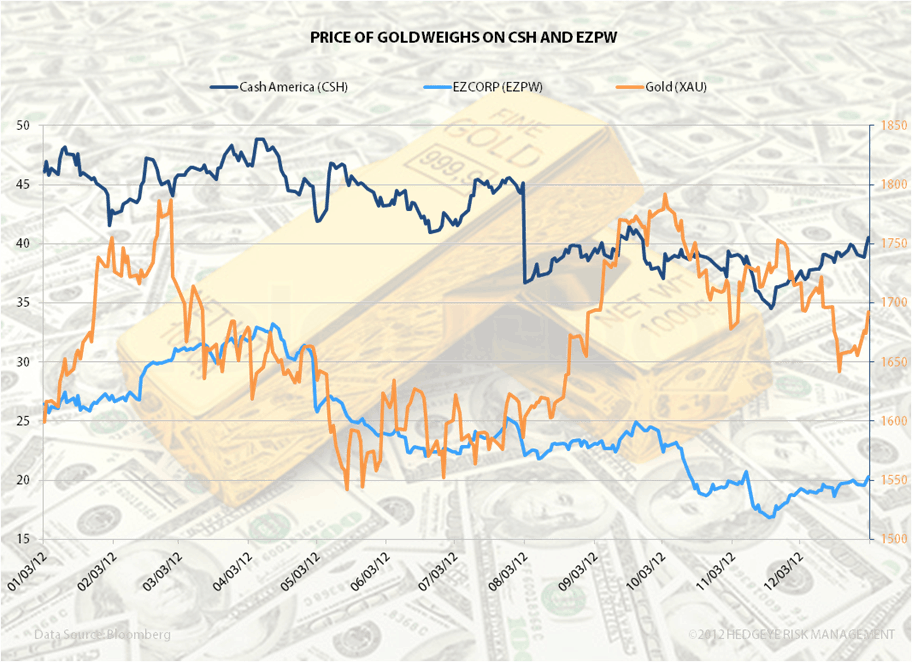

As commodity prices continue to deflate as growth stabilizes, we think that gold is likely to continue to fall in price and that will act as a headwind for pawn operators like EZ CORP (EZPW) and Cash America (CSH). It’s not just falling gold prices that will create problems for pawns going forward; gold volume also plays a significant role in the equation. Consider the “Cash 4 Gold” craze thats occurred over the past few years. With fewer customers coming in to sell gold, pawns that rely on gold and jewelry as a substantial part of their revenue will feel the pressure immediately. It’s important to keep an eye on the first quarter of 2013 as companies like CSH and EZPW are likely to feel the pain.