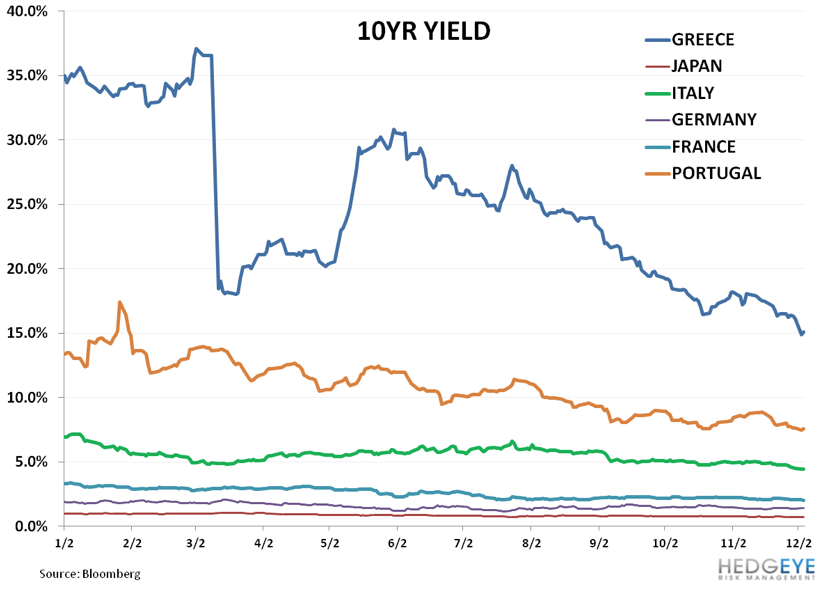

The sovereign debt crisis in the Eurozone has cooled off in the mainstream media lately, but the situation is far from being fixed completely. 10-year bond yields have declined significantly from the heightened levels experienced in June of this year. Greece, Portugal and Italy remain the biggest at-risk countries for investors and Germany and France continue to plow forward without any hiccups. Keep an eye on maturing debt for various countries in 2013 as some (particularly Italy) have nasty situations they must face.