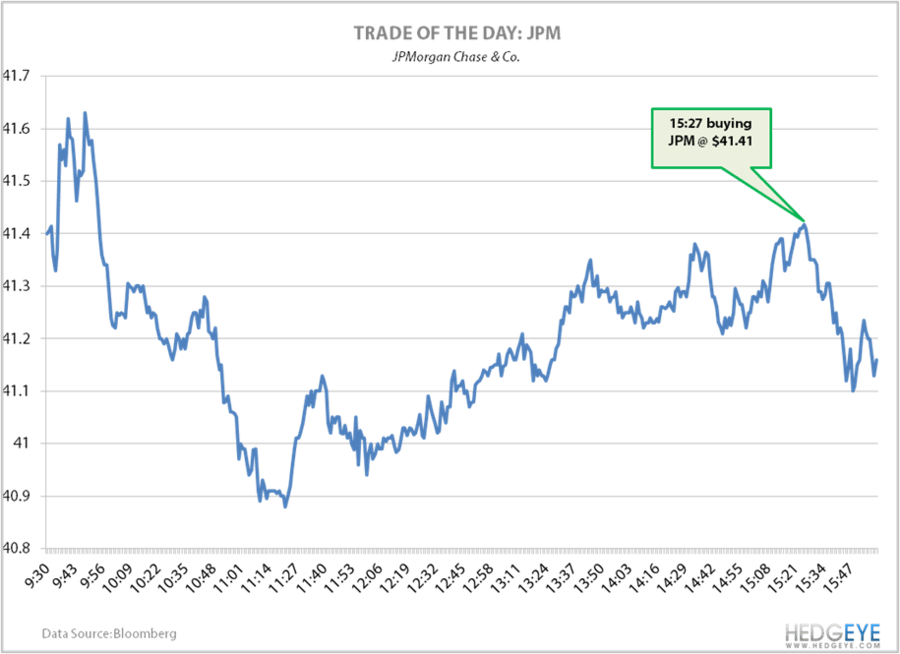

Today we bought JP Morgan (JPM) at $41.41 a share at 3:27 PM EDT in our Real Time Alerts. The company put up a solid quarter and Hedgeye Financials Sector Head Josh Steiner wants to be net long financials if Romney momentum continues to build. A Romney win would be a positive for banks and other financial institutions as he plans on toning down regulation.