Down The Chain: CAT Dealer Results & Thesis Update

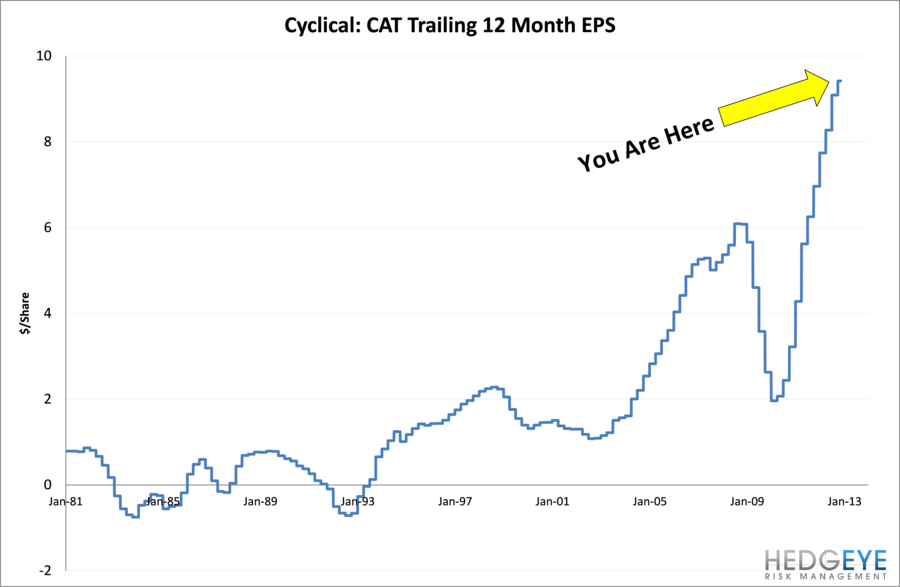

We continue to think that Caterpillar’s results are at or near a cyclical peak driven by recent bubble-like capital investment by basic resources companies. Importantly, we see ongoing evidence suggesting that the cycle has turned and will remain weak for a prolonged period. Dealer results, discussed below, add to our concerns. Consensus estimates for 2013 have declined significantly since our 9/14/2012 Black Book and the share price is lower. While this leaves us a little less bearish, we see continued downside. In our view, there are less risky investment opportunities on the equipment side in Paccar, and in the sector more broadly in FedEx.

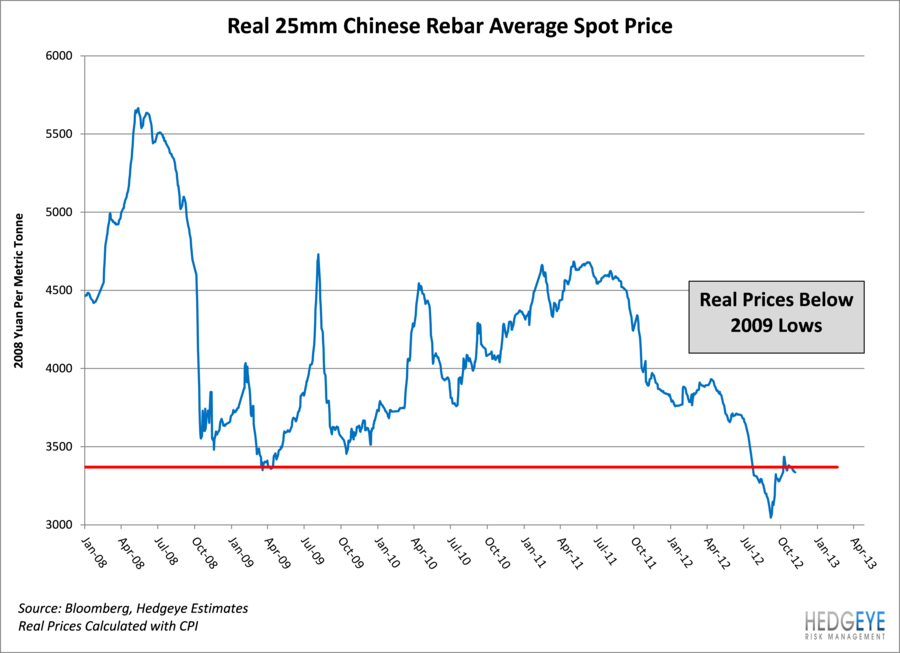

Recent improvements in Chinese data suggest that its economy is in a bottoming process (see work by Darius Dale and Hedgeye Macro team). While this may be the case, land sales by area are still down a mid-teens percentage YoY. Local metals prices point to ongoing weakness in Chinese construction, a key end-market for mining. Chinese average real rebar prices have lurched back below their 2009 lows in recent weeks.

Deep Cyclical

Caterpillar is a capital equipment supplier to highly cyclical end-markets, especially mining. Capital spending at cyclical companies tends to be more cyclical than the top-lines themselves. Considering this, buying into an earnings peak at CAT seems like a mistake. Down cycles can be long-lived.

Estimates Up & To The Right

Consensus tends to simply extrapolate recent results higher. While this forecasting method is unlikely to work well for most companies, the results are particularly inaccurate for cyclicals. Currently, estimates extrapolate near-peak results. Taking a multiple of estimated earnings is not a robust valuation approach, in our view.

Dealer Results Look Like CAT’s Results

CAT’s backlog declined during the past two quarters, supporting reported sales and profits relative to orders. Implied orders in 3Q 2012 were at the lowest percentage of trailing sales since the financial crisis. Orders tend to lead deliveries and revenues for obvious reasons. Interestingly, the quantity of long-term orders as a percentage of total backlog at CAT has also nearly doubled from 13.4% in 4Q 2011 to 22.5% at the end of 3Q 2012. That suggests orders might be at risk of cancellation as customers exercise delay options, in our view.

CAT Dealer Orders Deteriorate

Caterpillar dealers have served the company well over the years and have carved out a nice return for themselves in the process. A number of dealers are public, allowing insight directly into customer activity. Recent results suggest that end-user order activity has declined significantly. CAT management has said that “end-user demand” is more robust than current CAT orders based on dealer deliveries. However, this seems somewhat misleading because dealer deliveries lag dealer orders. CAT’s comments imply that revised 2012 and 2013 guidance is the product of dealer inventory adjustments and Caterpillar orders will soon return to high levels (“end-user demand”). From CAT’s 3Q 2012 10Q:

“Dealer reported new machine inventory increased about $400 million during the third quarter of 2012 compared with an increase of about $675 million during the third quarter of 2011. Dealer machine inventories at the end of the third quarter of 2012 are higher than historic averages relative to dealer deliveries to end users. Dealers have substantially lowered order rates below machine deliveries to end users, which we expect will result in dealer inventory reductions in the fourth quarter and continue into 2013. As a result of the anticipated reductions in dealer inventories as well as global economic conditions that are weaker than previously expected, we are lowering production in many facilities around the world. Lower production levels will continue until inventories decline and dealer order rates increase and are more in line with end-user demand.” – CAT 3Q 2012 10Q Page 57

However, implied order activity at the dealer level in the results we have seen suggest that end-user demand has weakened significantly. Backlogs have come down at the dealer level, too, sustaining current deliveries. Dealers do appear to have too much inventory, but they also appear to have suffered a significant order decline. That one/two punch will further push down CAT 2013 revenue and profit estimates, in our view.

Finning: New Equipment Implied Orders Down 45% YoY in 3Q 2012

Finning, like Caterpillar, drew down backlogs last quarter. Backlogs for new equipment fell from $1.7 billion to $1.4 billion, with sales in the quarter at $723 million. Implied orders were only ~$423 million in 3Q 2012 vs. ~$760 million in 3Q 2011, a 45% drop, by our estimates.

[The] Company is focused on reducing uncommitted inventory levels and prudently managing working capital.” – Finning 3Q Filing

Wajax: Oil, Gas and Mining Weakness

Wajax is a smaller Canadian dealer than Finning and has shown similar business trends. The company noted weakness in oil and gas orders, which was of particular interest since many investors expect this area of CAT’s business to hold up well.

“Overall backlog declined primarily as a result of a reduction in customer orders in the mining and oil and gas sectors…While the number of outstanding quotes for mining equipment continues to be significant, customers have been delaying their purchasing decisions in the face of lower commodity prices…Looking forward we expect softness in the oil and gas and mining sectors to continue into 2013.” - Wajax 3Q 2012 Release/Filing

The Bull Story at Sime Darby: It’s Just Like the 2009 Global Financial Crisis (?)

In a recent presentation, Sime Darby, an Asia-based conglomerate with a large CAT dealer network, suggested that the current situation was similar to 2009. We disagree, since the present environment looks nothing like 2009. In 2009 the order decline was driven by a global financial crisis, which is absent today. The current order declines have been driven by underlying market weakness following a decade of over-investments, in addition to stimulus spending roll-off, in our view.

Sime Darby reports in late November, and we will be interested in the results and will look for updates to this bull rationale.

Jay Van Sciver, CFA

Managing Director

HEDGEYE RISK MANAGEMENT

120 Wooster St.

New York, NY 10012