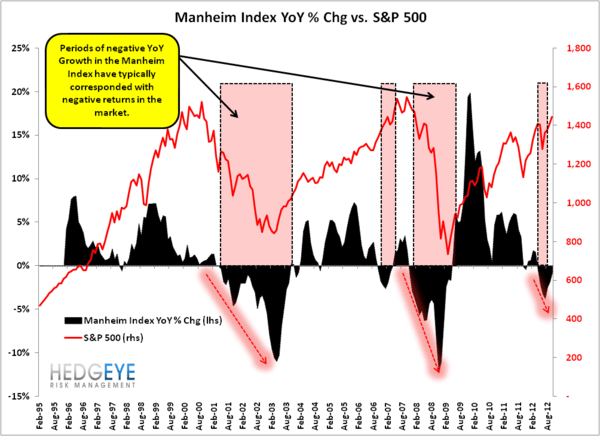

The Manheim Index of Used Car Values rose in October by 1% on a month-over-month basis, an improvement but is still trending negative on a year-over-year basis. As of November 1, new vehicle inventory levels have been below 60 days (on a 12-month rolling basis) for the longest period ever. Low inventory in new auto sales means there’s a strong market there, putting pressure on used car sales.

Why do used car sales matter? Because the Manheim Index historically correlates closely to the S&P 500 and financials (XLF). Pressure on the used car market could be a harbinger for things to come in the broader market.