TODAY’S S&P 500 SET-UP – December 10, 2012

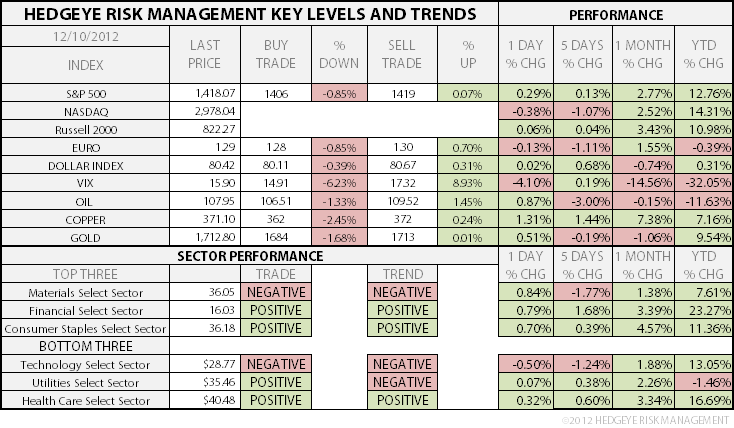

As we look at today's setup for the S&P 500, the range is 13 points or 0.85% downside to 1406 and 0.07% upside to 1419.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

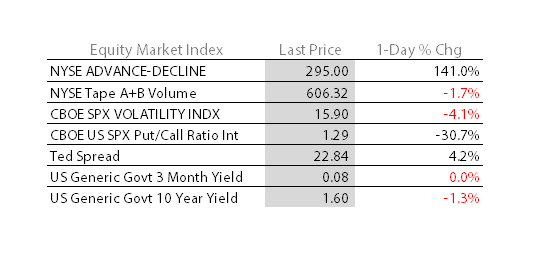

- YIELD CURVE: 1.37 from 1.38

- VIX closed at 15.9 1 day percent change of -4.10%

MACRO DATA POINTS (Bloomberg Estimates):

- 11am: Fed to buy $1.5b-$2.25b notes due 2/15/36-11/15/42

- 11:30am: U.S. Treasury to sell $32b 3-mo., $28b 6-mo. bills

- 12:45pm:Bank of England Governor King speaks at Economic Club of New York

GOVERNMENT:

- President Obama to deliver speech in Detroit to promote his federal budget deficit plan

- FDIC Systemic Resolution Advisory Committee meets to discuss Title II of Dodd-Frank Act

WHAT TO WATCH

- Obama, Boehner held private meeting at White House on budget

- Greece extends deadline for debt buyback after nearing target

- Canada’s approval of $20b energy takeovers may spark more foreign investments

- Dragon Systems founders take Goldman to trial over advice

- SEC said to investigate SAC Capital’s trading in Intermune and Weight Watchers

- Apple, Google team up for $500m-plus Kodak patents bid

- AIG sells ILFC majority stake to Chinese investors for $4.23b

- Japan sinks into recession as opposition leader Abe calls for more stimulus

- China’s exports rose less than forecast in November

- Ingersoll-Rand said to plan share buyback, asset spinoff

- Apple/Samsung ruling on U.S. phone sales may come this week

- Wanxiang outbids Johnson Controls for most of A123 assets

- Suntory weighs takeover of whiskey maker Beam, official says

- Mattel returns to appeals panel that threw out Bratz verdict

- ‘Skyfall’ reclaims top spot with ticket sales of $11m

EARNINGS:

- Ferrellgas Partners (FGP) 7am, $(0.23)

- John Wiley & Sons (JW/A) 8am, $0.82

- Casey’s General Stores (CASY) 4pm, $0.85

- Teavana Holdings (TEA) 4:01pm, ($0.01)

- Greif (GEF) 4:07pm, $0.55

- ABM Industries (ABM) 5pm, $0.40

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

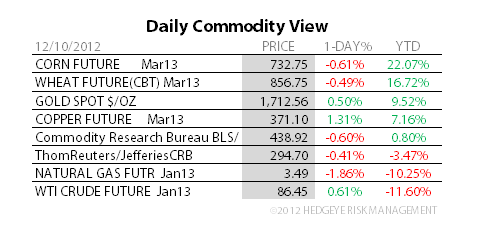

- Oil Rebounds as German Exports Advance; OPEC to Meet in Vienna

- Speculators Cut Bullish Bets on Fiscal Cliff Talks: Commodities

- Japanese Aluminum Fees Said to Decline for First Time in a Year

- Gold Gains in London on Drop to One-Month Low, Stimulus Outlook

- Copper Reaches 7-Week High as Chinese Industrial Output Expands

- Corn Falls to Three-Week Low as South American Outlook Improves

- Sugar Declines on Indications of Ample Supplies; Cocoa Slides

- Gold Set for Retreat on Momentum Indicator: Technical Analysis

- China Crude Imports Rise to Six-Month High as Oil Refining Jumps

- Tin Shipments From Indonesia Drop for First Time in Three Months

- Iron-Ore Exports From Australia Jump to Record on China Recovery

- Palm Oil Stockpiles in Malaysia Climb to Record as Exports Drop

- Japan Suspends Beef Imports From Brazil on Mad-Cow Disease

- Hedge Funds Quit U.S. Natural Gas as Cold Fades: Energy Markets

CURRENCIES

USD – 1st up week in 3 for the USD last week punished Commodity prices, and we liked it. Oil in particular is back into a Bearish Formation after snapping TRADE support of $109.63 Brent; TREND in USD is higher, not lower (up for 8 of last 11 weeks), so we’ll see if getting a cliff deal strengthens it further – not clear on that yet either way.

EUROPEAN MARKETS

ITALY – Monti probably took a peek at down -2.4% y/y Q3 GDP growth and said we’re out! So is whoever bought last week’s lower-highs in Italian equities; MIB index down hard (-3.4%) moving back below 15,615 TRADE support and back into a Bearish Formation – risk happens fast.

ASIAN MARKETS

CHINA – Chinese stocks moved out of crash mode putting on a +4.1% move last week and saw +1.1% follow through this morning back about my TRADE line of 2039 support (Shanghai); that was bullish, and so was NOV Industrial Production growth (10.1% vs 9.6% in OCT) and Retail Sales (+14.9% vs 14.5%); CPI rose to 2% from 1.7% only neg news.

MIDDLE EAST

The Hedgeye Macro Team