Agricultural commodities price action continues to be mixed. Grain and protein prices are up significantly higher than a year ago while coffee prices continue to sink lower. The fundamental outlook suggests that the strength in beef prices should continue for some time. Higher beef prices are negative for TXRH, BLMN, WEN, JACK, CMG, and others.

Summary View

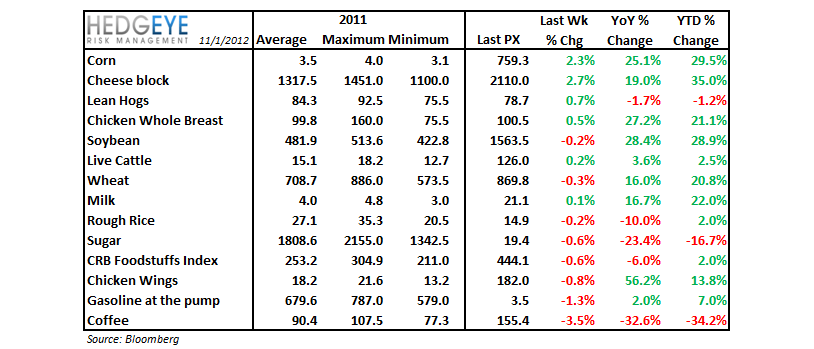

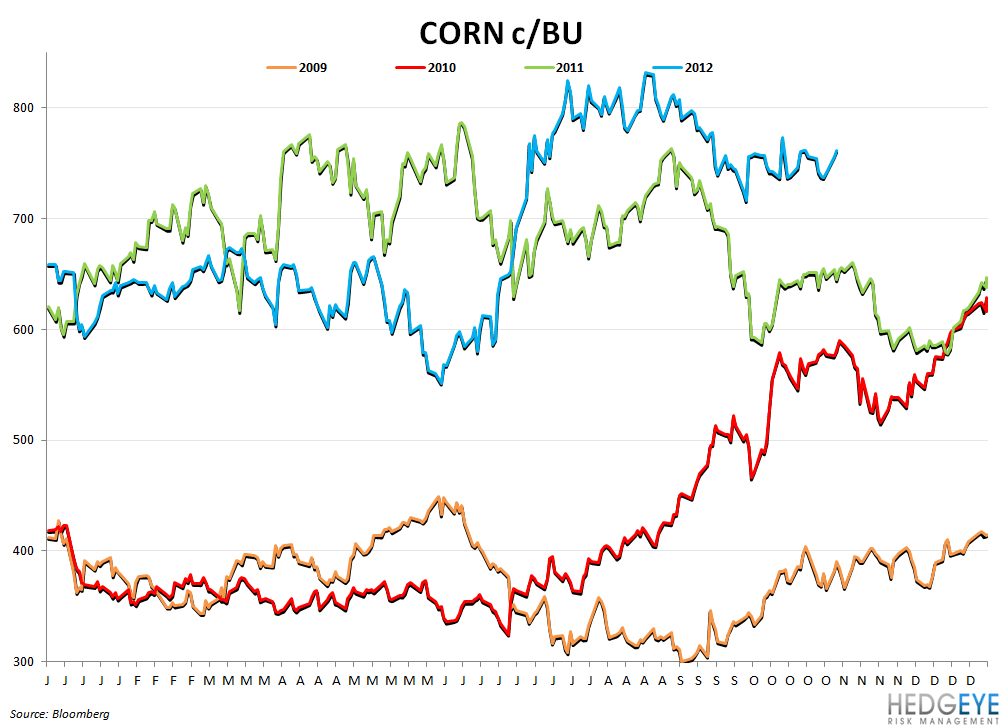

Corn prices have been moving higher over the past week as global supply concerns drive sentiment. Heavy rains in South America have delayed crop plantings. Theories that the world is going to need to turn to the US for supplies have not yet been confirmed by export sales prices. The amount of corn inspected for export at U.S. ports did increase by 49% in the week ended October 25th, however, according to the Department of Energy.

Beef prices moved modestly higher over the last week but trading has been mixed as bullish corn price action has been counteracted by uncertain near-term demand. The U.S. cattle industry is under pressure as record feed prices and elevated feeder cattle prices are not being offset by beef demand. The soft economic climate continues to limit retail and wholesale beef pricing power relative to the input price squeeze that feedlots continue to face. Elevated beef prices pose a headwind for TXRH, BLMN, WEN, JACK & CMG, among others in the restaurant industry.

Coffee prices declined -3.5% over the last week. Coffee has been trading in a range between 150 cents/lbs and 190 cents/lbs since May and is currently 33% below year-ago levels. On a global basis, indications are that supplies are ample. Concern about global economic growth slowing is adding further pressure to coffee prices. The continuing weakness in coffee prices is a positive for SBUX, PEET, DNKN, THI, CBOU, GMCR and other coffee retailers.

Gasoline Prices

Gasoline prices declined -1.3% over the last week but, as usual, regional trends are worth bearing in mind. The gasoline shortage in the North East, caused by Hurricane Sandy, is likely to have an impact on restaurant traffic trends in the region for several weeks. A similar impact was felt post-Katrina, in the gulf region, when tight gasoline supplies led to a decrease in miles driven which, in turn, led to a deceleration in restaurant traffic.

Correlation

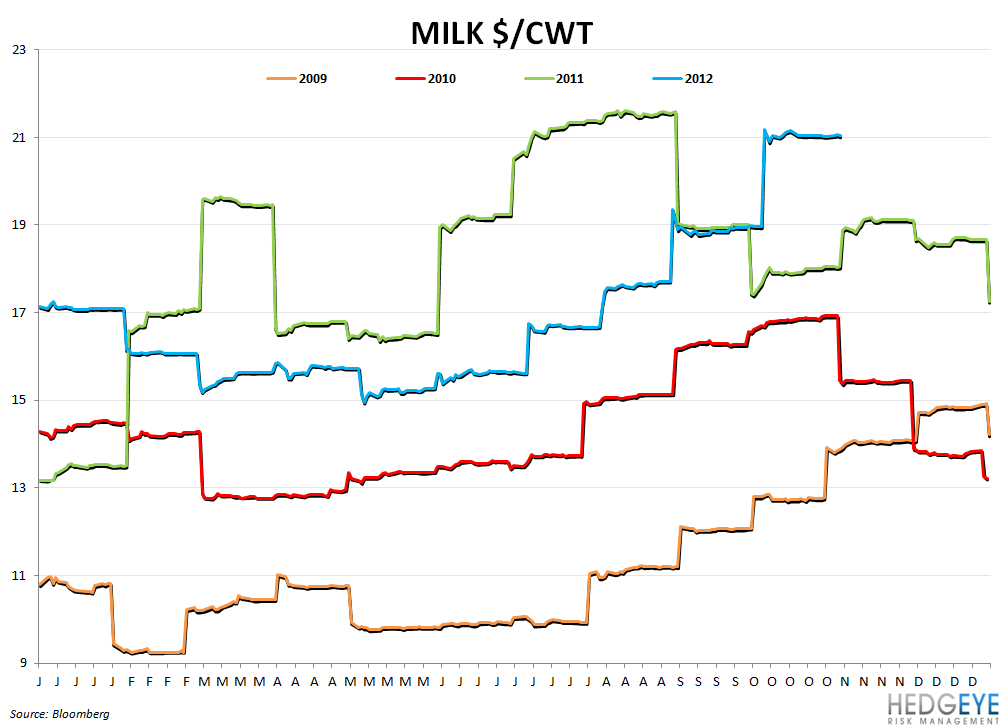

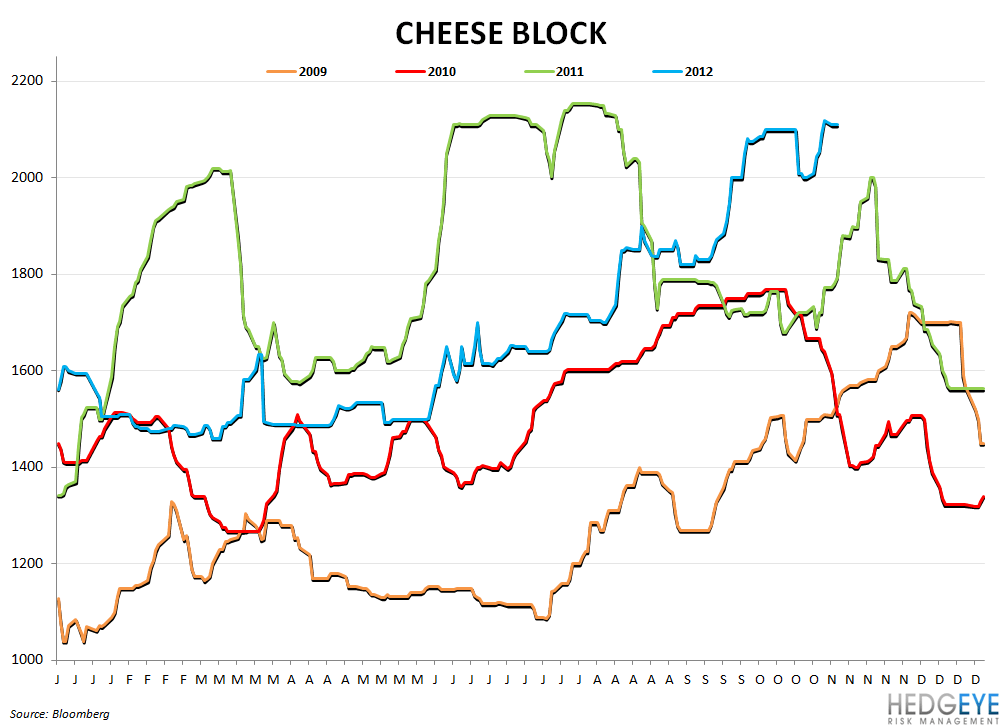

Charts

Howard Penney

Managing Director

Rory Green

Analyst