This note was originally published at 8am on October 23, 2012 for Hedgeye subscribers.

“This tends to leave us less prepared when the deluge hits.”

-Nate Silver

If you think about all of the corrections (2-8%), draw-downs (9-19%), and crashes (20-30%) stocks and commodities have had in the last 5 years, how many of your favorite economists nailed calling all of them?

Almost anyone who is overpaid on the sell-side can tell you a story about why something is going up – but why do they have such are hard time articulating real-time risk on the way down?

Forecasting growth (slowing in Q1/Q2 of 2012) and earnings (slowing Q3/Q4) in 2012 wasn’t easy. But it’s even more difficult to comprehend how people who missed calling both are now telling you this is the “trough” and stocks are “cheap.”

Back to the Global Macro Grind…

“Forecasting something as large and complex as the American economy is a very challenging task. The gap between how well these forecasts actually do and how well they are perceived to do is substantial. Some economic forecasters wouldn’t want you to know that.” (The Signal And The Noise, page 177)

How $50-100 Billion in market cap companies like Caterpillar (CAT) and Intel (INTC) miss these very obvious turns in both the global growth and the corporate earnings cycle at this point shocks me.

Does anyone get paid to have learned anything from the cycle turning in late 2007? The Fed can’t smooth the corporate EPS cycle.

In our top Global Macro Theme for Q4 (#EarningsSlowing – ask sales@Hedgeye.com for the slide deck if you haven’t reviewed it), we contextualize the following:

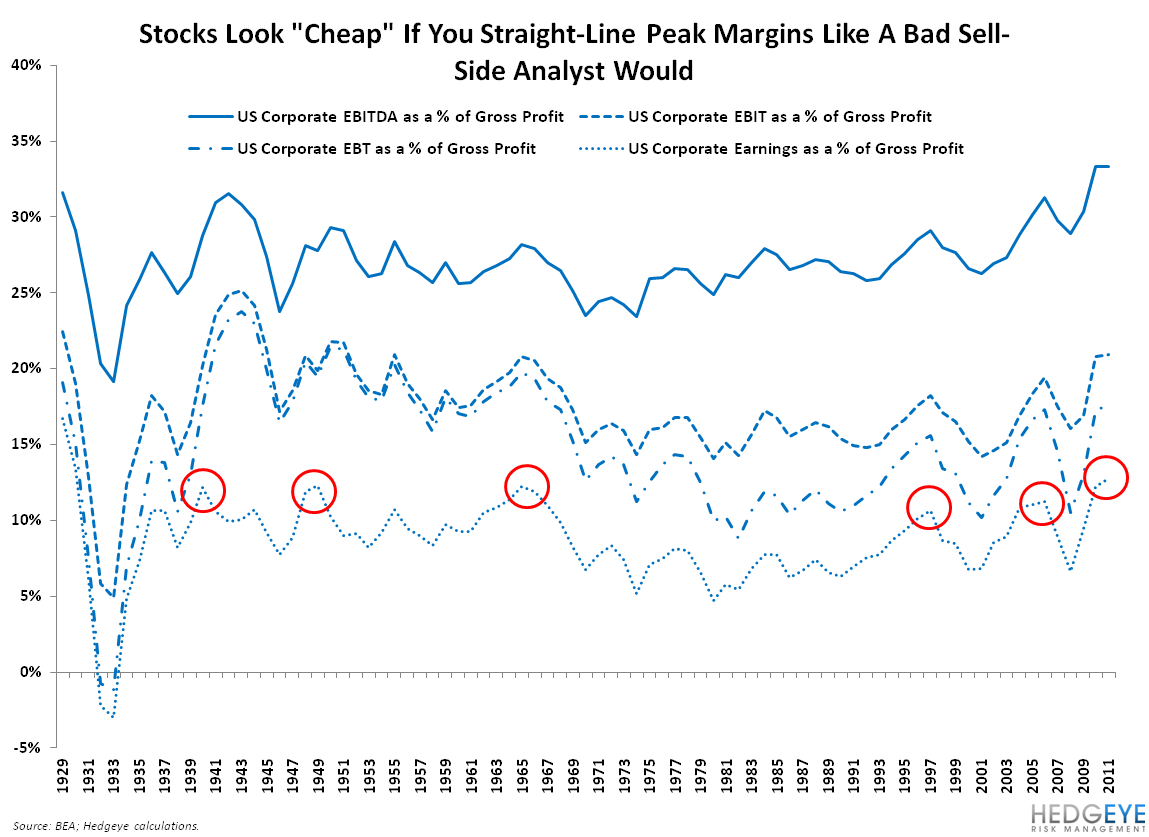

- What coming off the last 5 peaks in corporate margins in the last 100 years looks like (stocks look “cheap” at the peaks)

- Why the risk to expectations is more in Q4 and 2013 than what’s staring CFO’s in the face in Q312

- Why stocks aren’t cheap if you’re using the right growth, margin, and earnings assumptions

That’s just the long-cycle data. It’s not “tail risk.” Corporate margins peaking as sales growth slows is a very high probability situation that you are seeing come across the tape with each and every Q312 earnings report. This should not be surprising you.

What surprises me is how disconnected the reality of this moment in the cycle has been relative to where the stock market has levitated. If you want to talk legitimate TAIL risk, that spread risk is it.

I often get asked what would change my view. My answer is usually a question – on what, the economy or the stock market? These have been two very different things in 2012 and all of a sudden they are colliding.

“Apres moi, le deluge”

That’s what King Louis the XV said to his mistress, meaning, en francais – ‘after me, the flood.’ And oh did he nail that one! And that’s the point of hitting the end of a long-standing narrative – everything bullish about stocks, oil, and gold at 14 VIX tends to end, fast.

Are the perma-bulls still serious about what they were saying in March (right as #GrowthSlowing took hold)?

- US GDP Growth +3-4% (US GDP = down 69% from Q411’s 4.10% to 1.26% reported most recently)

- Earnings are “great” (they were at the Q1 2012 top; but Q312 has been the worst in 3 years)

- Stocks are “cheap” (sure, if you use the wrong numbers)

Given the data, I doubt it. That would be a joke. And clients aren’t laughing. From Denver to Kansas City, Boston, Maine, and San Francisco (this morning), I have been on the road speaking with clients for the last month. They are getting very concerned about Q4 of 2012 through Q2 of 2013 – and they should be. They’ve seen this movie before.

The real reason stocks and commodities were straight up since June was the Fed. Since the Bernanke Top (September 14, 2012), the SP500 has had a 3% correction. What would make it a 9-19% draw-down from that “buy everything high”? Re-read the last 600 words, then factor in an Obama win, and then add a US Debt Ceiling being bonked in January, right before we hit the #FiscalCliff.

And remember, after stocks were up “double-digits YTD” in October of 2007, le “deluge” had a heck of a time finding its trough.

My immediate-term risk ranges for Gold, Oil (Brent), US Dollar, EUR/USD, UST 10yr Yield, and the SP500 are now $1699-1741, $108.22-110.84, $79.06-80.16, $1.29-1.31, 1.71-1.82%, and 1419-1442, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer