PCAR: Key Part of Our Thesis Playing Out As NAV Loses Class 8 Share

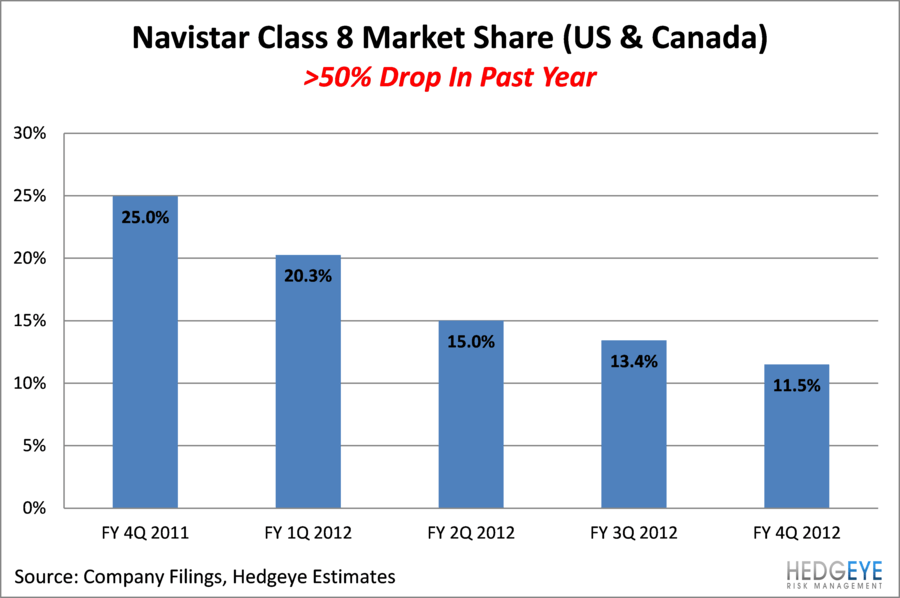

- Navistar Share Loss: In our August Truck OEM Black Book, we suggested that Navistar was likely to lose significant market share following product quality and strategy challenges. The share loss has been significant and continued last quarter.

- Unclear Call Comments: Navistar management said “And while we have lost some share during the course of the year, overall our market share has been relatively consistent for the last two quarters and our position in each segment has not changed.” (Troy Clarke) At least in the Class 8 market, this appears to be an optimistic reading, in our view.

- PCAR Should Gain: We expect PCAR to pick up a significant portion of Navistar’s lost market share. The share gains represent a tremendous opportunity for PCAR in the Class 8 space.

- PCAR Best Way To Play NAV Woes: Shorting Navistar is a risky trade, in our view, because of a potential buyout by Hino, VW, or other interested party.

- Full 2013 Benefit: Next year, PCAR should get a full year benefit of a higher market share, in our view. We note that Mack struggled to regain any of its lost market share in the 1990s.

- PCAR Top Idea: Paccar is one of our top long ideas because of share gains, reduced pre-buy cyclicality and higher construction activity. Please see our Truck OEM Black Book for additional information.

Jay Van Sciver, CFA

Managing Director

HEDGEYE RISK MANAGEMENT

120 Wooster St.

New York, NY 10012