TODAY’S S&P 500 SET-UP – November 28, 2012

As we look at today's setup for the S&P 500, the range is 36 points or 1.14% downside to 1383 and 1.43% upside to 1419.

SECTOR AND GLOBAL PERFORMANCE

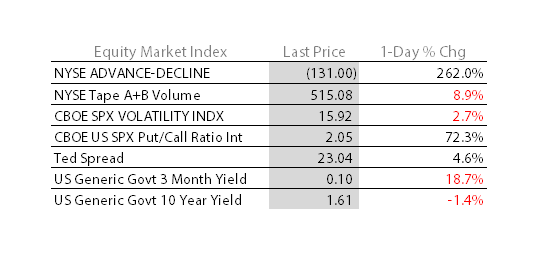

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.35 from 1.38

- BONDS – you can love to hate them on “valuation”, or just buy them on dips and smile into yr end; UST 10yr yield makes another lower-high last wk, dropping to 1.62% (from 1.69% at the start of the wk); no support to 1.55%.

MACRO DATA POINTS (Bloomberg Estimates):

- 7am: MBA Mortgage Applications, Nov. 23 (prior -2.2%)

- 10am: New Home Sales, Oct. est. 390k (prior 389k)

- 10:30am: DoE inventories

- 11am: Fed to buy $1.75b-$2.25b notes due 2/15/36-11/15/42

- 12:15pm: Fed’s Tarullo speaks in New Haven

- 1pm: U.S. to sell $35b 5Y notes

- 2pm: Fed’s Beige Book Economic Survey

GOVERNMENT:

- House, Senate in session

- President Barack Obama, House Speaker John Boehner hold meetings with Goldman Sachs CEO Lloyd Blankfein, other business leaders to discuss fiscal cliff

- Pandora CEO Joseph Kennedy to testify at music-licensing hearing by House subcommittee

- U.S. will auction ~3.8k blocks covering about 20.5m acres off Texas coast in western Gulf of Mexico, first sale of oil, gas exploration leases under Obama administration’s five-year plan for developing Outer Continental Shelf

- Ex-BP Plc vice president, two former well-site supervisors arraigned on criminal charges for actions after 2010 oil spill

- Treasury holds meeting of President’s Advisory Council on Financial Capability, with Undersecretary for Domestic Finance Mary Miller, 8am

- House Energy and Commerce panel holds hearing on waste, fraud and abuse in Medicare, 10am

WHAT TO WATCH

- Fed said to weigh forcing foreign banks to boost capital in U.S.

- Goldman’s Blankfein among 13 CEOs meeting with Obama today

- Groupon board said to consider CEO change amid growth slowdown

- Costco to pay out $3b with $7/shr special cash div.

- Smith & Nephew buys assets of Healthpoint Bio for $782m cash

- Google said to oppose consent decree in any FTC antitrust deal

- Samsung says IPhone relies on patented technology in U.K. trial

- BP seen paying billions more in oil spill claims after deal

- Hewlett-Packard’s war of words escalates with Autonomy’s founder

- Tobacco companies must admit lying on products, U.S. judge rules

- Obama urged to declare emergency as Mississippi water levels ebb

- Fiscal-cliff pressure is on for cuts to entitlement programs

EARNINGS:

- Fresh Market (TFM) 6am, $0.26

- Jos A Bank Clothiers (JOSB) 6am, $0.56

- Yingli Green (YGE) 6:07am, $(0.61)

- CGI Group (GIB/A CN) 6:30am, C$0.42

- JA Solar (JASO) 6:33am, $(0.21)

- Express (EXPR) 7am, $0.17

- Suburban Propane Partners (SPH) 7:30am, $(0.91)

- ANN (ANN) 8am, $0.74

- American Eagle Outfitters (AEO) 8am, $0.39

- Golar LNG Partners (GMLP) 8:30am, $0.56

- TiVo (TIVO) 4pm, $(0.24)

- Aeropostale (ARO) 4:01pm, $0.29

- Guess? (GES) 4:03pm, $0.44

- Semtech (SMTC) 4:30pm, $0.43

- Pall (PLL) 5pm, $0.66

- Workday (WDAY) Aft-mkt, $(0.49)

- Post Holdings (POST) Aft-mkt, $0.35

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Oil Trades Near One-Week Low on Supply Gain, U.S. Budget Concern

- DuPont Sends in Former Cops to Enforce Seed Patents: Commodities

- Gold Declines for a Third Day in London on Improving U.S. Data

- Olam Says No Insolvency Risk as It Rebuts Muddy Waters Claims

- Copper Declines on Concern About Progress of Fiscal-Cliff Talks

- U.S. May Double Soybean Exports to Russia After Obama Signs Law

- Soybeans Drop From Two-Week High as South American Concern Eases

- Sugar Falls as Harvesting Progresses in Brazil; Cocoa Declines

- Copper Demand in China to Improve Next Year, Aurubis Says

- India Iron Ore Dilemma May Reshape Seaborne Market: Outlook

- Coal Heads for Best Quarter Since 2010 on Cold: Energy Markets

- Larger Gold Miners Outperform Metal; Smaller Rivals Trail

- Copper Faces Resistance in London at $7,865: Technical Analysis

- Iranian Tanker Leaving Greek Island After Cargo Investigation

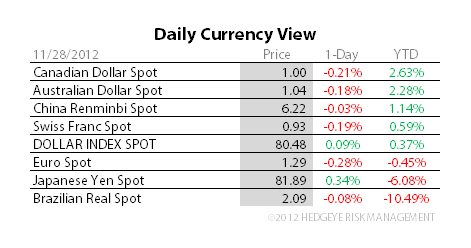

CURRENCIES

EUROPEAN MARKET

RUSSIA – the RTSI is beating the Chinese to the crash table this morning, down -1.2%, breaking the -20% barrier again for the 2nd time since September; Oil (Brent) failed at our long-term TAIL line of $111.48 resistance and there’s a commodity bubble unwinding.

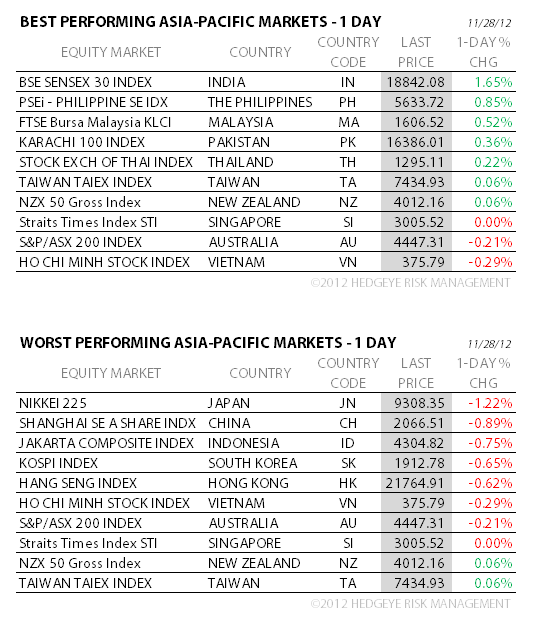

ASIAN MARKETS

CHINA – moves to within a hair of crash mode overnight (Shanghai Comp down another -0.9% to 1973 = -19.9% from its March #GrowthSlowing top); remember our baseline 3-factor model on global growth: China/Copper/BondYields.

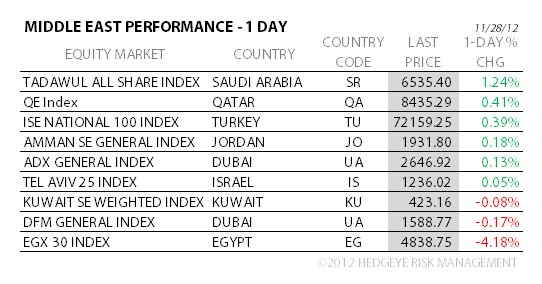

MIDDLE EAST

The Hedgeye Macro Team