"The farther backward you can look, the farther forward you are likely to see."

-Churchill

If you think it’s more progressive to look forward than backward, we should take a walk in the bush together on Northern Ontario right before the black bears go into hibernation. My Dad and I recommend keeping your head on a swivel.

Looking back at sovereign debt cycles (Reinhart & Rogoff go back to the year 1500) helps us look forward at how ridiculous expectations are that Greece is going to be fixed.

I couldn’t make this up if I tried this morning, but this is what Greece Prime Minister, Antonis Samaras, had to say about the latest Greek debt deal: “A new day begins for all Greeks!”

Back to the Global Macro Grind…

A new day in storytelling it is. World Equity markets initially rallied on the Greek “news”, then reversed, and quickly. Chinese stocks closed down -1.3% making fresh new lows, Greek stocks went from +1% to -1.5%, and US Equity Futures went from green to red.

If you’ve never played a shell game, this is how it works: now you see it, now you don’t. Here’s an abbreviated version of the Greek debt deal: €40B in debt is evaporated, then they get a fresh €44B in bailout debt within the next few months (€34.4 billion paid out in Dec and €9.3 billion in Q1 linked to MoU milestones agreed by Troika).

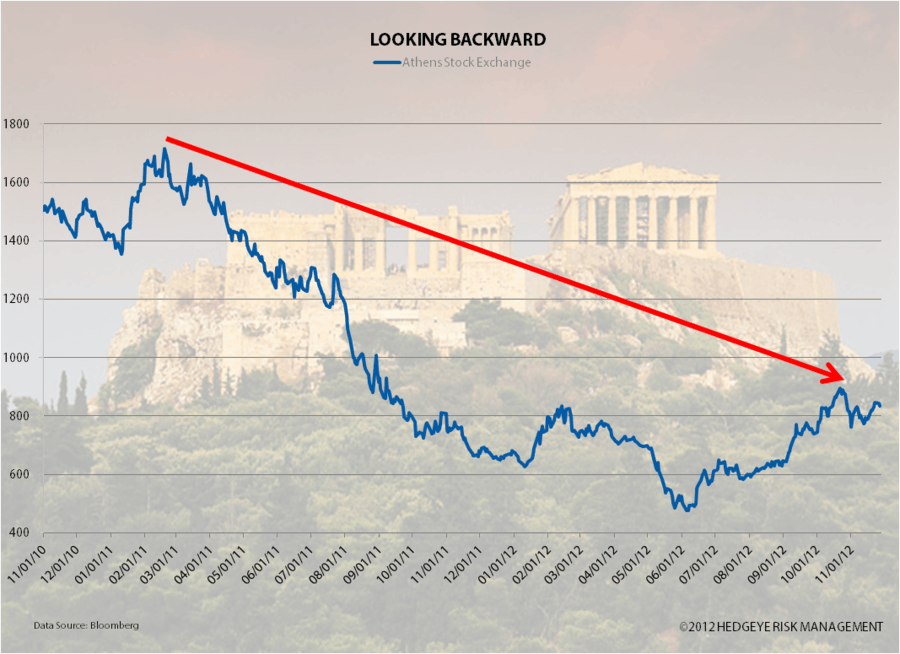

Great. Right? Yeah, just great. For those of you still looking backwards as you attempt to proactively risk manage forward, you can see what all this Greek noise has added up to over the years in Josefine Allain’s Chart of The Day:

- Greek stocks -1.5% on the news to 831 on the Athens Stock Exchange Index

- Greek stocks -7% from their lower long-term highs in October (894 on the Athex)

- Greek stocks -49% from the lower highs they established 2 years ago (November 2011)

To be fair, 2 years ago requires a decent look back. And, admittedly, I forget what the bailout rumors on Greece were 3 years ago. All I know is that whatever the rumors were, they were lies.

Martin Luther King, Jr. said “a lie cannot live.” And, if you have the risk management mandate to look forward far enough, that’s generally an accurate mean reversion assumption to make.

But, if you have an investment mandate to chase weekly and monthly performance bogeys, you’re probably ok to suspend disbelief and pretend the lies are realities. I read my kids fairy tales at bedtime too.

Reality: if you bought Greece (Athex Index) or Apple (AAPL) in November 2011 or September of 2012, you need to be up +96% and 19%, respectively, to get back to break-even. That’s just math.

Ultimately, betting on more of what has not worked (more debt financed government spending) is destroying the world’s long-term equity capital. That’s why I am wedded to looking back at LOWER-HIGHS in long-term prices. While this is a relatively new phenomenon to those who got plugged buying American or Greek stocks in 2007-2008, it’s been happening in Japan for 20 years.

Back to China (and Global #GrowthSlowing)…

Evidently those who were suggesting “China has bottomed” a few months ago were a little off on the timing. Last night’s -1.3% smack-down in the Shanghai Composite puts China 90 basis points away from going back into crash mode.

A crash, by our risk managed definition, is a price that’s made lower-highs on the order of 20% or more. Try it at home with your own money. I can promise you it will feel like what I just called it.

The Shanghai Composite is down -19.1% since #GrowthSlowing started, globally, in March of 2012. While it’s fun for passive Captain Stock Picker to talk about what the Dow is “up year-to-date”, real money that’s managed from a global macro perspective has been seeing lower-highs in prices in pretty much everything that matters since the March-April 2012 highs.

Here’s one really simple 3-factor Hedgeye Global Macro Growth Model to beam up onto your globally interconnected screens:

- CHINA (Shanghai Composite in a Bearish Formation = bearish TRADE, TREND, and TAIL)

- COPPER (Bearish Formation as well, down -11% from its Q112 lower-high)

- BONDS (US Treasuries in a Bullish Formation as Bond Yields are in a Bearish Formation)

Now, if my #OldWall competition wants to tell me that China, Copper, and Bond Yields are flashing a “back to growth” global economy, I’m happy to debate them live anywhere, anytime. Looking Backward, they’ll be forewarned that the Thunder Bay Bear will hold them accountable for missing the 2012 US and Global Growth slowdown just like they did in 2008.

Our immediate-term Risk Ranges (support and resistance) for Gold, Oil (Brent), Copper, US Dollar, EUR/USD, UST 10yr Yield, and the SP500 are now $1, $109.91-111.48, $3.43-3.56, $80.05-80.61, $1.28-1.30, 1.54-1.68%, and 1, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer