This note was originally published November 15, 2012 at 14:28 in Retail

Apparel retailers are reverting to a margin mean this quarter to an extent that we have not seen in years. As our SIGMA analysis shows, we’re seeing margins revert to zero barrier for many of the larger players oferall, with resulting in flex in the level of inventory relative to sales. The ups the ante for the level of sell-through that is necessary headed into the holiday season.

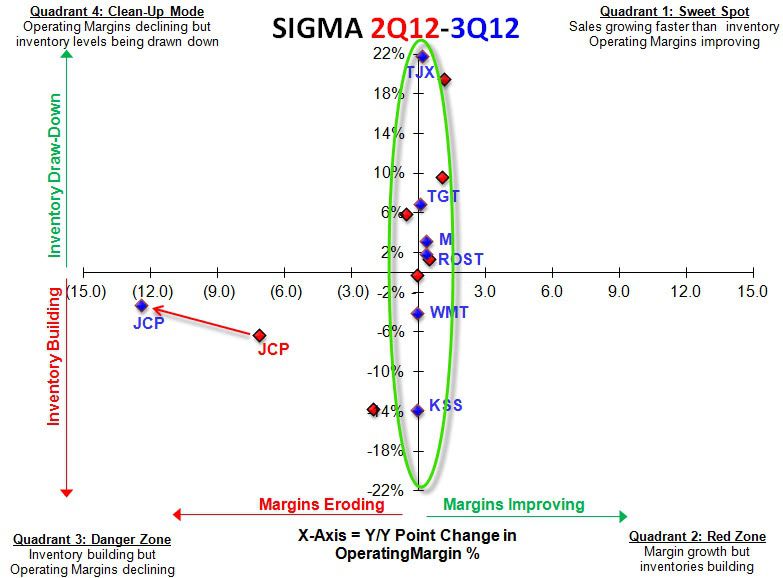

Our SIGMA charts below will look familiar to most, but for those new to this representation of fundamentals it triangulates the sales/inventory spread (i.e. sales growth minus inventory growth) on the x-axis as well as the year-over-year change in operating margin on the y-axis. Company’s want to be in the upper right (sales outpacing inventory growth with expanding margins) not the bottom right though directional moves within the same quadrant are often more important indicators for future outcomes and when stocks often have the most meaningful moves.

Consider the following:

- Mid-tier companies are at a collective inflection point re margins headed into 4Q. In fact, with all but JCP posting less than a +/- 40bps delta, variation in the yy change in margins is the tightest we’ve seen in over 4-years suggesting the likelihood for increased EPS volatility this holiday season particularly in light of top-line compression, or margin give up to support the sales gain.

- Our thesis on GPS and M is that the second JCP stops hemorrhaging sales at its current run-rate, it will put incremental pressure on these companies that have been gaining share. If JCP fails to recover – ever (which we think is unlikely) – then that’s bullish for M and GPS. We think in 1-2 quarters JCP’s delta will improve on the margin, and while still bad for JCP, will hurt its peers.

In light of this setup within this mid-tier(ish) space, we like M, GPS, and KSS (post 4Q) on the short-side and WMT long. In other segments of retail, we continue to favor the athletic space (NKE, FINL, FL) as it has such a positive tailwind in the form of a company R&D driven product and marketing cycle.