This note was originally published at 8am on December 05, 2012 for Hedgeye subscribers.

“Buying love is as stupid as loving money.”

-Loesje

Off the ice, I’m a sometimes cuddly Thunder Bay bear. And since it’s the holiday season, I decided to spread some of the holiday cheer and went shopping yesterday. I love buying things on sale, so I bought some US Consumer stocks. Why some people only buy these things when they are green is still beyond me.

Clearly, buying the love here requires a suspension of disbelief. I get that. But I am also getting used to getting that. For most of 2012, the economy has not been the stock market. On global #GrowthSlowing, the bond market has been closer to the truth.

But what is the truth? That’s a question that people have been asking since Pythagoras did circa 530BC. I’m sure Christopher Columbus found some not so true truisms when he landed on the shores of Hispanolia today in 1492 too. We’re always learning something.

Back to the Global Macro Grind…

The truth is that it helps to know when someone is lying to you. For example, look at the fine folks of the Political Class in Greece. Today, the Greeks got the nod as the “most corrupt” country in the European Union. Nice. Must do more bailouts.

In other love-oriented news this morning, it turns out that France’s sperm count just dropped by 32%. Now, if you are a single French male getting taxed at 75%, that’s a problem. The good news is that this isn’t new news. The French study cited by BBC News Europe this morning goes back to 1989. Centrally planned life was not cited as causal.

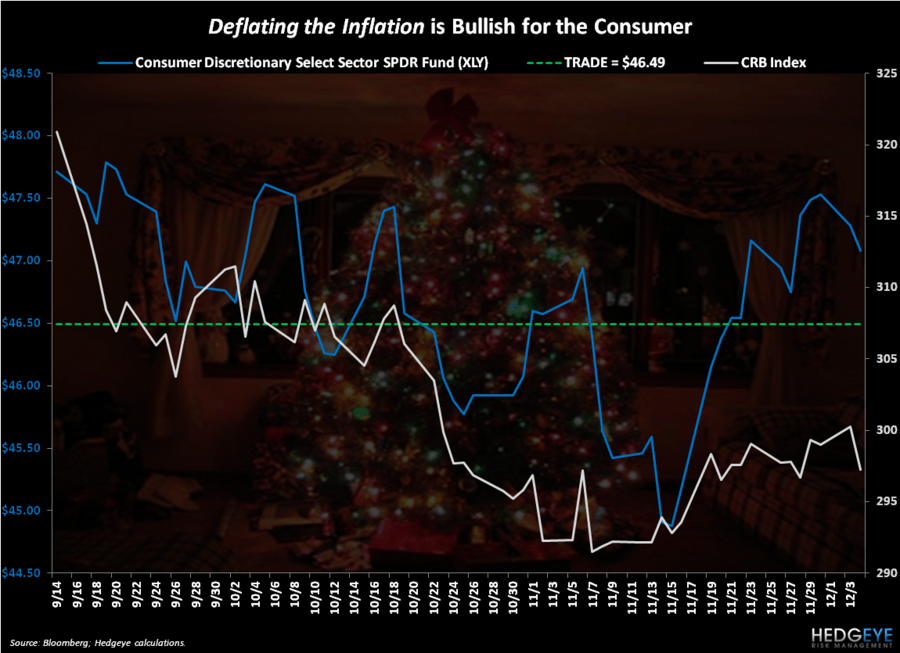

On a more serious note, why would you love buying US Consumer stocks here? The reason for that is as simple as it has always been in our Global Macro Economic model – deflating the Bernanke’s Bubble (commodities) is a real-time tax cut.

I know, I know – the whole Marxist tax demagoguery thing is still a factor out there. And I’m certainly not trying to downplay the confidence interval you’ll need to have in the bottom-up research that will get you to buy something on sale (74% of companies issuing guidance so far in Q412 have guided lower ) - but tickle me with something that isn’t French this morning and humor me.

The immediate-term risk management setup for US Consumer Stocks is as follows:

- SP500 held its immediate-term TRADE support line of 1404 yesterday

- Consumer Discretionary (XLY) held its immediate-term TRADE line of $46.49

- Consumer Staples (XLP) held its immediate-term TRADE line of $35.28

From an intermediate-term TREND perspective, the Commodity Deflation setup looks equally bullish:

- CRB Commodities Index Inflation remains in a Bearish Formation (bearish TRADE, TREND, and TAIL)

- Brent and WTI Crude Oil prices remain in Bearish Formations as well ($111.58 and $92.20 TAIL resistance, respectively)

- Food Prices (Coffee, Corn – and don’t forget Wheat! “cream of wheat” –Woody Allen) are in Bearish Formations too

So, while deflation of certain asset prices may not be good for some in the Political Class, it’s really good for the Rest of Us. If they are going to tax everything and anything that isn’t locked down, we’ll take some back-pocket relief where we can find it.

What are the risks to Buying The Love in US (or Global) Consumption stocks?

- The Government

- The Government

- And, The Government

You see, it’s only the Government that can impose Policies To Inflate on its people. Bastiat and von Misses called it plundering. That’s what politicians do – they plunder you so that they get paid (that’s why they call your taxes, “revenues”).

Moving along… In other globally interconnected market news this morning:

- Chinese stocks stopped crashing (up huge overnight at +2.87% on the Shanghai Composite)

- Russian stocks = +1.75% today (out of crash mode as well, now only -17.5% from the March #GrowthSlowing top)

- Both Global Equity Volatility and Sovereign Bonds (Treasuries and German Bunds) are finally overbought

When bonds and volatility are immediate-term TRADE overbought, it’s easier to fall in love with stocks (for a day) too.

Our Risk Ranges (support and resistance) for Gold, Oil (Brent), Copper, US Dollar, EUR/USD, UST 10yr Yield, and the SP500 are now $1694-1711, $109.12-110.69, $3.54-3.68, $79.52-80.32, $1.29-1.31, $1.59-1.66%, and 1404-1419, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer