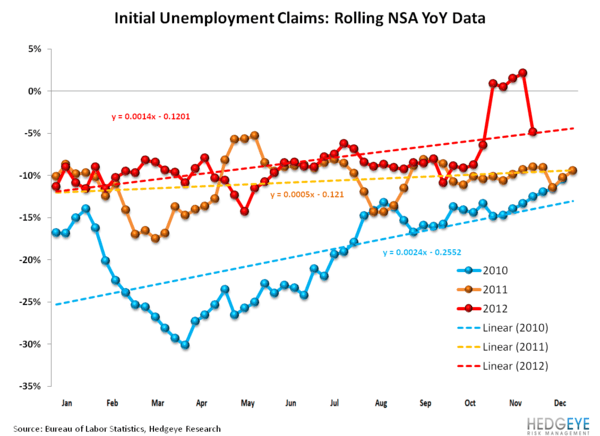

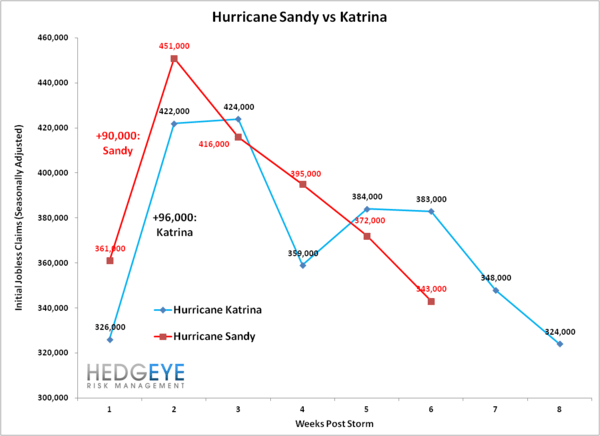

Today’s Jobless Claims numbers came in at 343,000, another strong showing on a week-over-week basis that suggests Hurricane Sandy is no longer affecting the data. The 343k print is significant because it represents a new low in claims post-financial crisis. It also returns claims to the seasonal trajectory we’ve seen in the last three years (i.e. the seasonality mal-adjustment tailwind is back in full effect).

Jobs data continues to improve but more importantly, the perception is even more positive than reality and perception is everything. The rate of improvement will continue to be strong through February of 2013. Between jobless claims and the recovery in the housing market, there’s a lot to be excited about here.