This note was originally published at 8am on November 20, 2012 for Hedgeye subscribers.

“Time in truth, discovers everything.”

-Thales

Bertrand Russell once claimed that, “Western philosophy begins with Thales.” And while I am not so sure about that being the truth, Thales was closer to getting to my definition of the truth than most Greek philosophers – he used math.

“Thales used geometry to solve problems such as calculating the height of pyramids and the distance of ships from the shore. He is credited with the first use of deductive reasoning applied to geometry… he has been hailed as the first true mathematician.” (Wikipedia)

The aforementioned quote comes from a book I started reading this past weekend titled Pythagoras The Mathemagician (pg 87). Since we’re in the midst of a bull market in Old Media storytelling, I needed to suspend disbelief and consider magic too.

Back to the Global Macro Grind…

Yesterday was a hoot. On no-volume (21% below the average US stock market down day volume in November), the SP500 melted up +1.99% to 1386. That was the biggest up day since September 6th (+2.04%). Back above my TAIL risk line of 1364. Hoowah!

Let’s not talk about September though. That was a time when The Bernank’s stock market magic stopped. As a friendly reminder, inclusive of yesterday’s squeezage, the SP500 is still down -6% from the September 14th YTD high.

But why? What is the truth? Have stock and commodity markets been going down for 2 months only because of the #KeynesianCliff? Or did a few things related to economic gravity (growth and earnings) have something to do with it?

To review, our Top 3 Global Macro Themes for Q4 are as follows:

- Earnings Slowing

- Bubble #3 (Commodities)

- Keynesian Cliff

So, I’m not saying that Theme #3 doesn’t matter. I’m not saying that Bubble #3 doesn’t either (we re-shorted Oil on yesterday’s ramp, and bought Natural Gas). I’m simply saying what I always say – embrace uncertainty, because the global marketplace’s interconnected risks are much more encompassing than a manic media sound-bite about timing the cliff.

Back to reality. Now that Q312 Earning’s Season is winding down, per Darius Dale’s scorecard, what has Time & Truth told us about #EarningsSlowing?

1. Roughly 96% of the way through the Q3 earnings season, 58.7% of SP500 companies have missed on the top line and 30.7% have missed on the bottom line (478 total). That compares with 57.8% and 26.8%, respectively, in 2Q12. If the season wraps up as things currently stand, 3Q12 will have reported the lowest percentage of companies beating on the top line since 1Q09.

2. 72% of companies that have issued 4Q12 EPS guidance have issued projections below the mean EPS estimate. That compares with a ratio of 80% on the negative side at this time during the previous earnings season. Despite this improvement, we continue to warn that consensus estimates for 4Q12 and 2013 remain dramatically inflated relative to any reasonable economic GROWTH scenario.

3. Bloomberg consensus still has SP500 constituent EPS growing an average of +7.1% YoY per quarter over the NTM vs. +0.9% YoY in 3Q12 and a trailing four quarter average of +3.1% YoY. While down from a projected quarterly average NTM EPS growth rate of +9.9% YoY when we first called out consensus’ poor modeling technique back on OCT 8, we still contend these estimates remain out to lunch.

Out to lunch? Yes. As in no soup fo you Mr. Sell-Side consensus. It’s been a long year for you on GDP growth and earnings forecasts. Maybe we should just pretend those 2012 predictions didn’t happen. Long live Hyman’s 569 “global easings” instead.

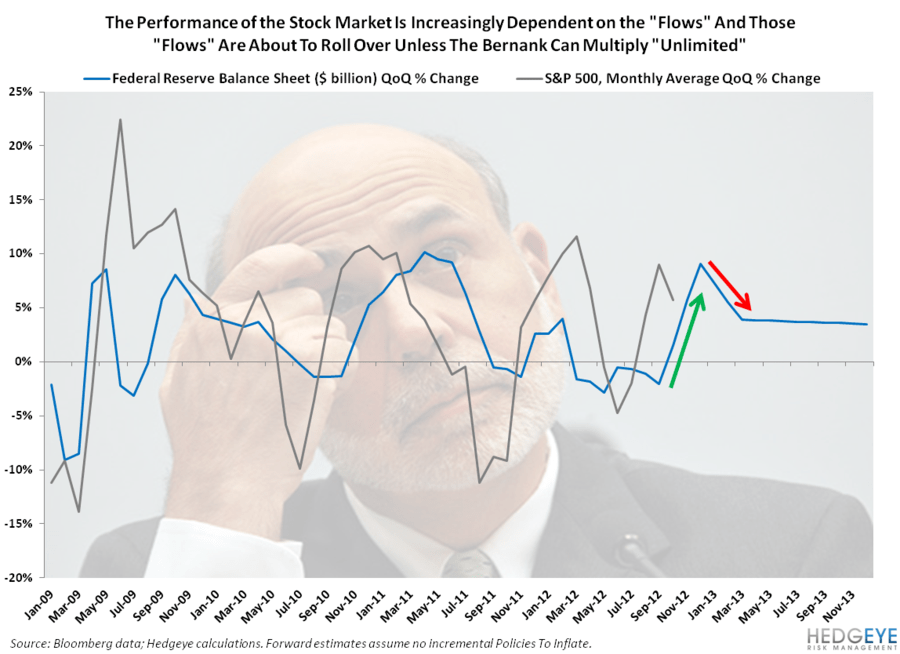

Money printing, of course, is not magic. The slope of growth in money supply is just math. If Bernanke doesn’t double or triple his monthly debt monetization soon, the slope of the Fed’s balance sheet will continue to slow. That’s bullish, on the margin, for the Dollar.

Perversely, in the immediate-term what’s good for the Dollar is bad for stocks. Part of yesterday’s fun times at no-volume high was that the US Dollar was having its biggest down day in 3 weeks. A -0.45% down day on the USD Index = a +2.8% up day for Basic Materials (XLB) stocks. Hooray.

Just a quick update on the Correlation Risk math (using 30-day correlations versus the US Dollar Index):

- SP500 = -0.90

- EuroStoxx600 = -0.85

- MSCI World Index = -0.89

- CRB Commodities Index = -0.84

- CRB Food Index = -0.79

- VIX = +0.44

In other words, yesterday’s rally to lower-highs (SP500 still down -1.8% for November after the +1.99% move) has nothing to do with what I called bullish in Monday’s Early Look (Food Deflation and Commodity Speculation Imploding). It had everything to do with the same old playbook the bulls who have confused stocks with the real-economic growth have been using all year.

Our immediate-term Risk Ranges (support and resistance) for Gold, Oil (Brent), Natural Gas, US Dollar, EUR/USD, UST 10yr Yield, and the SP500 are now $1710-1737, $109.96-111.35, $3.56-3.88, $80.69-81.39, $1.26-1.28, 1.49-1.64%, and 1364-1401, respectively.

Best of luck out there today,

Keith R. McCullough

Chief Executive Officer