We remain bearish on Darden Restaurants. Yesterday, Keith added it to the short side of our Real-Time Positions.

The poor same-restaurant sales trends at Olive Garden and Red Lobster are pressing the company towards an impasse. The concepts account for roughly 75% of the company's consolidated revenues. We believe that the company is on an unsustainable path. Specifically, the company is burning cash and the stock can no longer be all things to all investors. A rich dividend, aggressive growth profile, and sturdy balance sheet have attracted investors of all different styles to buy Darden’s stock over the past few years. One, or more, of these attributes is likely to fall away as maintaining all three becomes unsustainable. A proactive reorganization, including a cessation or slowing of unit growth, would be preferable to the more likely reactive lowering of margins or slashing of the dividend that we think is becoming inevitable.

Prior to the onslaught of the Hurricane Sandy, casual dining same-restaurant trends were slowing. We believe that the impact of Sandy on Darden’s results have not yet been baked into consensus. October looks to be worse than September and November, almost certainly, has gotten off to a difficult start given the company’s exposure to the northeast.

Expectations, and company guidance, may be negatively revised in the coming weeks as we progress further through Darden’s second fiscal quarter of 2013.

- Management expects total sales growth in fiscal 2013 of between 9 % and 10%; consensus is 12%

HEDGEYE: We believe that the Street may be aggressive in modeling sales growth 200 bps in excess of management’s guidance

- Management expects combined same-restaurant sales growth for Red Lobster, Olive Garden, and LongHorn Steakhouse of approximately 1% to 2%; consensus is looking for 1.46%

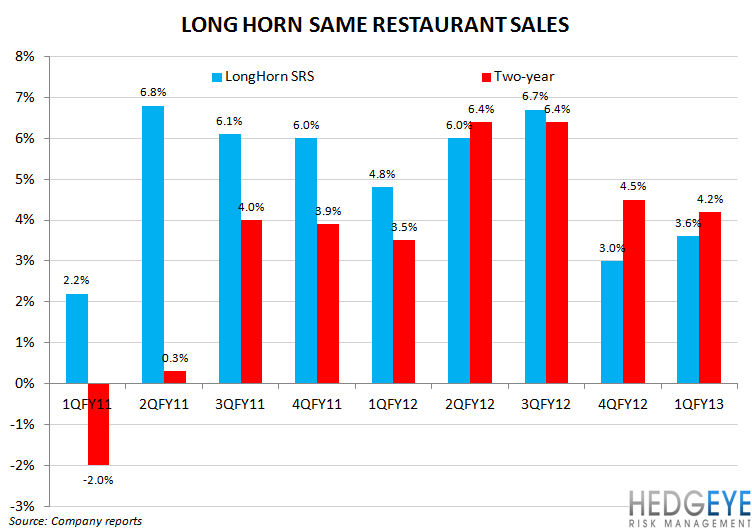

HEDGEYE: LongHorn Steakhouse lost momentum on a two-year basis in 1QFY13 and slowing industry trends, along with the impact of Sandy, could pressure the Darden system’s sales growth. Consensus is expecting continuing sales momentum at RL & OG in 2QFY13 with an acceleration coming in 2HFY13

- Management expects that diluted net earnings per share growth from continuing operations for 2013 will be 5% to 9%; consensus 8%.

HEDGEYE: Despite consensus expecting a resounding top-line beat in 2QFY13, earnings per share growth is expected to come in 100 bps below the high end of management’s guidance.

The Darden management team has done a commendable job outlining the plan towards a sales recovery as the company navigates FY13. We believe that the likelihood of the recovery playing out as planned is slim; we expect continuing softness in the broader category and continuing underperformance at Olive Garden and Red Lobster. We are expecting FY13 guidance to be revised lower when the company announces 2QFY13 results.

Howard Penney

Managing Director

Rory Green

Analyst