We still like URBN even after the +6% move reflecting the positive QTD comp update after yesterday’s close of +HSD ahead of expectations (+5%E). It’s worth noting this outperformance came against the tougher half of the quarter – comps get easier over balance of 4Q. Revisions out over the last 24-hours will be the latest in what we expect to be a series of upward earnings revisions. We’re still +11% above consensus for F13 (half of which has been updated) and +19% above the Street for F14 representing an average of 28%+ EPS growth over the next two years.

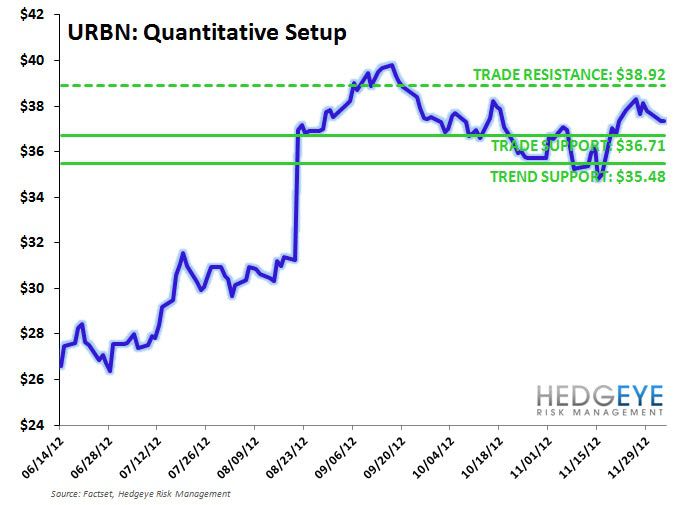

Up next on the catalyst calendar is an update at ICR in mid-January right as Anthro is accelerating out of the turn and then earnings in early March. A year after reshuffling the senior ranks, it appears that management is hitting its stride and doing everything right. In addition, with URBN breaking through its TRADE line of resistance at $38.92 this morning it has a bullish setup here according to Keith’s quantitative risk management levels.

With a favorable fundamental setup over the next several quarters, one of the best positioned e-commerce businesses in retail (20%+ of sales) headed into the holidays, and quantitative factors all in alignment, we see 25%+ upside from here in 2013.

Here are our thoughts from last week’s Idea Alert on URBN:

“We published it first on 3/22 with the stock at $28. Then again at $26 on 5/22. Today we have an opportunity to publish it again in the wake of a 'less than breathtaking' quarter. Though we think we'll have the opportunity to remind you of our thoughts again 20% higher a year out.

Underlying business trends came in largely as expected in the most recent 3Q, but importantly posted continued improvement in fundamentals. Importantly, Anthro is reaccelerating headed into a highly anticipated holiday season for the brand. With a rebound in comps along with new store, online, and international growth opportunities, we see a sustainable return to low double-digit top-line growth. Moderating markdown rates coupled with tighter inventories (see SIGMA below) is gross margin bullish at the same time the company is beginning to leverage its investment spending including its new DC. This call isn’t predicated on a return to prior peak margins (18%+) to work. In fact, we’re shaking out at +/- 16% margins over the next two years which will likely prove conservative.

The reality is that sentiment is still not overly bullish with 46% Buy ratings from the 31 firms that cover the name. While modestly more bullish than the 43% Buy rating mix YTD, it’s well below the 60%-80% mix from 2008 through 2010.

We’re shaking out ahead of the Street in the upcoming quarter as well as +12% and +20% above consensus EPS in 2013 and 2014 respectively. After nearly two years of declining estimate revisions, we think we’re at an inflection point of what we expect to be multiple upward earnings revisions in 2013. It's not cheap, and it’s a slow grind to full recovery. But from where we sit, boring can still work.”

URBN Risk Management Levels (on 12/4):

URBN SIGMA is back in the sweet spot (sales outpacing inventory growth with margins expanding):