We think there is modest downside to Chipotle’s share price. That being said, our favorite short idea in the QSR space is BKW. As far as the long side of CMG goes, we would possibly become more constructive on the stock closer to $250.

Below, we run through some fundamental, macro, and sentiment factors that we think are important for CMG going forward. In particular, we would highlight new unit performance as a key metric to focus on when trying to get comfortable with the intermediate-to-long term outlook for the stock.

Top-Down View

Chipotle’s stock price has cratered since early 2012, declining almost 40% from its peak in April. Picking the bottom is likely to be difficult, albeit not as difficult as picking the top, but we believe that the bottoming process is going to take several quarters as the fundamentals flush out.

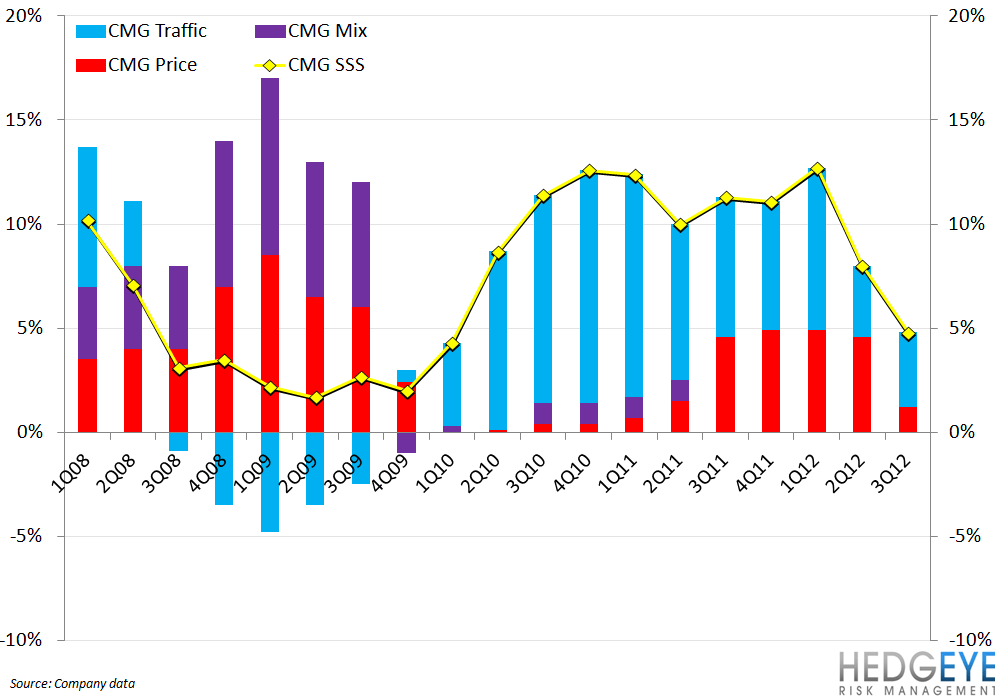

Macroeconomic growth is an important driver of Chipotle’s business. The following chart shows that something clearly has gone awry with the Chipotle growth model; average unit volume growth has decelerated in recent quarters.

Fundamental Outlook

Same-restaurant sales growth has come in meaningfully as the company is struggling to re-accelerate top line growth. Average check has been negatively impacted by lower drink sales and the outlook for FY13 comps is flat-to-low-mid-single-digit growth. Two further “difficult” top-line compares remain before we can start to expect higher same-restaurant sales growth numbers. The favorable weather in 1Q11 added, by management’s estimation, contributed 100-200 bps to the quarter’s same-restaurant sales growth number. We believe that there is a stong possibility that CMG posts negative SRS in one or both of the next two quarters. Consensus expectations are for the company to maintain positive SRS over the next two quarters.

Total sales growth has been decelerating, sequentially, for the past couple of quarters. As long as Chipotle is growing at a mid-teen percent-rate, we will focus on the growth in new unit volumes as a signal of likely improving sales growth for the company.

We believe that new unit average unit volume growth has, and will continue to be a critical metric for this stock. In terms of picking inflection points in growth, the performance of new units has been the one signal worth watching over the past few years. For the stock to begin the bottoming process we must also see a stabilization in new unit volume performance. If the new unit continue to underperform the real estate strategy and the accelerated pace of development will be called into question.

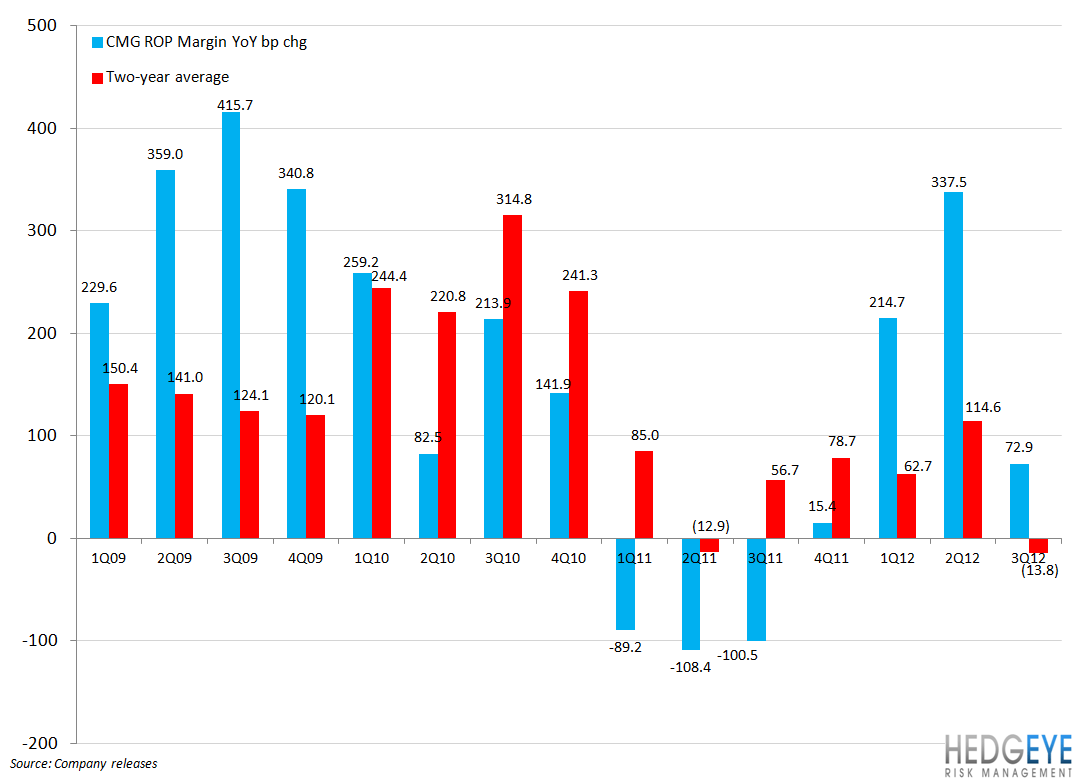

Restaurant-level margins remain the wild-card of 2013, in our view. Chipotle’s restaurant operating margins are vulnerable to swings in commodity prices as the company purchases its ingredients on the spot market. Inflation is currently running at low-single-digit levels, driven by higher dairy and meat prices. Ultimately, margins in 2013 are sensitive to more adverse weather conditions that impact protein prices. Guidance is also baking in avocado prices remaining at current levels next year

Labor costs have been a source of margin expansion for CMG for years as the company’s efficient operating model has been complemented by strong traffic gains. Now that traffic growth has decelerated considerably, we think that there is heightened risk in assuming continuing leverage to be driven through the labor line.

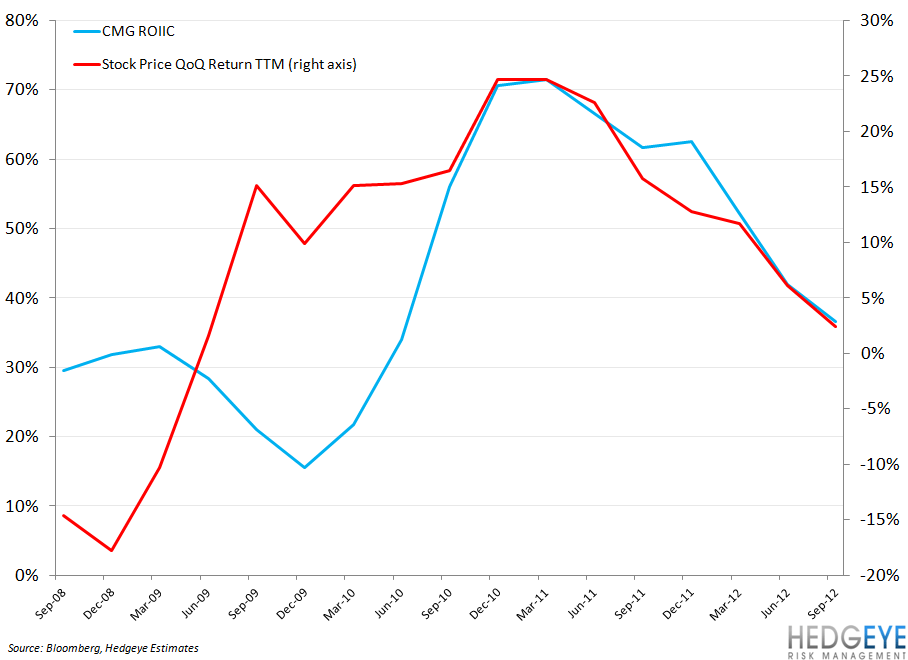

In aggregate, the outlook for the company’s Return on Incremental Invested Capital is still uncertain and we believe that the company slowing growth, and cutting capex, could serve as a catalyst to take a long position in the stock at a lower price. Currently, with capex growth far out-stripping sales growth, we would not sleep too well the night before Chipotle’s next earnings call if we were to buy in at this level. Longer-term, we believe the company’s business model is likely to deliver strong returns for shareholders but our confidence in near-term ROIIC is less firm.

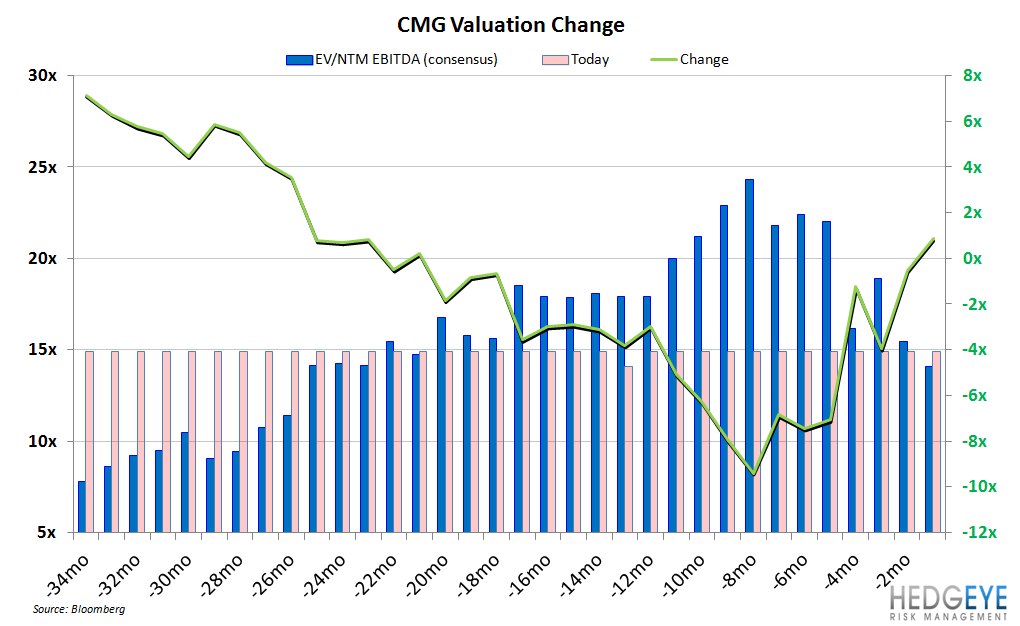

Sentiment & Valuation

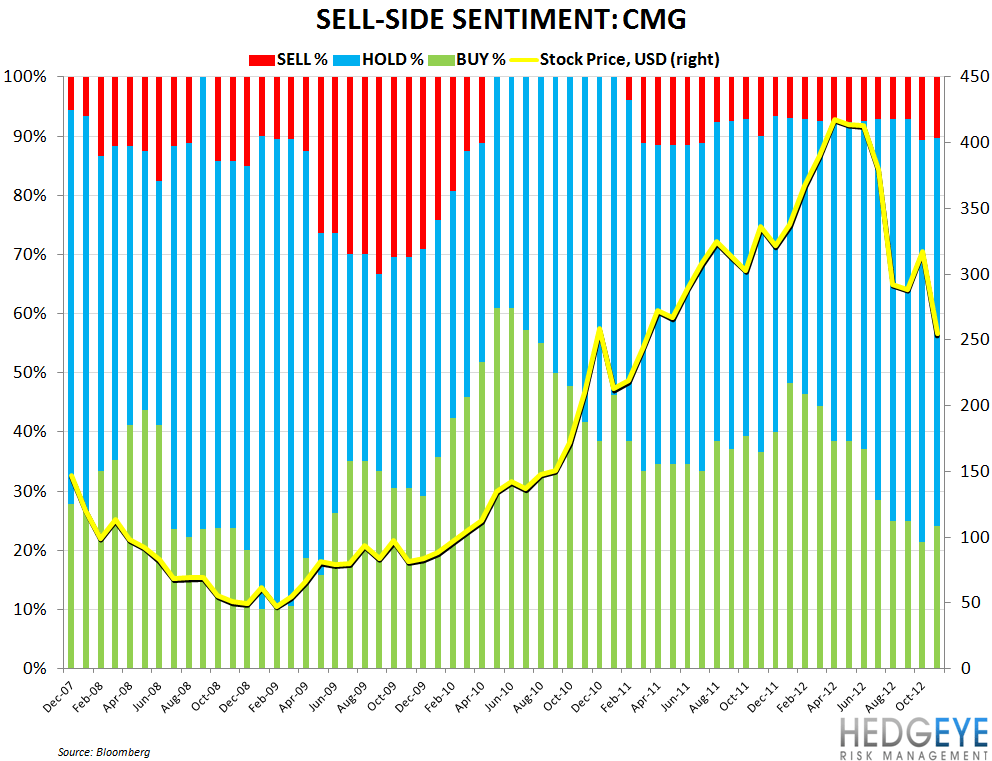

The investment community’s view of CMG has changed drastically in 2012 but we would point to historical precedent as a suggestion that the Street can likely become more bearish from here. Short interest has been rising since May. It’s worth noting that, the last time this company’s growth model was encountering problems of the magnitude that it now seems to be facing, short interest as a percentage of the float was in the 30’s.

We hold a similar view of the valuation outlook for CMG. We believe that there is further downside risk to FY13 EBITDA and EPS estimates. While the multiple has come in, it is possible that the bottoming process could take some time if we are right that there are negative revisions to estimates coming over the next few quarters.

Howard Penney

Managing Director

Rory Green

Senior Analyst