This note was originally published at 8am on October 15, 2012 for Hedgeye subscribers.

“We think we want information, when we really want knowledge.”

-Nate Silver

Within the context of the always-on tweeter-net, I thought that was a really thoughtful quote from the introduction to Nate Silver’s new book, The Signal and The Noise. I’ll be reviewing his framework for forecasting in the coming weeks.

Silver says the “signal is the truth” and “the noise is what distracts us from the truth” (page 17). Without having read the bulk of the book yet, I can already assure you that doesn’t hold when attempting to proactively predict Risk Ranges in real-time markets.

Our most immediate-term risk management duration (TRADE) is, by definition, noisy. Whereas our intermediate and long-term (TREND and TAIL) work can often be mistaken as truth when the noise isn’t confusing our confirmation biases.

Back to the Global Macro Grind…

Whether we like hearing it or not, we all have confirmation biases. That’s because we are human. At a bare minimum, I think Nate Silver and I agree on that. Thinking, Fast and Slow’s Daniel Kahneman would too.

Our risk management day involves grinding quantitative economic realities (data) with behavioral finance (timing). In order to make a probability-weighted forecast (taking a long or short position) we always look back, across durations, before looking ahead.

For us, the signal (and the noise) is real-time market prices – here’s what they did last week, across asset classes:

- US Dollar Index =up +0.4%, closing up for the 3rd week in the last 4 at $79.65 (bullish on both TRADE and TAIL durations)

- EUR/USD = down -0.7%, looking like the upside down of the USD Index (bearish on both TRADE and TAIL durations)

- CRB Commodities Index = down -0.3% (down -4.7% from the Bernanke Top, printing to Infinity & Beyond)

- Oil (blended Brent and WTIC) = up +2% (WTIC down -4.3% from the Bernanke Top)

- Gold = down -1.4%, as it continues to make a series of lower long-term highs (vs the 2011 Bernanke Bubble top)

- Copper = down -2.2% (bearish on both TRADE and TAIL durations)

- SP500 = down -2.2% (bearish TRADE resistance = 1448; bullish TREND support = 1419)

- Nasdaq = down -2.9% (bearish TRADE resistance = 3129; bullish TREND support = 3022)

- US Equity Volatility (VIX) = up +12.6% (bullish on both TRADE and TAIL durations)

- US 10yr Treasury Bond Yield = down -5% to 1.66% (bearish on both TRADE and TAIL durations)

In other words, there were plenty of signals and noises, across durations, in last week’s closing prices. There is also a confirmation bias in attempting to describe what happened because I, unlike Keynesian policy makers, believe that central planners are the primary causal factor in driving currency values and market correlations.

In the private sector, it’s ok to have a confirmation bias – you just have to be right more than you are wrong. If you’re wrong more than you are right, it’s ok - just go work for the government.

What do you do when you are wrong? For us, it’s pretty simple – we hold ourselves accountable to the mistake, try to learn from it, and grow. What other people do when they face adversity is up to them.

With the SP500 not having an up day in the last 6, what is the truth? Do growth and #EarningsSlowing matter? Or did it from the price where a lot of people thought Bernanke’s money printing meant the “fundamentals don’t matter”?

What are the fundamentals?

- US GDP Growth of 1.26% in Q2 2012, or consensus expectations of +3-4% growth 6 months ago?

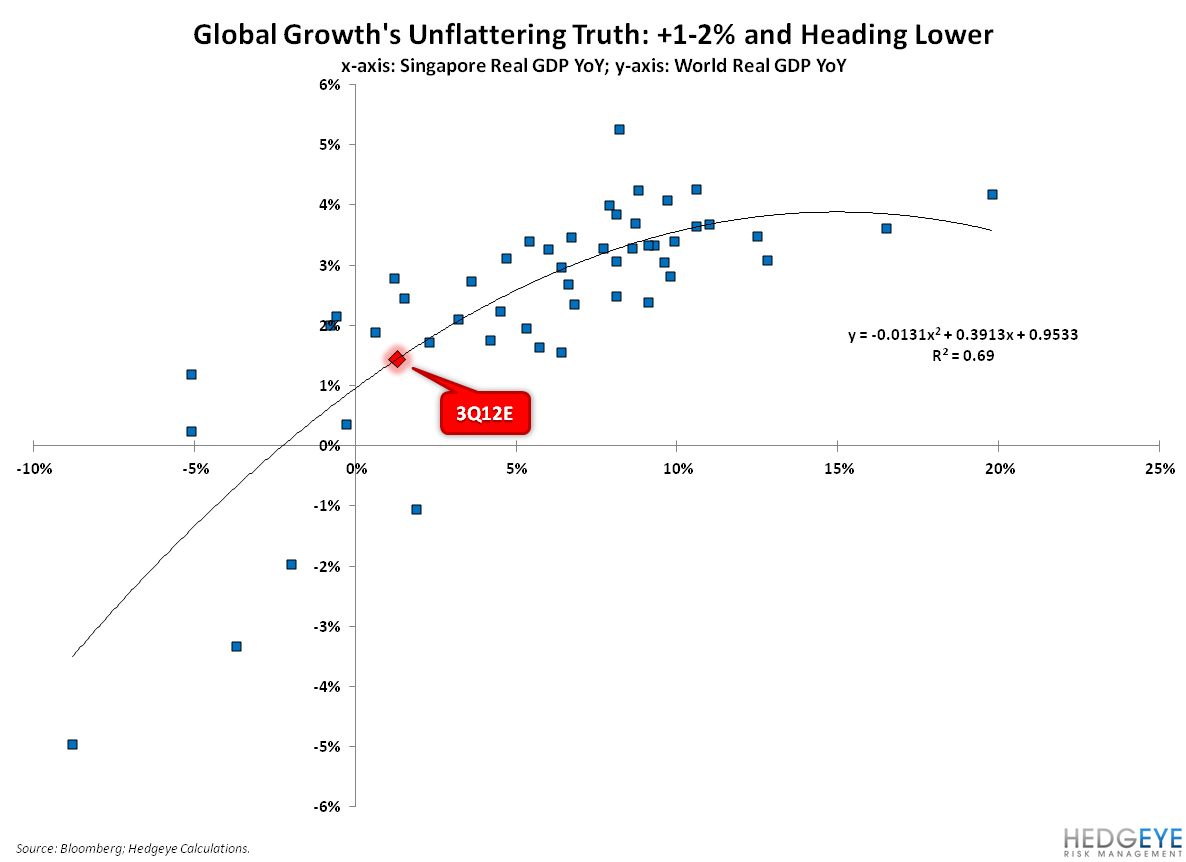

- Global GDP Growth of 1.3% (Singapore just reported that for Q3 2012) or +3% as far as the excel model can see?

- The worst preannouncement ratio (4:1) of #EarningsSlowing misses since Q3 of 2001, or stocks are “cheap”?

- US Technology Sector (XLK) down -3.5% in the last month, or what it’s “up YTD”?

- US Financials Sector (XLF) down -1.6% last week on JPM/WFC earnings, or what they are “up YTD”?

- Chinese inflation down sequentially to +1.9% (SEP) or India wholesale inflation up sequentially to +7.8% (SEP)?

Some might say all of this doesn’t matter, and all you need to do is know where a 1-factor/1-duration simple moving average model tells you where the market is and everything is either fine. Some might say that all of it matters and is measurable. That’s closer to the Noisy Truth.

Our signals say all this noise adds up to us having 12 LONGS and 9 SHORTS for this morning’s US stock market open. Provided that the SP500 doesn’t close > 1448, we’ll likely sell on green bounces, and buy on red corrections closer to 1419.

Our immediate-term risk ranges for Gold, Oil (Brent), US Dollar, EUR/USD, UST 10yr Yield, and the SP500 are now $1748-1774, $112.68-115.08, $79.34-80.05, $1.28-1.30, 1.61-1.71%, and 1419-1445, respectively.

Best of luck out there this week,

KM

Keith R. McCullough

Chief Executive Officer