“Waves are not measured in feet or inches, they're measured in increments of fear.”

-Buzzy Trent

Great stock calls come and go, but rarely are there times when one can ride a Macro wave that tees up broad-based outsized returns in Retail.

History points to three distinct time periods over the past decade where this worked on the long side:

a) January-November 2003 = MVR Retail Index +60%

b) March 2009-April 2010 = +165%

c) September 2011-September 2012 = +49%

Our process is leading us to one bet from here, and it’s that 2013 will not contain one of these periods. That is, unless, we see the retail group flat-out crash first. After all, in the three periods noted above, only one happened without a preceding selloff in the group before a subsequent rally.

There are two waves leading to our summation. One is Macro, and the other is Micro.

1) Macro: One thing that is critical to measure is the spread between the price consumers are willing to pay for apparel and footwear versus the price for which the wholesalers and retailers are buying the product. Simply put, one minus the other is a major component of the margin that all members of the retail supply chain fight over at the end of the day.

The beauty is, over the past year, they have not done much fighting. Following a historic surge in raw materials costs in 2011 we saw Consumer Price increases hold in the +4-5% range despite a reduction of 2-3% in actual costs in 2012.

That resulted in a quarterly run rate of about $3bn in ‘free money’ injected into the supply chain. We’re talking about $12bn in total for an industry that only generates about $30bn in annual operating profit. Some of this is yet to be reported in 4Q with a residual in 1Q13, but the fact of the matter is that we’re on the downside of this realization. It gets harder from here. This is a wave if we ever saw one…but it’s already crested.

2) Micro: This one is all about JC Penney. So many people get so caught up in their opinions of CEO Ron Johnson and his latest and greatest ideas like giving free haircuts to every school kid in America. But they don’t keep tabs on the big picture.

First off, size-wise JCP is about 8-9% of US apparel retail. To put this into perspective, it is about 4x as big to US apparel as Greece is to the Euro zone. There’s no way that JCP can have such a major change to its operating metrics without meaningfully shaking the rest of the ecosystem.

And shake it did in 2012. We don’t think it’s appreciated exactly how much share JCP has hemorrhaged in year 1. For the first three quarters of this year we’re talking over $2.7bn. When 4Q – the seasonally strongest quarter – is released, we’ll be looking at something closer to $4bn in annual share. This is coming off a base of only $17bn in revenue. Our sense is that the M’s, GPS’, KSS’ and TJX’s of the world are underestimating how much share JCP is handing them. Is it any coincidence that these companies posted some of their best growth rates in recent history as JCP imploded? This is not a permanent share shift by any stretch.

There's nothing wrong with this if the industry both acknowledges and plans around it. But ask the average CEO of an apparel company what they think about this. They'll deny that the JCP-factor is meaningfully helping them. Check M, GPS, TJX, and KSS conference call transcripts for the words “JC Penney”. You won’t find much. The industry is in denial. That means that their process around keeping the share is nonexistent.

The key distinction is that these companies need JCP to keep comping down 25% in order to continue to feel the same competitive benefits that they have today.

We have one simple question. What if JCP comps +1 for the year? That’s a +26% positive swing.

We’ll make the call right now that the company is more likely to comp positive than negative. We think they’ll have to pay for it, but we think they’ll get it. Also remember that 33% of JCP stores will be rebranded by the end of 2013. This will not make comping easy for anyone that competes with JCP, or sells into retailers that compete with JC Penney. JCP might ultimately be a zero, but it won’t get remotely close in 2013. Check out our 12/13 report “Reasons to Reconsider Your JCP Short”.

So...where’s the next wave? We think we’re in it and the barrel is collapsing. Get out of the way otherwise it could snap your board like a toothpick. On the short side, we like names that don't have much differentiation and are at the mercy of changes in the macro climate. Financial leverage is a plus. We’re talking GPS, M, KSS, and VFC. There are others that make the cut as well, but have some company specific reasons like CRI, FDO and GES.

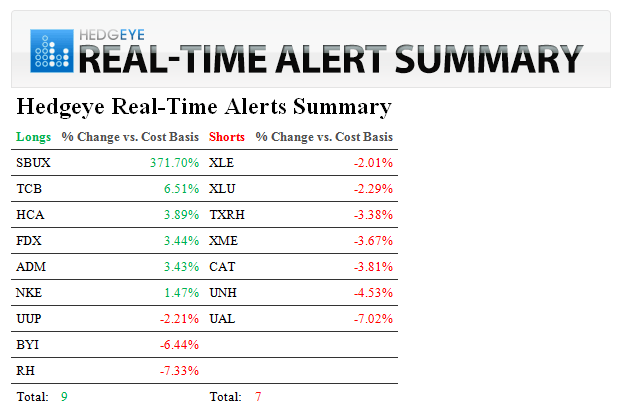

On the long side, be careful, but there are companies with asymmetric setups that should work. That's NKE, FNP, RH and RL.

In the end, Jon Kabat-Zinn said it best…'you can't stop the waves, but you can learn to surf.'

Our immediate-term Risk Ranges for Gold, Oil (Brent), Copper, US Dollar, EUR/USD, UST 10yr Yield, and the SP500 are now, $1, $105.95-108.94, $3.64-3.71, $79.36-79.99, $1.29-1.31, 1.69-1.80%, and 1, respectively.

Brian P. McGough

Managing Director