“All is calm, all is bright.”

-Garth Brooks

One of my favorite holiday history songs is Belleau Wood, by Garth Brooks. It’s a song about a truce between US and German soldiers in 1918. The first WWI Christmas truce came between British and German soldiers in 1914.

“Through the week leading up to Christmas, parties of German and British soldiers began to exchange seasonal greetings and songs between their trenches; on occasion, the tension was reduced to the point that individuals would walk across and talk to their opposite numbers bearing gifts.” (Wikipedia, Christmas truce)

“Then across the frozen battlefield another’s voice joined in…

Until one by one each man became a singer of the hymn.” (Garth Brooks)

Back to the Global Macro Grind…

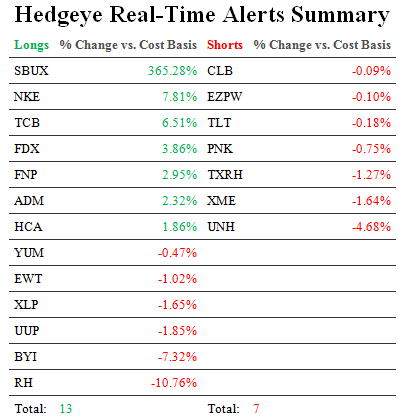

I’ll keep it relatively tight this morning – just economic data and risk management levels.

But first, here’s how I’d summarize our GIP (Growth, Inflation, Policy) model right now:

- Globally (across countries in our model), growth has been stabilizing now for almost a month

- Inflation continues to deflate, providing the real-time tailwind to this shift from growth slowing to stabilizing

- Both Treasury Bond and Gold prices do not like this (they like #GrowthSlowing)

Global Macro Economic data:

- Taiwan printed its highest Industrial Production number in 9 months this morning (+5.9% NOV vs +4.8% OCT)

- Singapore reported a 2-yr low in Consumer Price Inflation (CPI) this morning (+3.6% y/y NOV vs +4% OCT)

- CFTC Futures & Options net long contracts hit a 6 month low (-5.6% wk-over-wk to 758,256 contracts)

That last point is one of the most critical we have been focused on since making our Bubble#3 (Commodities Bubble) call - 1 of our Top 3 Global Macro Themes @Hedgeye for Q42012. It’s also what’s driving the shift in our model from growth slowing to stabilizing.

To put the market’s expectations for lower commodity prices in perspective:

- Total net long contracts are -43% below their all-time (Bernanke Bubble) peak of September 2012

- Gold net long contracts (down -13% last wk to 112,421) hit their lowest level since August 2012

- Corn contracts are getting cobbed, down another -22% last week to 175,631 (lowest since July 2012)

Now maybe the Policy to Inflate thing gets plugged back into your life in January, but the probability of Qe6 superimposing new all-time highs for commodity inflation versus those that have been bubbling up for the last decade is relatively low.

Across the board, our risk management signals concur:

- CRB Commodities Index = 294 (flat last week in an up tape for Global Equities) remains in a Bearish Formation

- Gold = down another -2.2% last week to $1657/oz, snapped our long-term TAIL risk line of $1671

- Silver = down another -7.1% last week led losers in the commodities complex, followed by Palladium at -4.8%

Yes, this is me pushing my thesis for Strong Dollar = Strong America. With the US Dollar making a series of higher long-term lows (up for 9 of the last 13 weeks), that’s the most bullish thing I can tell you this Christmas. Let free-market prices win the day.

“But for just one fleeting moment, the answer seemed to clear…

Heaven’s not beyond the clouds, it’s just beyond the fear.” (Garth Brooks, Belleau Wood)

Our immediate-term Risk Ranges for Gold, Oil (Brent), Copper, US Dollar, EUR/USD, UST 10yr Yield, and the SP500 are now $1, $106.20-109.59, $3.52-3.58, $79.09-79.99, $1.31-1.33, 1.70-1.85%, and 1, respectively.

Merry Christmas and Happy Holidays to you and your loved ones,

KM

Keith R. McCullough

Chief Executive Officer