The setup here looks tempting over the immediate-term, but we think KSS is in for another tough year in 2013.

KSS may appear to be a cheap stock, but we think it’s built to stay that way. Our bias is to the upside this holiday given the abysmal performance it went up against last holiday, and the fact that it does not really begin to feel pressure from JC Penney coming back on line until 2013.

We need to keep in mind that KSS is quickly becoming a zero square footage growth retailer slowing from ~3%+ in 2010 and 2011 to +1.7% in 2012 and +1% next year. More aggressive repurchase activity can and likely will be used to grow earnings, but that doesn’t warrant ‘historical multiples’ from the days when KSS was aggressively growing its footprint productivity, and efficiency. As we pointed out in yesterday’s note on Macy’s, zero growth retailers have no problem trading at 6x forward earnings. KSS has never really gotten there, but it has also never been as mature as it is today.

Let’s keep in mind that it’s planning for a 3-4% comp in what it already thinks will be a highly promotional holiday. We already know that Macy’s is planning for a 4% comp, and while it has the benefit of JCP which will likely comp down at least 10-15 points below last year, there’s still potentially not going to be enough for everyone to go around.

That said, we’re less concerned with comp on what we’ll call ‘planned-promotion’ merchandise. In reality, it is a number we cannot forecast. No one can. Retailers themselves cannot do it other. It’s not as much a function as the actual number as the level of comp they are PLANNING. Then they execute on a marketing plan, and either a) convert at planned price, b) clear at heavier than expected discounts, or c) let comps lag, but keep margins high while letting inventories grow. (Note: Those are listed in order of attractiveness for the stock.)

Who are we to doubt that they can get the 3-4% comp given their more aggressive and better assorted inventory position compared to last year, but we do cast doubt on gross margins. While we see risk in 4Q EPS, however, our real concern is looking out to 2013.

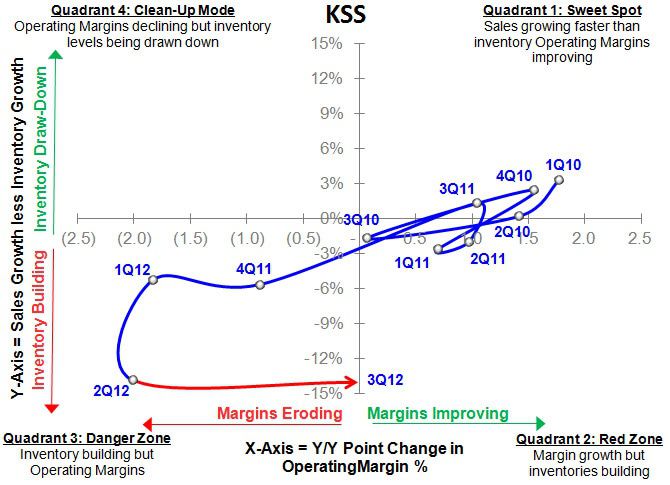

2013 is when we expect the mid-tier to become severely promotional, and the fact that KSS is off mall does not isolate it from JCP (on-mall) regaining share. Growth in e-commerce (+220bps) and new stores (+140bps) has helped offset KSS’ contracting core business this year (-150bps), but we see slowing new store contribution, further erosion in core (comps down -3.5%), and anniversarying a 53rd week leading to a 3%-4% sales deceleration next year. This is illustrated in the first chart below.

The best bull case is that consumer spending rebounds, and KSS’ off-mall presence proves to insulate itself from increased competition between JCP, M, and GPS. In addition, technology investments continue to drive 40%+ e-commerce growth and the new merchandise team gets the kids business back on track driving +3%-4% comp growth. With modest gross margin expansion and SG&A leverage you get $5.25 in 2013 earnings – suggesting 10x earnings and ~5.3x EBITDA. That’s cheap enough for us to get interested in KSS, presuming there was a fundamental catalyst we could identify to get it there.

A number between $4.00-$4.25 suggests that the stock is closer to 12x-13x earnings. This might not be expensive, but mature department stores – with better content – have traded at half that multiple in the past. The simple fact that KSS hasn’t comped while the rest of the mid-tier has benefitted from JCP hemorrhaging nearly $3Bn in share requires a high degree of trust to assume a meaningful rebound just when JCP’s top-line reaccelerates. We don’t see enough differentiation at KSS to bet against this risk/reward setup. While not at the top of our short list, it’s a name we think will work headed into 2013 (we like Macy’s and GPS better on the short side).