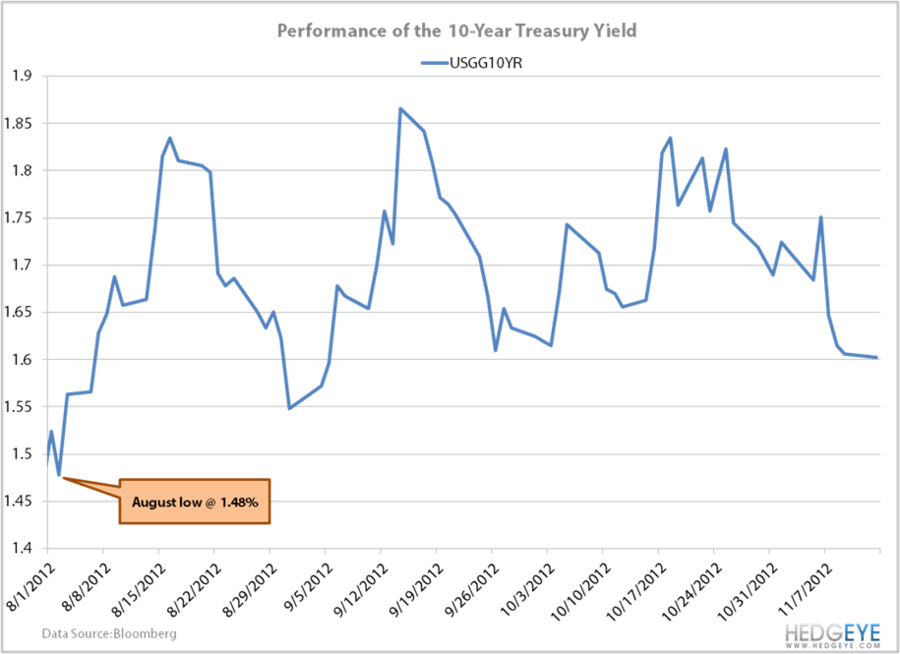

The 10-year Treasury yield is currently hovering around 1.58%, nearing the August 2012 low of 1.48%. As growth continues to slow and the stock market weakens, investors are buying up Treasuries like it's going out of style. If the S&P 500 can't hold 1364, look for the 10-year to get pushed even lower.