We added CRI on the short-side of our Real-Time Positions on green today. This is one of our core short ideas and one that we see with 20%-30% downside from current levels.

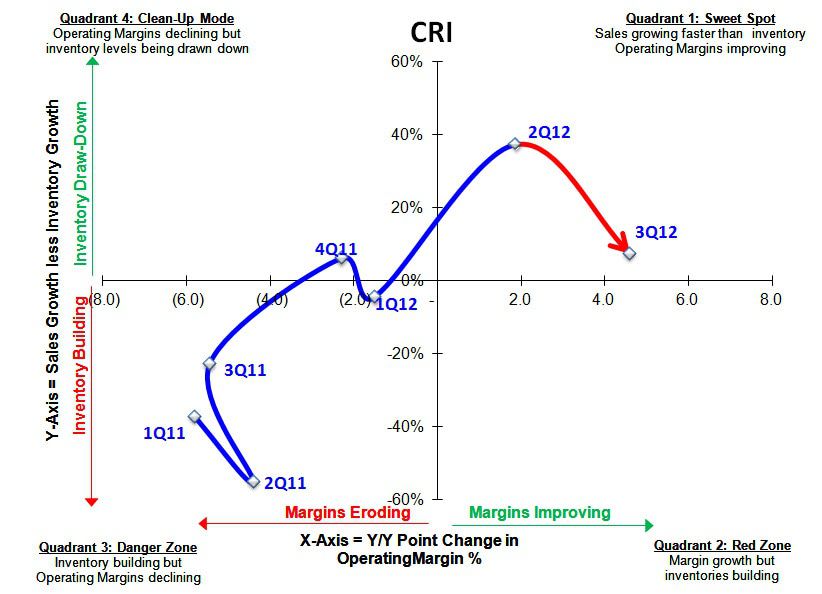

We went into 3Q (10/25) and outlined in our CRI Black Book on 10/15 that we didn’t expect a miss due to an inflection in margins (i.e. product costs turn favorable), but that we expect the reality of our thesis – lack of product differentiation and increasing competition resulting in pricing/margin pressure – to play out more visibly in Q4 and into 1H F13. We had investors short the bounce on earnings and Keith is doing the same here today on lower highs.

In short, we think there is a disconnect between what management (and investors) think margins can get to and what will ultimately transpire. There’s a full 3pt spread between our margin estimates and consensus. Wholesale revenues just turned negative for the first time in 9-quarters and retail comps remain a concern with underlying (2yr) Carter’s and OshKosh comps decelerating with a tougher setup ahead over the next 2 quarters. With price increases no longer holding (a new development as of 3Q call), we think the lack of product differentiation/ segmentation will prove margin expectations overly optimistic.

To request our detailed CRI Black Book with complete analysis, please contact .

CRI Setup by Duration:

CRI Risk Management Levels:

CRI SIGMA is starting to roll: