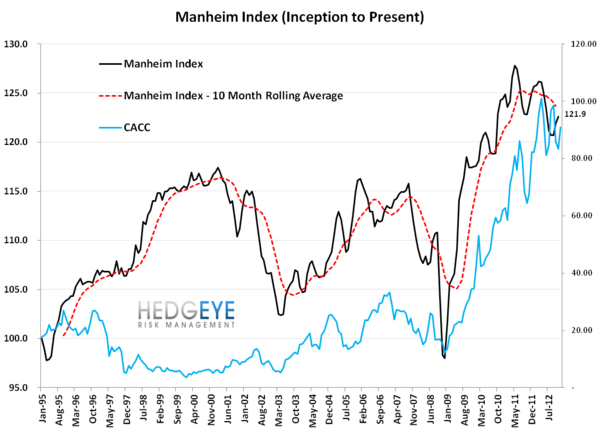

The Manheim Index of used car values tends to closely correlate to the S&P 500 and right now we're seeing upside in both indices. The Manheim Index rose 0.6% month-over-month in November to 122.6 but declined on a year-over-year basis by 1%.

Hurricane Sandy played a role in the November numbers by reducing supply and increasing demand for used cars, which is expected to continue into December and part of early 2013. Interestingly, Manheim co-integrates with the labor market. A generally improving labor market means more people need cars to get to work and most cars on the road are…wait for it….used. This is one reason why we're so interested in the decline in Manheim over the last few months. It seems to be a contradictory data point compared with what the other labor market series are telling us.