There is plenty to like but too much uncertainty to get behind this name ahead of the quarter. Our research process is telling us to not be long SBUX for the second successive quarter.

Starbucks reported worse-than-expected 3QFY12 earnings and we believe there is significant risk of an additional miss in 4QFY12. We expect comparable sales to grow in line with consensus but believe that the likelihood of a substantial upside surprise is remote. The macroeconomic environment represented a headwind for Starbucks in 4QFY12 but company-specific factors are also hampering profit growth.

Our Stance Ahead of the Quarter

We would remain on the sidelines through the 4QFY12 earnings release. Consensus is assuming a sequential slowdown in comps for the Americas division but we believe global macroeconomic concerns will weigh on FY4Q results and the outlook for FY13. We expect a shortfall versus sales and EPS estimates for Starbucks’ FY4Q results.

Outlook

To become more constructive on Starbucks shares, as we were from March 2009 through May 2012, we would need to see management focused on a less complex web of operations. With the core business, CPG, and the Verismo home brewer, Starbucks has more than enough growth to satisfy investors. Increasing the number of “four-wall” concepts under the company’s umbrella is, in our view, not a promising development.

Starbucks has usurped McDonald’s as the most-loved restaurant stock among sell-side analysts. This is not a badge of honor from the perspective of the stock price. Below are some of the key guidance metrics for the upcoming quarter and the full fiscal year 2013:

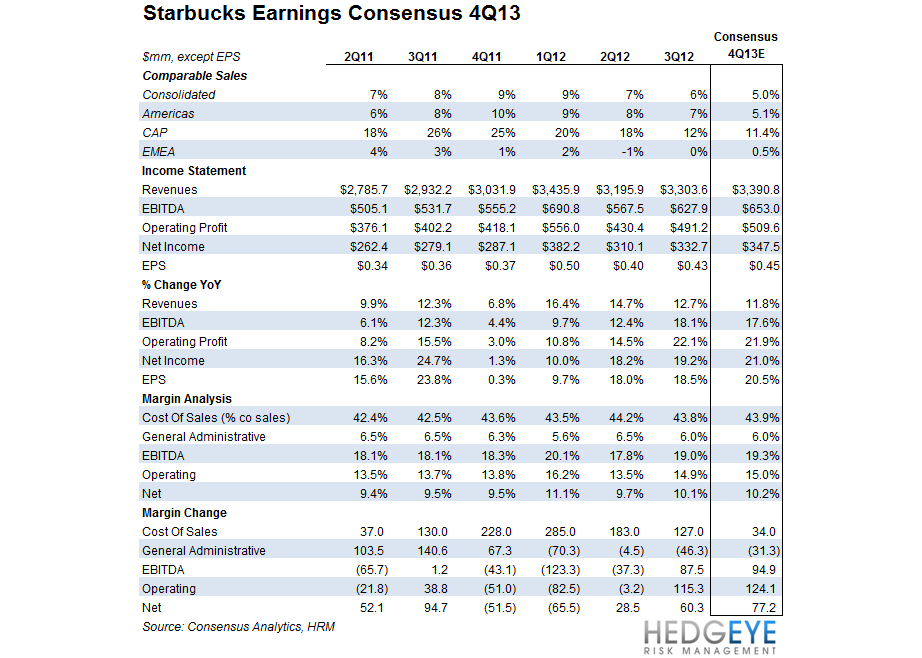

- 4QFY12 revenue growth of 10-12% versus the street is at 11.8%

- 4QFY12 EPS of $0.44-0.45, growth of 19-22% versus consensus of $0.45

- FY13 targeted revenue growth of 10-13% versus the street at 11.7%

- 1,200 net new stores – acceleration in U.S., China, possible acceleration of closures in Europe (the company has said that 25% of the store base in Europe is unprofitable)

- FY13 EPS of $2.04-$2.14 versus consensus of $2.13, according to Consensus Metrix

- FY13 is locked for coffee costs through 11 months at favorable prices. ~100m tailwind to operating income

Conclusion

The coffee tailwind is a well-documented tailwind for Starbucks. What is less well-known is the extent to which comps have slowed and what return on investment the company has been receiving on its growth initiatives. We believe that there is significant risk the company sets out to manage (bring down) expectations among investors ahead of FY2013 results.

Over the long-term, we believe that Starbucks is one of the best-positioned consumer-facing companies given the growth prospects that management has outlined. Over the near-term, we believe that expectations are overly optimistic and we would look elsewhere for exposure to restaurants on the long side.

Howard Penney

Managing Director

Rory Green

Analyst