Average daily table revenues were HK$775 million over the past 9 days, same as the prior week and up 14% the comparable period last year. We believe the market is on pace for December YoY growth of 13-17% which would be above our original expectations of 12%. High hold percentage may be the main driver of the better than expected results.

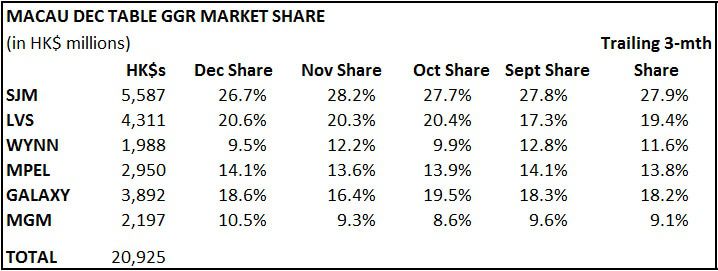

Wynn has been unable to recapture much share lost in the first 10 days of December and remains well below trend. LVS and MGM continue to outperform their recent trend. We think LVS will continue to gain share over the coming months while MGM appears to be more of an anomaly.