Today we added TJX as a #RealTimeAlerts Position on the short side.

The longer term story here is reasonably attractive predicated largely on the int’l store growth opportunity, rebound in European margins, and ~5%+ annual share repurchase booster, but we don’t think that the stock is appropriately discounting the risks from a more competitive department store climate on top of dwindling inventories and peak gross margins.

The near-term setup is likely to provide an opportunity to get involved lower. Most notably, the company is coming off an investment year, which should be a positive, but it is likely to incur additional spend as it pushes more aggressively into Europe. That should be heaviest as it goes up against its toughest compare of the year (1Q).

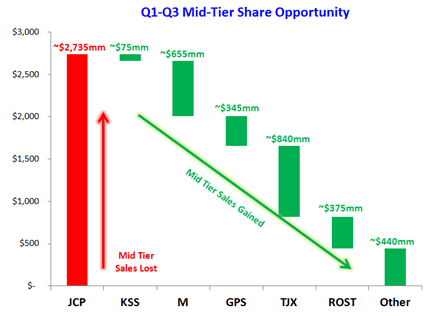

But our biggest concern is the impact of a more competitive department store space as JC Penney shows some signs of life and ceases to hemorrhage the kind of market share it ceded in 2012. Remember, a bear scenario doesn't need JCP to GAIN share in 2013, but rather simply NOT LOSE share to the extent it did last year. By a country mile, the off price retailers made out the best when JCP was incapacitated, with TJX leading the way. Where we could be wrong on the negative side is if JCP has another year of comping down solid double digits, creating an easy environment for TJX to quickly replenish its dwindling inventory levels (either directly from brands, or indirectly through department stores). We think that this opportunity would need to come by way of career risk for JCP’s Ron Johnson – something we don’t think he will let happen.

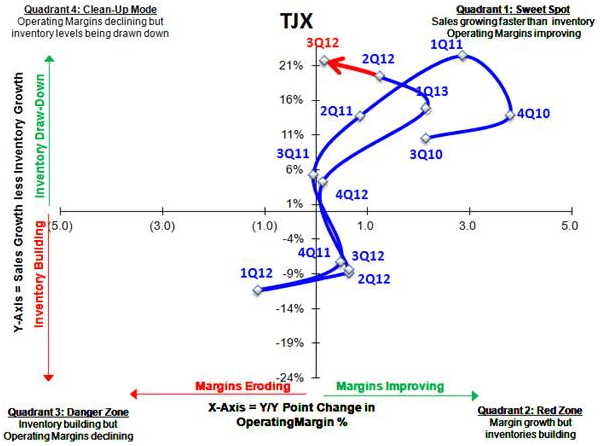

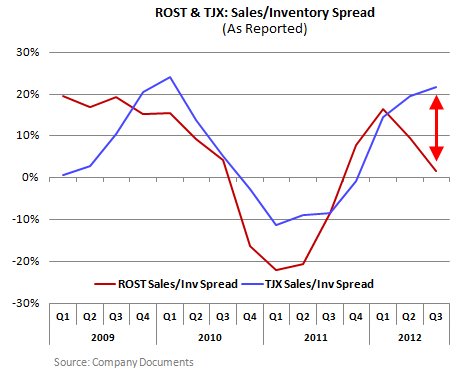

At this precise time, TJX had a noticeable (positive) boost in its sales/inventory spread – even relative to Ross Stores. The sales/inventory spread is peaking today, and while we think this has positive implications for Gross Margin, we think that it’s top line that investors will pay for – and that top line growth rate should decelerate throughout 2013.

One booster to the sales line should be TJX’s recent acquisition of Sierra Trading Post positive, but we caution that since the deal, sales estimates have picked up by just over 100bp – which is the amount of revenue Sierra will add to the parent. TJX paid ~$200mm for the business. The e-commerce infrastructure will be valuable to TJX as it looks to build out its own branded sites more aggressively.

With four discount stores out West associated with the deal, there is the possibility that TJX looks to apply their discount prowess more meaningfully to the outdoor/sporting goods space as a standalone concept. This could prove to be add an nice kicker to the value of this deal 3-5 years down the line. But that is hardly enough to get excited about today.

Valuation and Sentiment

At 8x EBITDA, 15.5x earnings and 1.2 EV/Sales, TJX is trading near peak multiples on all accounts. Sentiment is also near peak, as measured by the Hedgeye Sentiment Monitor (which blends buy side, sell side and insider trading activity). We get the whole ‘good management, good long term story, good liquidity’ argument. But the reality is that there are some headwinds in 2013 that can’t be overlooked.

Hedgeye Sentiment Monitor

Hedgeye SIGMA Analysis