DG’s EPS beat this morning is uninspiring. The key trend to watch continues to be the rate of consumables growth. For the third quarter in a row consumables grew as a percent of sales, but at a decelerating rate sequentially (on a TTM basis). This trend is notable because 1) consumables tend to be a lower gross margin business – a positive, and 2) they are a key traffic driver – not good. As such, it’s not surprising to see DG post comps +4% shy of expectations+4.6%E in the quarter. In addition, DG’s 4Q comp outlook of +3%-4% vs. +4.3%E suggests continued pressure on the top-line over the near-term.

One of the key factors to consider here is the recent introduction of tobacco at FDO. As one of DG’s chief competitors, this is a notable shift as it’s the only dollar store to sell tobacco to consumers over-indexed to smoking. It’s hardly a game changer for DG today, but when a key competitor needs to shift to Smokes to get its comp, it’s not exactly a positive sign for the space. We continue to think that ‘the consumables shift’, which has been driving comp for both major Dollar Stores, is getting long in the tooth to say the least.

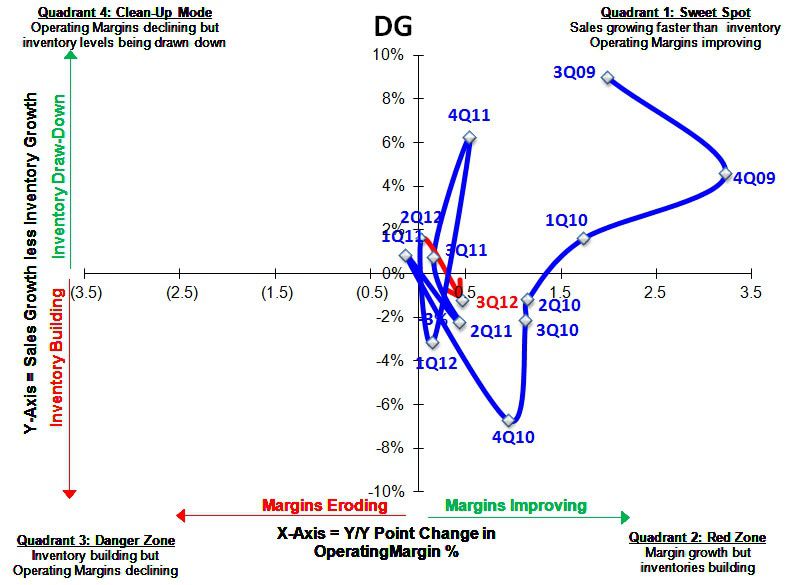

Lastly, with inventories outpacing sales growth this quarter and a tough comp ahead in 4Q (including an extra week), this is not a good setup near-term for DG.