TODAY’S S&P 500 SET-UP – December 24, 2012

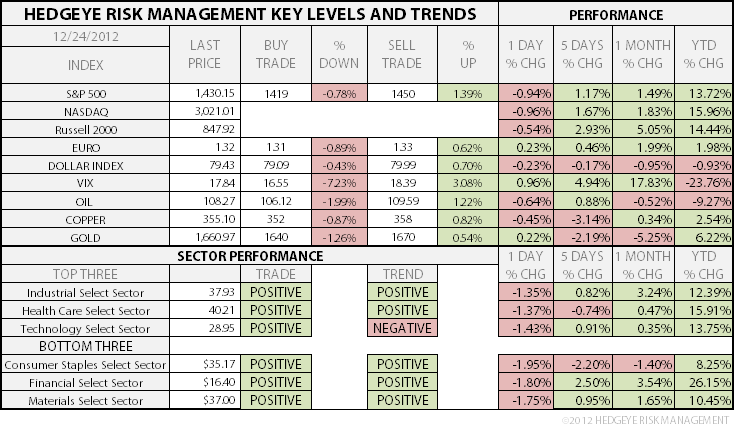

As we look at today's setup for the S&P 500, the range is 31 points or 0.78% downside to 1419 and 1.39% upside to 1450.

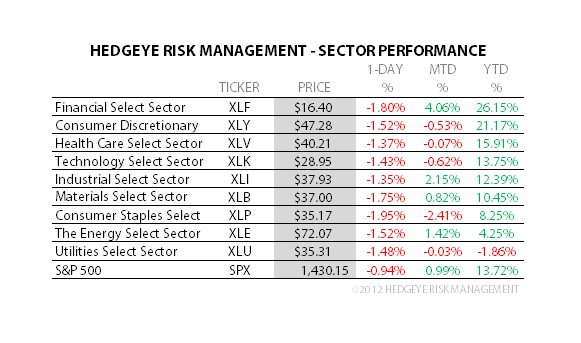

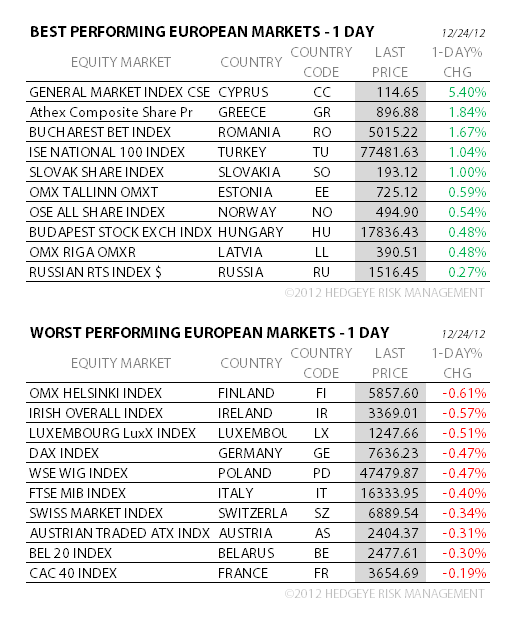

SECTOR AND GLOBAL PERFORMANCE

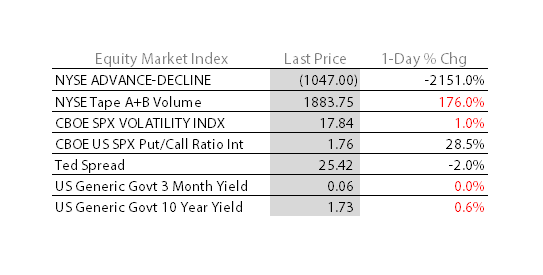

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.51 from 1.50

- VIX closed at 17.84 1 day percent change of 0.96%

- BONDS – 10yr UST Yield ticks up 1 basis pt to 1.77% this morning (instead of ticking down w/ US Equity futures); the breakout line for UST yields = 1.70% TREND (now support) and we’ll go with the bond market signal on growth all day long vs whatever stocks are doing.

MACRO DATA POINTS (Bloomberg Estimates):

- 11:30am: U.S. Treasury to sell $32b 3-mo. bills, $28b 6-mo.

GOVERNMENT:

- Federal offices closed for Christmas holiday

- President Obama on vacation in Hawaii, attended service yday for U.S. Sen. Daniel Inouye

- Hagel would be challenging nomination for Defense, Graham says

WHAT TO WATCH

- Holiday shoppers hit malls amid concerns of slowing economy

- Online U.S. holiday spending up 16%, Comscore says

- Groupon made failed bid for online luxury retailer Achica, Telegraph says

- ‘Hobbit’ top N.A. movie again with $37m in ticket sales

- U.S. gasoline falls to lowest in year in Lundberg survey

- U.S. equity exchanges, bond markets have reduced hours today

- Leveraged loan issuance in U.S. this year hit highest mark since 2007

- Sony said in talks with state-run fund to sell battery unit

- Verizon says hacker didn’t release customers’ data: Forbes

- Pimco’s Bill Gross sees probability of U.S. going over fiscal cliff of >50%

- Regions Financial probed by SEC, others on loans: WSJ

- U.S. Weekly Agendas: Finance, Industrials, Energy, Health, Consumer, Tech, Media/Ent, Transports, Real Estate

- Canada Weekly Agendas: Energy, Mining

- Week Ahead: Fiscal Cliff, U.S. Home Sales, 2013: Dec. 24-Jan. 5

- NOTE: No U.S. Daybook tomorrow due to Christmas holiday

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

OIL – continue to see selling right where it matters on both Brent and WTIC (both continue to fail at my TRADE and TREND lines of resistance); this is ultimately bullish for consumers, globally.

- Brent Crude Declines a Third Day Amid U.S. Budget Talk Impasse

- Bullish Wagers Drop to Six-Month Low on U.S. Budget: Commodities

- Copper Gains in London as Hedge Funds Boost Bets on China Demand

- German Day-Ahead Power Price Turns Negative Before Holiday

- Sugar Falls on Signs of Oversupply in Brazil, India; Cocoa Drops

- EU Carbon Permits Fall as Volumes Shrink Before Public Holidays

- Palm Oil Advances to Four-Week High on China Demand Speculation

- Wheat Futures Gain on Russia Frost, U.S. Seen More Competitive

- SEC Puts Off Decision on Blackrock’s Copper ETF to February

- Hedge Funds Boost Oil Bets Most in Four Months: Energy Markets

- Asia Naphtha Crack Gains; PetroChina Buys Jet Fuel: Oil Products

- Kazakh Wealth Fund Said to Weigh Acquisition of Kazzinc Stake

- Tiberius Says Active Commodity Fund Gained 2.4% in November

- Aluminum Canceled Warrants Are at Record High on London Exchange

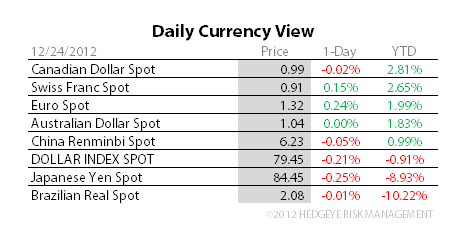

CURRENCIES

EUROPEAN MARKETS

ASIAN MARKETS

ASIA – on the top-line, Taiwan printed its best Industrial Production growth number in 9 months (+5.9% NOV vs 4.8% OCT) and from a cost of goods/living perspective Singapore reported inflation (CPI) at a 2yr low (3.6% y/y NOV vs 4.0% OCT). #bullish.

MIDDLE EAST

The Hedgeye Macro Team