“You want a prediction about the weather? You’re asking the wrong Phil. I’ll give you a winter prediction: It’s gonna be cold, it’s gonna be grey, and it’s gonna last you for the rest of your life.”

-From the film Groundhog Day

I used the quote from Groundhog Day because as an analyst covering Europe the political and economic developments of the region continue to repeat and there appears no simple solution to solving its ails – headline risk is here to stay.

If Greece headlined the film by taking its first bailout in May of 2010, it was quickly joined by the peripheral actors of Portugal, Spain, Italy, and Ireland – and each and every time the scene repeated: a crisis deepened, Eurocrats (European politicians) responded by calling a summit, announced a solution, the solution did not have “teeth” or didn’t work, and risk expectations shifted as the movie played on.

Monday’s Greek aid deal is part of the same film. The main tenants of the “deal” include a payment of its next bailout tranches (€43.7B); approval to reduce its debt as a percentage of GDP to 124% by 2020 (versus estimates of 190% in 2013); both a reduction in interest rates on loans and extension in loan maturities and interest payments (by as much as 15 years!); a pass-along of €7B from profits on ECB Greek debt holdings to Greece; and a potential (undetermined) debt-buyback scheme.

Yet what’s most unsettling is that market participants recognize this deal for what it is: a shell game. After all there’s no prospect of this being the last bailout or concession thrown Greece’s way.

But can Eurocrats get away with playing the game? And where is the region politically and economically going now that it officially slipped into recession, with Eurozone GDP declining -0.1% in Q3 quarter-over-quarter following a -0.2% contraction in Q2? Here are some assumptions we’re working under:

- Eurocrats will do everything in their power to maintain their own job security and therefore will continue to support the region monetarily

- There’s nothing in the main constitutional treaties to allow a member state to exit the Eurozone or be expelled. Therefore we do not expect Greece et al to leave or be forced out over the next 1-3 years

- When it comes to ‘hard’ decisions or impasses, Eurocrats will chose the path of least resistance (a strong argument for keeping the region together remains the fear of a breakup), which should prolong a return to growth

- Fiscal consolidation (austerity) is needed across much of the periphery; governments have recently taken the flawed stance that they need to take their foot of the gas. Instead what’s needed is more manageable consolidation expectations and strategy to reform labor markets to improve growth prospects

- A Eurozone governed only by monetary policy is not feasible for long-term sustainability

- The path to a Fiscal Union is littered with challenges given the inability of states to relinquish their sovereignty to a European commission

- Fellow member states represent the largest trading partners for most states, therefore no one state will see a major inflection in growth until the region collectively improves

- France, the second largest economy in the Eurozone, and once a close political ally to Germany via Merkozy, has inflected alongside the election of the Socialist President Hollande. His 75% tax policy on the rich, among others, will be a headwind as the country’s sovereign debt tips past 90% of GDP and France loses its AAA status. All this bodes poorly for Eurozone bailout structures built around the credit rating of the larger economies and given that France is the second largest contributor behind Germany.

Draghi’s Unlimited

Despite the region’s challenges, one cannot forget ECB President Mario Draghi’s September announcement that “the ECB is ready to do whatever it takes to preserve the euro” via the Outright Monetary Transactions (OMT) program to buy sovereign bonds.

To date the facility has not been triggered, however sadly market operators are left to manage risk around the bubble of Big Government and Central Bank Intervention. It’s this market reality that solidifies our thinking that Eurocrats will do all that is necessary to maintain the Union; has kept the EUR/USD trading in a relatively tight band and eliminated the euro parity crowd; and caused sovereign bond yields to moderate in recent months and new issuance to be priced at lower yields versus previous auctions.

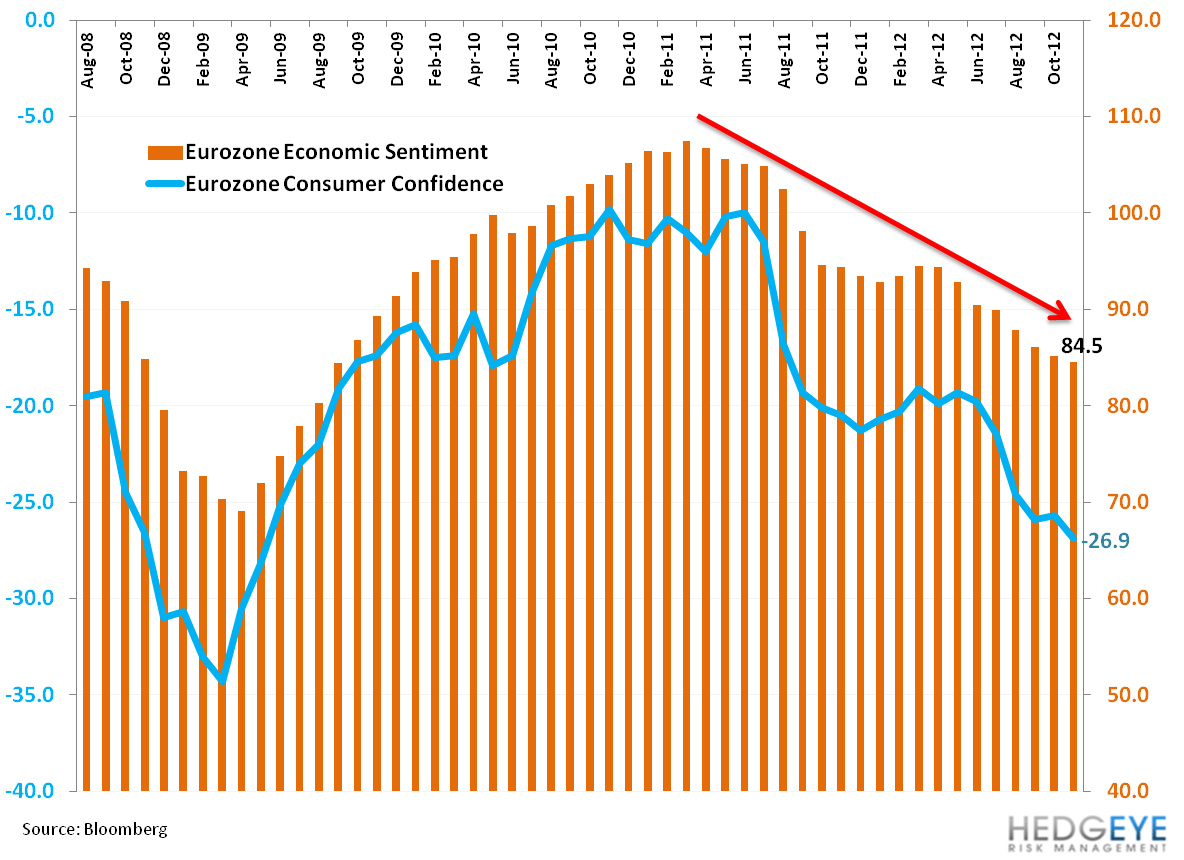

This is all positive but hinges on Draghi suspending economic reality over the long term, and is a mismatch with Eurozone fundamental indicators that continue to move in the wrong direction: PMI Services and Manufacturing figures remain grounded below 50 representing contraction; economic, business, and consumer confidence figures have been down for 7-8 straight months; Retail Sales and Industrial Production remain challenged in the core and bombed out in much of the periphery; and inflation is sticky and above the ECB’s target.

Tipping Points

On the downside we’d caution that there is measurable risk still imbedded in Spain (the sovereign) needing a bailout, which could accompany a need for assistance in Italy. Further, a rise in foot power, namely strikes and riots, especially given outsized unemployment rates across the periphery, and push back on austerity could turn both the political and economic tide in the Eurozone.

Remember, just two weeks ago there was the first ever coordinated strike against austerity of 40 unions across 23 countries. In addition, a recent Greek popular poll showed that the anti-bailout Syriza party leading, and regional elections in Catalonia, Spain over the weekend voted in a majority of secessionist parties, all suggesting that there’s risk in reaching a tipping point should we see more concentrated popular push back on government policy and Eurozone membership.

While we don’t expect to see borders shifting in the Eurozone anytime soon, citizens have a way of viewing shell games for what they are: deception.

Our immediate-term Risk Ranges for Gold, Oil (Brent), Copper, US Dollar, EUR/USD, UST 10yr Yield, and the SP500 are now $1, $107.94-111.49, $3.45-3.58, $79.95-80.61, $1.28-1.30, 1.56-1.68%, and 1, respectively.

Matthew Hedrick

Senior Analyst