Just about any development that gives the investment community ‘hope’ in JCP these days gets the stock rallying. That’s exactly what happened yesterday with a newly formed REIT structure out of Loblaw – Canada’s largest food retailer. But one consideration people should keep in mind is that if JCP creates a REIT, it may not be able to make its rent.

After five years of starving its store base of capital and pushing out leases to preserve cash flow, we’re left asking what levers the company has left to pull if sales and profitability growth fail to materialize. The most obvious option is to leverage the company’s real estate assets, a strategy that Bill Ackman & Co. have considerable experience with. Here’s an option JCP could consider to unlock its real estate value:

REIT Option: Back in January 2011, Dillard’s announced its intent to form a REIT in order to “enhance its liquidity” by transferring “real properties” that are currently owned and lease back the properties under triple net leases. Given an improved environment and recent transactions in the REIT sector, this strategy is likely under consideration for other retailers as well in an effort to unlock real estate value.

Loblaw’s announcement is similar to Dillards in that it is planning to spin off roughly 70% of its property assets worth more than $7Bn into a REIT. The funds from the transaction will be reinvested in the operating business. With cash flow from operations YTD down -$655mm and net debt-to-equity at historical highs at 0.67x, the probability of JCP pursuing this option is still low, but increasing on the margin.

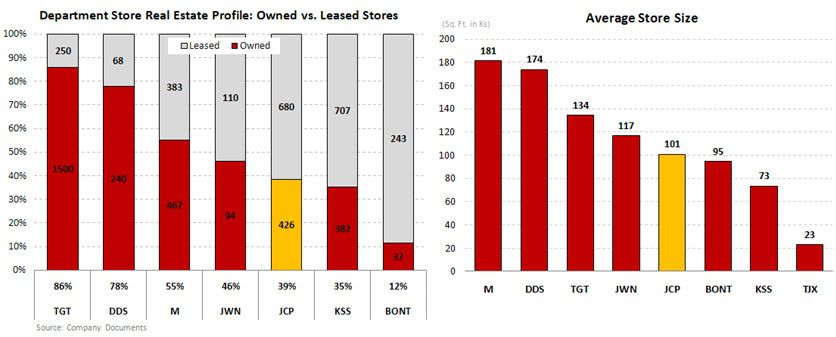

Since the formation of a REIT provides the greatest benefit for retailers that own a substantial percent of their real estate, we’ve looked at the likely candidates (see chart below). Both Macy’s (55%) and Nordstrom (46%) own a greater portion of their store base compared to JCP, but even with 39% of its real estate owned, this is an option for Penney’s to consider.

JCP currently owns approximately 39% of its real estate, or 44.6 million sq. ft. Based on current rent and cap rates, we estimate JCP’s potential REIT value at $1.85Bn-$2.55Bn, or $8.25-$11.50 per share.

While forming a REIT is not likely, one thing to keep in mind that Steven Roth is on JCP’s board. While Loblaw’s announcement may have roused speculation in the start of a potential trend, recall that Roth was one of the first to execute such a strategy when he bought Alexander’s out of bankruptcy in 1993 and converted it to a REIT. Roth has “been there and done that” before.

Here’s an obvious but big consideration.

Also, this 39% that is owned carries very low cost on the land. Yes, the company is depreciating the property (some of which is fully depreciated). But if it created a REIT, it would actually have to start paying market rent on this property. Funds from a transaction would provide operating cash and cushion initially, but rent expense could ultimately prove problematic for JCP over time.

In a perfect world, the 39% of JCP’s stores that are owned will be the 400 stores that are not going to be converted into the new format. After all, keeping the old format in these stores will default them to a very high cost infrastructure. But that’s a very fat chance of perfect overlap. In fact, it makes the most sense to run a chain of only 700 stores – so they logistically and structurally only have to serve stores that are converted. Otherwise these remaining assets will do nothing but weigh down the core.