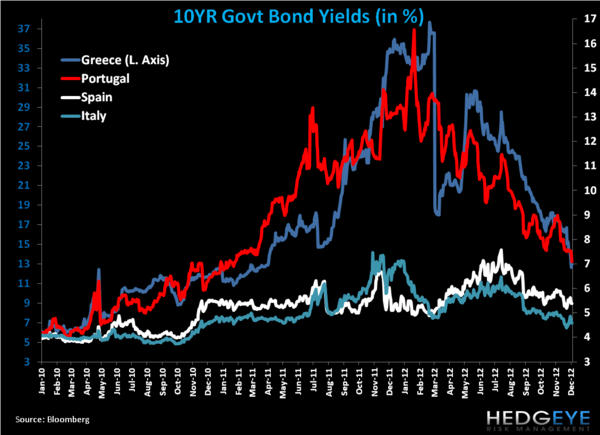

Looking at the Eurozone, risk decreased across several nations while Germany and Italy saw a slight uptick in yield. Greece declined -1.54% to 12.92%, Portugal fell -47 basis points to 7.09% and Spain dropped -8 basis points to 5.38%. Geramany and Italy rose +6 basis points and +5 basis points, respectively. Yields have fallen considerably since highs made in April of this year but have yet to reach levels seen in 2009/2010.