TODAY’S S&P 500 SET-UP – December 13, 2012

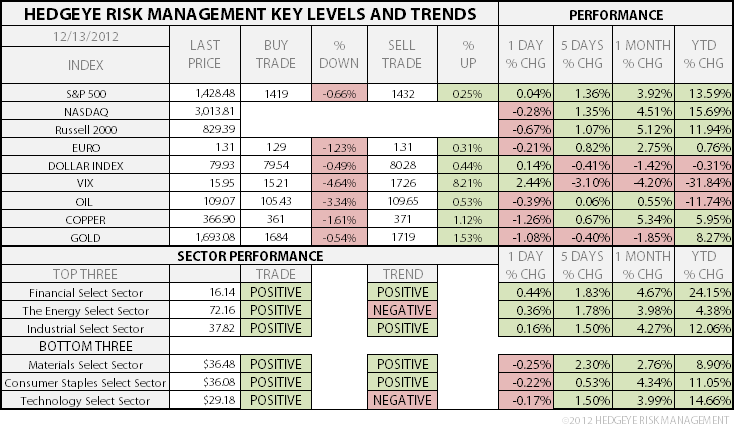

As we look at today's setup for the S&P 500, the range is 13 points or 0.66% downside to 1419 and 0.25% upside to 1432.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.46 from 1.46

- VIX closed at 15.95 1 day percent change of 2.44%

- BOND YIELDS – huge relative move in Treasuries yesterday (primarily because volatility in Fixed Income has gone away), but the 10yr yield held below 1.71% TREND resistance backing off to 1.69% this morning; TAIL resistance on the 10yr = 1.89% and that’s as good a proxy for US growth expectations as any right now.

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Advance Retail Sales, Nov. 0.50% (prior -0.30%)

- 8:30am: Retail Sales Less Autos, Nov. 0.00% (prior 0.00%)

- 8:30am: Producer Price Index (MoM), Nov. -0.50% (prior -0.20%)

- 8:30am: PPI Ex Food & Energy (MoM), Nov. 0.10% (prior -0.20%)

- 8:30am: Initial Jobless Claims 8-Dec 368K (prior 370K)

- 8:30am: Continuing Claims 1-Dec 3210K (prior 3205K)

- 8:45am: Bloomberg Dec. United States Economic Survey

- 9:45am: Bloomberg Consumer Comfort 9-Dec (prior -33.8)

- 10am: Business Inventories Oct. 0.40% (prior 0.70%)

- 10am: Freddie Mac mortgage rates

- 10:30am: EIA natural-gas storage change

- 11am: Fed to purchase $4.25b-$5.25b notes

- 11:30am: U.S. to sell $10b cash-management bills

- 1pm: U.S. to sell $13b 30-yr bonds reopening

GOVERNMENT:

- House, Senate in session

- House Financial Services holds hearing to examine effects Volcker Rule will have on businesses seeking access to capital markets

- House Agriculture panel holds hearing on Dodd-Frank derivatives rules, international markets, 9am

- Senate Judiciary votes on Sen. Al Franken’s privacy bill that would require smartphones, apps to request user permission before collecting, sharing location data, 10am

- Rep. Edward Markey, D-Mass.; Rep. Joe Barton, R-Texas hold a briefing on data brokerage industry, how companies collect, assemble, sell consumer information to third parties, 10:30am

- House Transportation holds hearing on private-sector participation in high-speed rail projects, 10am

- Transportation Secretary Ray LaHood delivers remarks at news conference on holiday drunken driving crackdown program, 10am

WHAT TO WATCH

- Retail sales in U.S. probably rose as auto demand rebounded

- Americans back Obama tax-rate increase tied to entitlement cuts

- Apple releases Google’s mapping application through iTunes

- MetLife taking steps to deregister as bank holding co.

- Euro zone set to back Greek payment post-Merkel endorsement

- Aetna CEO sees doubling of some health insurance premiums

- Citigroup named in lawsuit by Swisscanto

- CFTC urged to delay implementation of Dodd-Frank 6 mos.

- FCC requires wireless carriers to allow text-to-911 services

- Foxconn to assemble Amazon’s smartphone: Commercial Times

- Amazon selling Kindles on its own Chinese website

- SNB maintains currency ceiling as crisis woes weigh on franc

- Canada considering alternatives to F-35 fighter jet

- Errors in credit reporting may get easier to resolve: CFPB

EARNINGS:

- Pier 1 Imports (PIR) 6am, $0.25

- Ciena (CIEN) 7am, $(0.06)

- Empire (EMP/A CN) Pre-mkt, C$1.26

- VeriFone Systems (PAY) 4:01pm, $0.76

- Adobe Systems (ADBE) 4:03pm, $0.56

- Nordson (NDSN) 4:30pm, $1.03

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

COPPER – not down as much as Silver (getting smoked, -2.6% this morning as the Bernanke Bubble continues to pop), but down the same as China was overnight. I see no irony in either. We’ll keep shorting anything that ticks that is related to the mega Mining Capex Bubble.

- Palm Oil Tumbles to Three-Year Low as Stockpiles Climb to Record

- Bonus Cuts as Jobs Decline for Oil-to-Metal Traders: Commodities

- Oil Drops From One-Week High Amid Disagreement on U.S. Budget

- Wheat Rebounds From Five-Month Low as Drop May Attract Buyers

- Gold Drops as Rally to Highest This Month Spurs Investor Sales

- Copper Drops on U.S. Growth Concerns as Stimulus Optimism Fades

- Sugar Slides in London on Ample Brazilian Supply; Cocoa Declines

- Natural Gas $4 Cap Seen in 2013 as Supply Swells: Energy Markets

- U.K. Lifts Ban on Shale Fracking, Allowing Cuadrilla to Drill

- Iron Ore Prices in China Show Imports to Slow: Chart of the Day

- Top M&A Ranked Mitsui Targets Food With $17 Billion Cash: Energy

- Sierra Leone Blood Spills as Iron Ore’s Boom Stirs Ghosts of War

- Europe Exports to Asia Seen Surging in Deepening Crisis: Freight

- Oil at $60 or $120 Doesn’t Prevent U.S. Supplanting Saudi Arabia

CURRENCIES

EUROPEAN MARKETS

ASIAN MARKETS

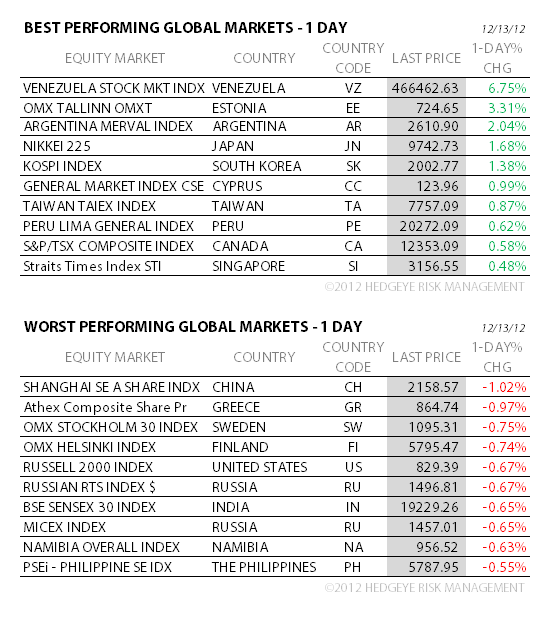

CHINA – one of the more solid 3-factor intermediate-term TREND leading indicators we use on Global Growth = CHINA/COPPER/BONDS; that composite tends to sniff out the truth as consensus hedge funds short low and cover high. China backed off its TREND resistance (2095 Shanghai Comp) this week, closing down -1% overnight, down -16.2% since global #GrowthSlowing began in March.

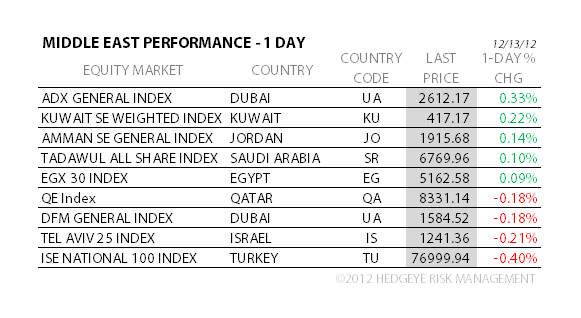

MIDDLE EAST

The Hedgeye Macro Team