TODAY’S S&P 500 SET-UP – December 3, 2012

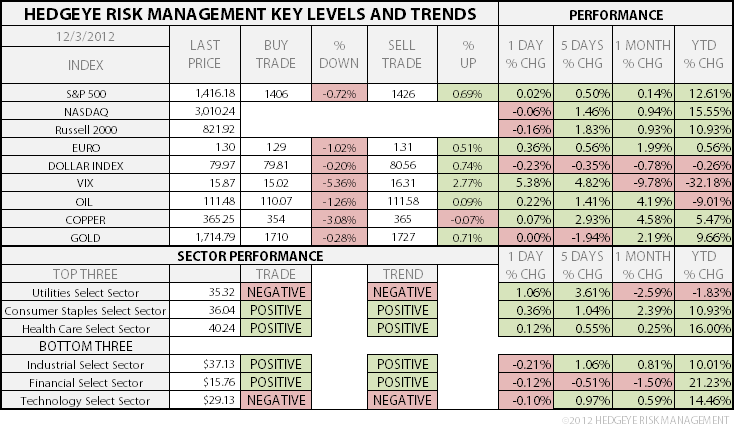

As we look at today's setup for the S&P 500, the range is 20 points or 0.72% downside to 1406 and 0.69% upside to 1426.

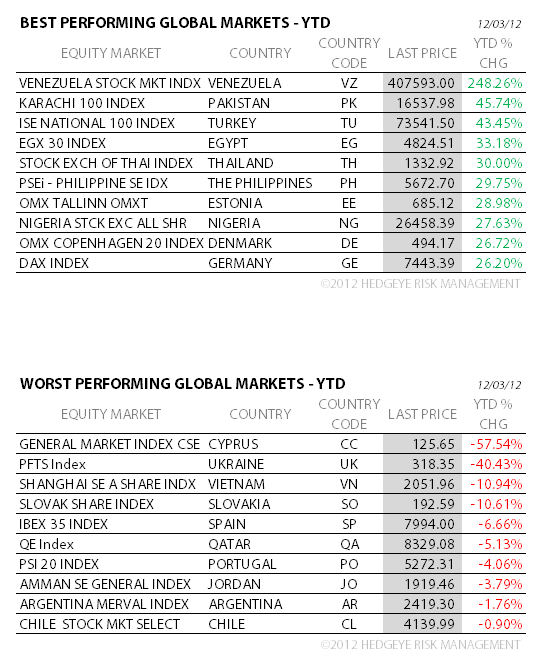

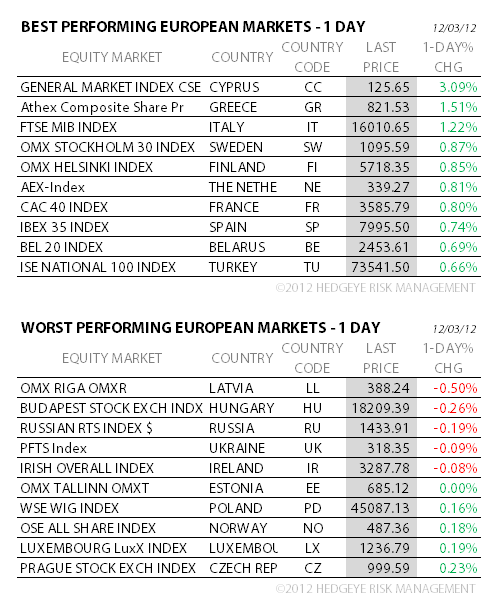

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.38 from 1.37

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Corelogic Oct. foreclosures

- 8:58am: Markit US PMI Final, Nov. est. 51.7 (prior 51.4)

- 10am: ISM Manufacturing, Nov. est. 51.5 (prior 51.7)

- 10am: Construction Spending, Oct. est. 0.5% (prior 0.6%)

- 11am: Fed sells $7b-$8b debt due 12/31/2015-1/31/2016

- 11:30am: U.S. Treasury to sell $32b 3-mo., $28b 6-mo. bills

- 12:15pm: Fed’s Rosengren speaks at New York Fed conference

- 1:40pm: Fed’s Bullard speaks in Little Rick, Arkansas

GOVERNMENT:

- House, Senate in session

- Secretary of State Hillary Clinton in Prague

- Democratic Governors to being 2-day conference in Los Angeles

- Federal Housing Finance Agency closes public comment on plan to create standardized system for issuing mortgage bonds

- U.S. High Speed Rail Association opens 3-day conference; to discuss California’s plan for $68b bullet train

WHAT TO WATCH

- Auto sales may have increased 12% in Nov. to highest monthly pace in 4 years

- Rupert Murdoch chooses WSJ editor Robert Thomson to lead publishing spinoff

- UBS said to be close to settlement over Libor-rigging

- EADS says talks on changes to shareholder structure are ongoing

- Starbucks in discussions with U.K. Treasury regarding taxes

- Health Management pressured doctors to admit patients to increase revenue, CBS’s “60 Minutes” reports

- Carl Icahn’s offer to buy Oshkosh expires at midnight; will drop offer if <25% of shares tendered by deadline

- Northrop, other defense contractors speak on fiscal cliff in DC

- Macau gambling rev. climbed 7.9% in Nov. vs est. 8%

- California may fine makers of mobile apps over piracy: San Francisco Chronicle

- North Korea continues plans to test long-range rocket, Japan says will shoot it down if deemed necessary

- Yahoo facing $2.7b non-final verdict in Mexico on charges related to a Yellow Pages listing service

EARNINGS:

- Conn’s (CONN) 7 a.m., $0.27

- Exa (EXA) 4:05 p.m., $0.08

- Casella Waste Systems (CWST) 4:30 p.m., $(0.09)

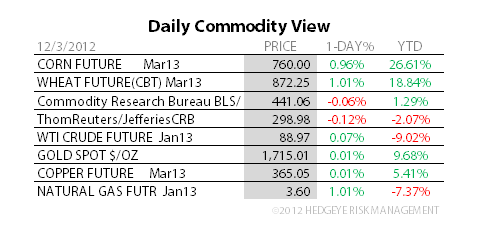

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Crude Trades Near Two-Week High as China Manufacturing Improves

- Hedge Funds Increase Bullish Bets Most Since August: Commodities

- Gold Gains as Physical Demand Improves After Price Decline

- Crop Futures Advance as Demand Increases Amid Supply Concerns

- Copper Swings Between Gains and Drops on Manufacturing Gauges

- Sugar Rises for Third Day on Lower Indian Output; Coffee Falls

- Rebar Jumps Most in Six Weeks on Chinese Manufacturing Data Gain

- Palm Oil Drops for Fifth Day on Indonesian Stockpile Concerns

- Oil Bulls Boost Bets as U.S. Economy Strengthens: Energy Markets

- Russia’s Grain Exports Fall 18% as Wheat Takes Smaller Share

- Auto Aluminum Gains on Steel Thanks to Tighter Fuel Standards

- Nickel-Ore Cargoes from Philippines to China Delayed by Storm

- Goldman Forecasts 7% Return on Commodities in a Year on Energy

- Rubber Climbs to Six-Week High as China Manufacturing Improves

CURRENCIES

USD – get the dollar right and you get most things beta right; last wk was the 2nd consecutive down wk for the Dollar (European and US stocks were up for the 2nd consecutive wk as the inverse correlation on a TREND duration remains close to -0.9 b/t USD and SP500).

EUROPEAN MARKETS

GREECE – thank goodness this is the bullish catalyst every Monday; after rallying last Monday on whatever the news was, Greek stocks closed the wk down -4.2%, but rally +1.3% to another lower-highs on this morning’s funny money news. Net net, the Athex is down -8.2% from the OCT lower-high.

ASIAN MARKETS

CHINA – the Chinese get it; Washington update: Geithner’s “deal” includes changing the rules on the Debt Ceiling (rising debt) and raising, not cutting, “stimulus” spending; Shanghai Comp dropped another 1% to a fresh YTD low before the Greek “news”; China crashing again (-20.4% from the March global #GrowthSlowing peak).

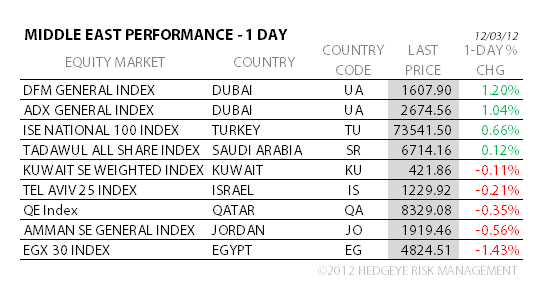

MIDDLE EAST

The Hedgeye Macro Team