This note was originally published at 8am on November 19, 2012 for Hedgeye subscribers.

“Together we build.”

-Henry Kaiser

In 1941, “the experts predicted it would take Bedford, McCoon, and their teams six months to build up enough solid ground before they could begin work in the shipyard. It took Kaiser’s men exactly 3 weeks.”

“There was a race … between the Kaiser draftsmen and the field people as to whether we could build it first or the engineers and architects could draw it first.” (Freedom’s Forge, page 131)

That was during WWII. We are in a very different kind of war now – a globally interconnected economic one that is dominated by compromised politicians and theoretical Keynesian draftsmen – but it is a war we free-market libertarians can still win. We, the field people, need to lock arms and build a new foundation for global growth. There’s only 1 big one that we have not tried.

Back to the Global Macro Grind…

The difference between us and them is that we believe in a Strong Dollar providing the foundation for a Strong America (1983-1989 and 1993-1999) and a stronger global consumption economy at large.

They have always believed that a weak US currency would drive “strong exports.” We believe that a weak currency drives global food, energy, and cost of goods inflation – that, in turn, slows real (inflation adjusted) global economic growth.

With the US Dollar up for 8 of the last 9 weeks, if the SP500 can re-capture my long-term TAIL line of 1364, together, we can build upon 2 very bullish economic developments:

1. Food Inflation is deflating

2. Institutional Commodity gambling is imploding

With the US Dollar up +0.2% last week to $81.26, the Euro continued to weaken and the Japanese Yen got slammed for a -2.2% wk-over-wk decline. Japan is channeling its inner-Krugman (1997 “Print Lots of Money) by attempting to do what the USA did at the Bernanke Top (print money, juice stocks, and eventually fizzle out at another 20yr lower-high in the Nikkei).

Back to Food Deflation last week (and from Bernanke’s Top, 2 months ago):

- Wheat = down another -5.5% week-over-week (-7% in the last 2 months)

- Soy = down another -4.7% week-over-week (-20% in the last 2 months)

- Coffee = down another -1.7% week-over-week (-19% in the last 2 months)

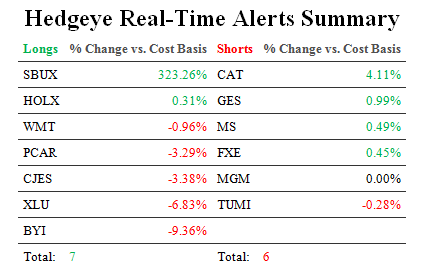

If you eat carbs and drink coffee every morning, that’s good. And it’s really good for the likes of our Top 2 Global Consumption long ideas right now (Starbucks, SBUX and Walmart, WMT) too.

Forget about the USA’s politicized class warfare thing. When you deflate food prices, you save money for at least 99% of the world’s 7,053,206,438 people. With taxes going up on the some-of-us, I like tax cuts like that for the all-of-us.

If you’ve been living large long Oil futures contracts since 2009, you may not like how this story ends. If you’ve been shorting food and energy since September, you are smiling.

Here’s a look at how Institutional Commodity Gambling (CFTC futures/options contracts) is imploding:

- Net long contracts (bets on commodity inflation) = down another -17% last wk to 772,512 contracts

- Bullish Commodity bets are now crashing, down -42% from the Bernanke Top (SEP14, 2012)

- Crude Oil contracts = down another -18% last week (despite Israel/Gaza) to 100,021

- Farm Goods = down -22% last week to 415,498 contracts

- Corn (biggest component of the Farm Goods basket) = down -14% wk-over-wk to 202,853 contracts

- Copper joined Cotton as the 2nd major commodity to move into a net SHORT position

Since I won large in Vegas last week ($736 bucks!), I’ll bet my whole lot that at least 1/2 of institutional investors reading this note will call what I just outlined as a bullish contrarian indicator. On the margin (immediate-term TRADE duration) that’s probably right.

But, as you move out from intermediate (3 months or more) to longer term durations (TREND and TAIL), averaging down into a wildly volatile asset class like commodities can put perma-commodity bulls out of business, fast. So be careful.

From an asset allocation perspective, the most asymmetric long-term risk to all of Global Macro continues to be Strong Dollar. If it manifests itself into the mid-to-high $80 levels (US Dollar Index), you haven’t seen anything in terms of commodity deflation yet.

While it may sound perverse to call deflation bullish, it’s not. Letting free-market prices clear without fiscal and/or monetary price supports is the only big idea we have not tried for the last decade.

I think it’s the only way We Build sustainable consumption growth in both the US (71% of GDP) and global economy. Get the Dollar right, you’ll get long-term growth right. If you want to know how I get bullish on the economy, look no further than that.

Our immediate-term Risk Ranges (support and resistance) for Gold, Oil (Brent), US Dollar, EUR/USD, UST 10yr Yield, and the SP500 are now $1704-1723, 106.12-109.98, $80.87-81.45, $1.26-1.28, 1.49-1.64%, and 1335-1364, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer