSBC client admits to using offshore accounts to dodge taxes

- Chesapeake Energy CEO McClendon loses 2012 bonus amid reforms

- BAE butts into Lockheed $3b overseas market for F-16 work

- Vodafone gains after Verizon CEO signals U.S. mobile buyout is feasible

EARNINGS:

- IHS (IHS) 6am, $1.11

- Lindsay (LNN) 7am, $0.75

- RPM International (RPM) 7:30am, $0.42

- Monsanto (MON) 8am, $0.36 - Preview

- Schnitzer Steel (SCHN) 8:30am, $0.06

- Acuity Brands (AYI) 8:35am, $0.83

- WD-40 (WDFC) 4pm, $0.56

- Alcoa (AA) 4pm, $0.06

- Global Payments (GPN) 4:01pm, $0.87

- Mistras Group (MG) 4:01pm, $0.32

- Apollo Group (APOL) 4:05pm, $0.90

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

OIL – looking less and less like gold by the day; this becomes a global economic headwind in our model (to real-inflation adjusted growth), so keep tabs on it; Brent’s TAIL risk line = $111.48, so Oil is back above that and signaling $113 next as probable.

- Oil Trades Near Four-Month High on Demand, Euro-Area Confidence

- Record Car Sales Extending Shortages in Palladium: Commodities

- Soybeans Slip as Rain Forecast to Improve Brazil Crop Conditions

- Palm Oil Extends Decline as China Builds Record Port Inventories

- Gold Halts Three-Day Decline as Weaker Dollar Increases Demand

- Copper Rises as Index Weighting Change Fuels Buying Speculation

- Liquefied Natural Gas Creates a New, Global Commodity Market

- Mongolian Group Says Draft Law Hurts Foreign Mining Investment

- Iron-Ore Swaps Rise to 14-Month High as China Growth Accelerates

- Alcoa Profit Seen Recovering After Output Cuts as Aluminum Gains

- African Oil Flows Seen Shifting to Asia as U.S. Imports Drop

- Investors Should Bet on Dry-Bulk Shipping Gains: Deutsche Bank

- New U.S. LNG Terminals to Muscle in on Global Domestic Gas Trade

- BullionVault’s Gauge of Client Buying Climbs to 12-Month High

CURRENCIES

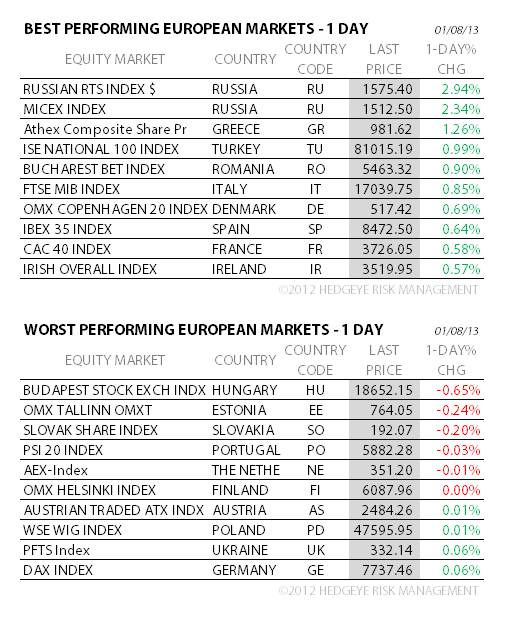

EUROPEAN MARKETS

ITALY – unemployment doesn’t improve (11.1% y/y in NOV), but the stock market pushes for a higher-high – that’s Europe, in a nutshell; where economic data is stabilizing, stocks rip (Denmark, Germany, etc); where its soft, they’re making higher-highs now too. Shorts are capitulating. Russia opens the yr +3.1%.

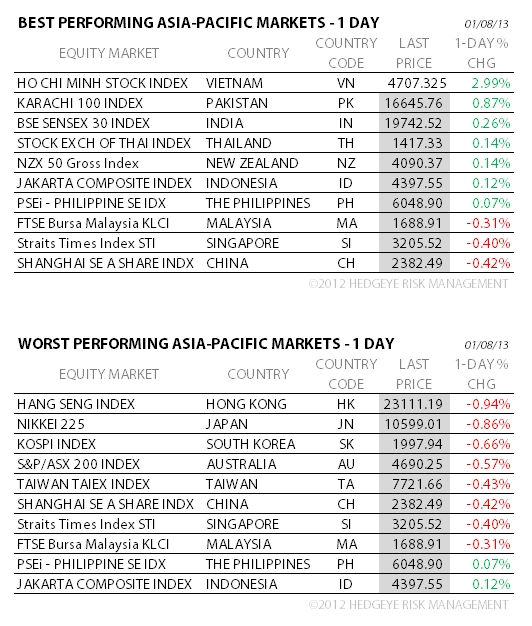

ASIAN MARKETS

JAPAN – Taro Aso is now saying he’s going to buy ESM (European debt) to “stabilize Europe” and weaken the Yen; we think this guy is crazy – and history is littered with crazy political people who have wreaked havoc on their citizenry, so stay tuned; Japanese Equity vol is picking up as people try to front run this guy; they’ll blow through the 44 Trillion Yen debt issuance ceiling.

MIDDLE EAST

The Hedgeye Macro Team