Our expectation of a strong December, with accelerated YoY growth from November, seems to be coming to fruition. Average daily table revenues were HK$930 million, up 33% from the comparable period of 2011, and much higher than November’s ADTR of HK$769. Our full month GGR projection for December is HK$25-26 billion, up 9-13% YoY. Beyond December, we remain concerned with smoking restrictions to be implemented in January, stabilizing Mass hold %, China’s corruption crackdown, and the recent poor performance of the Shanghai stock exchange.

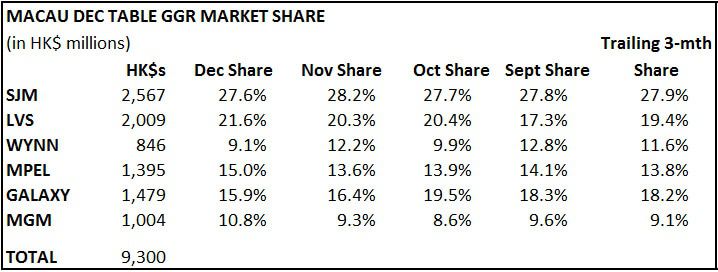

For market shares, MPEL, MGM and LVS are strong out of the gate here in December, all well above recent trend. We are hearing that the market held high in the first 10 days with the exception of Wynn and Galaxy. We continue to believe that LVS and MPEL are the most defensive stocks against our slowing growth theme. LVS should continue to be a market share gainer over the next 12 months while MPEL is on track to handily exceed Q4 EBITDA projections.