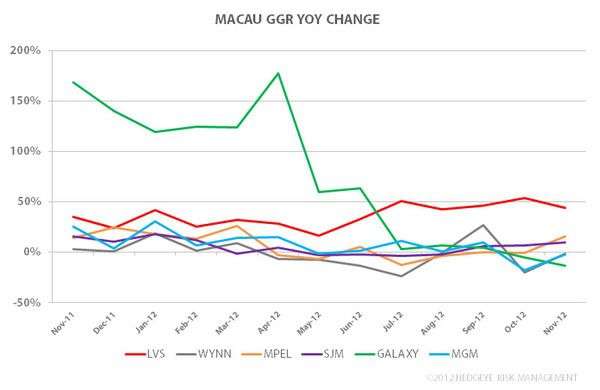

Gross gaming revenue (GGR) in Macau rose 8% in November on a year-over-year basis. Despite a tough hold comp, VIP hold appeared slightly below normal for this year but well below 2011 numbers. Mass revenue led the way, up 33%, while VIP revenue declined slightly for the second consecutive month. How did the Macau players fare?

Sands China (LVS) saw market share at 20.8%, up 15.6% year-over-year. GGR growth led the market and the mass business grew a whopping 75% year-over-year. Wynn (WYNN) struggled with GGR down 2% and mass hold up only 6%. MPEL saw GGR grow above average and mass share grew to 12.9%, an all-time high. MGM Resorts (MGM) had the worst month with market share barely rebounding from October’s 8.9% number and mass share was only 6.9%, nearly an all-time low. GGR fell for the second straight month at MGM.