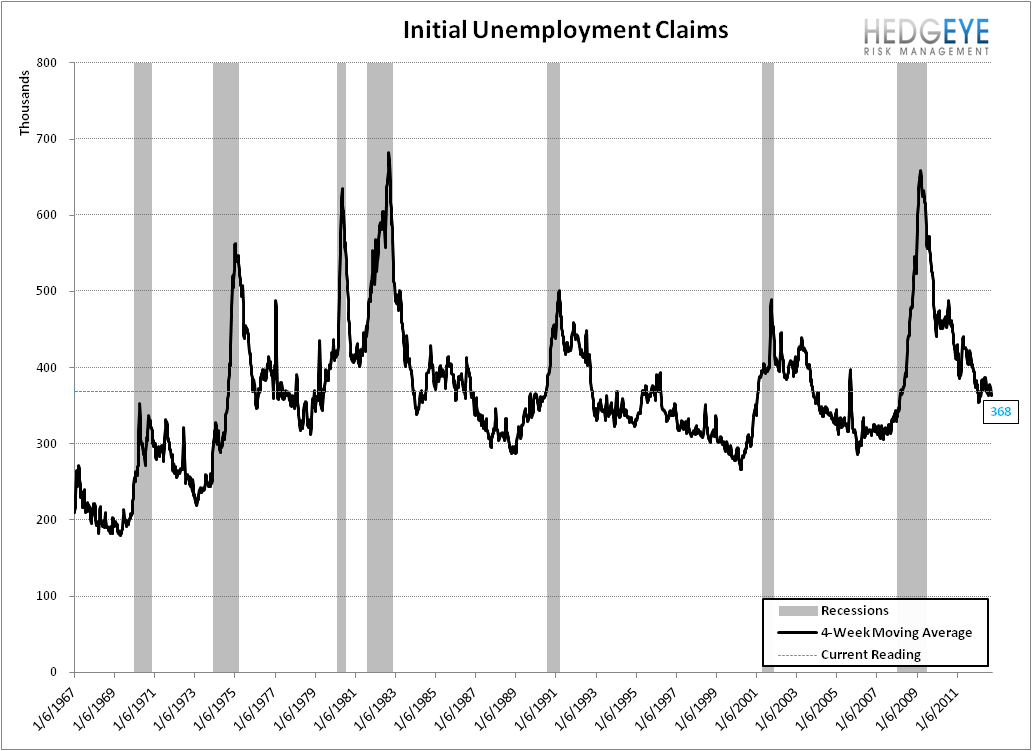

Blame California

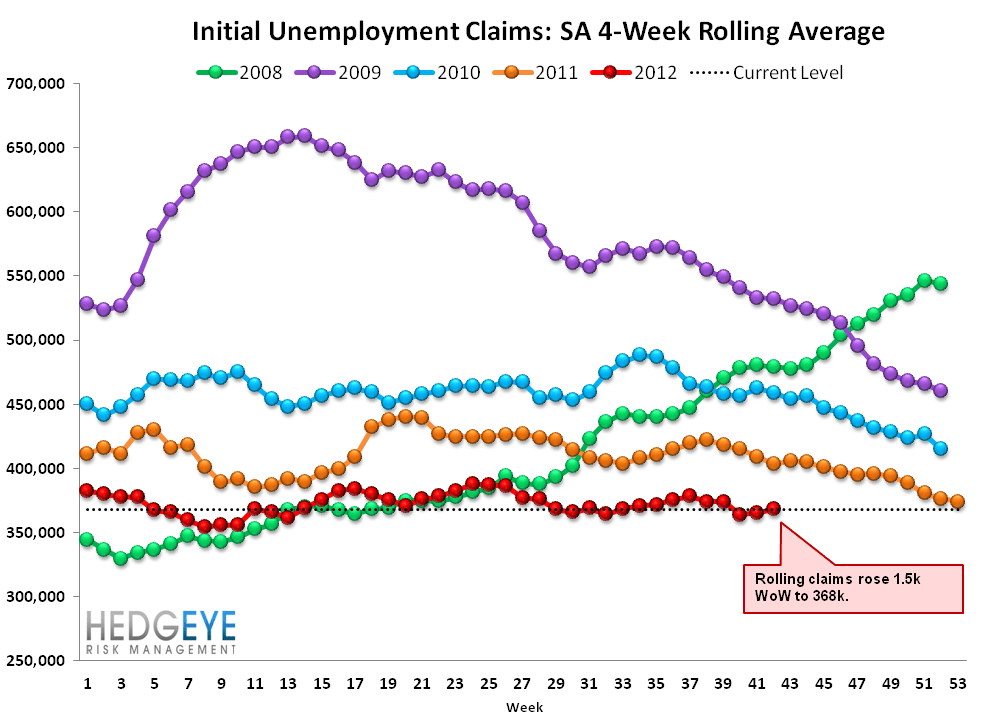

Three weeks ago, California was omitted causing initial jobless claims to drop 28k. Two weeks ago, California was double-counted causing claims to rise 46k. Last week, California was back to normal so claims dropped 23k. Net net, in the last three weeks, the 4-week rolling average for seasonally-adjusted jobless claims has gone from 364k three weeks ago to 368k in the most recent week.

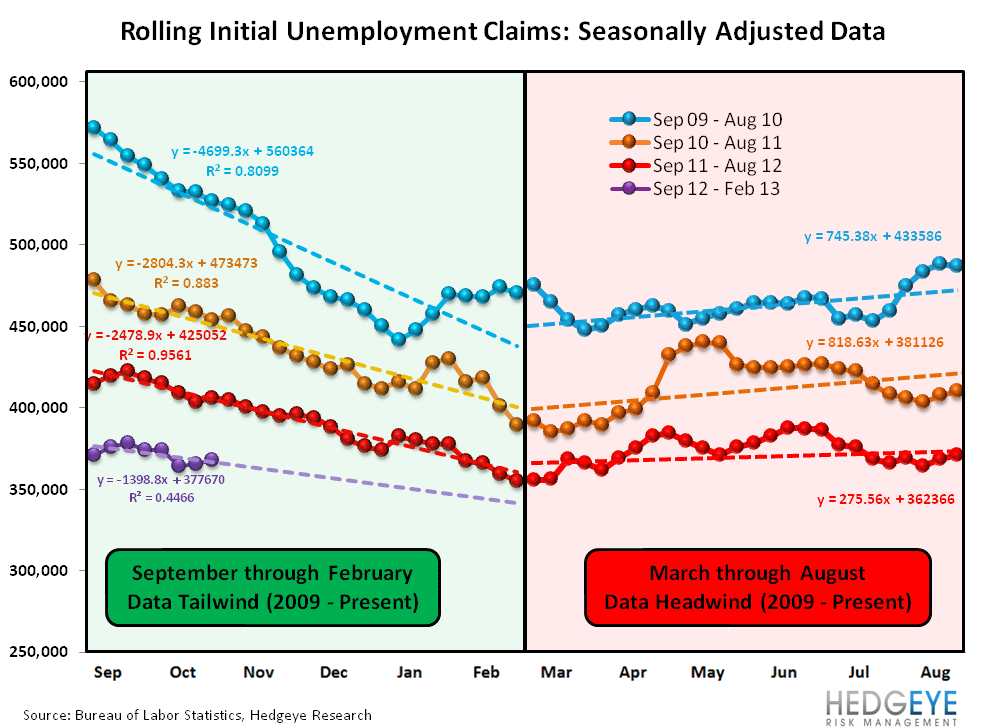

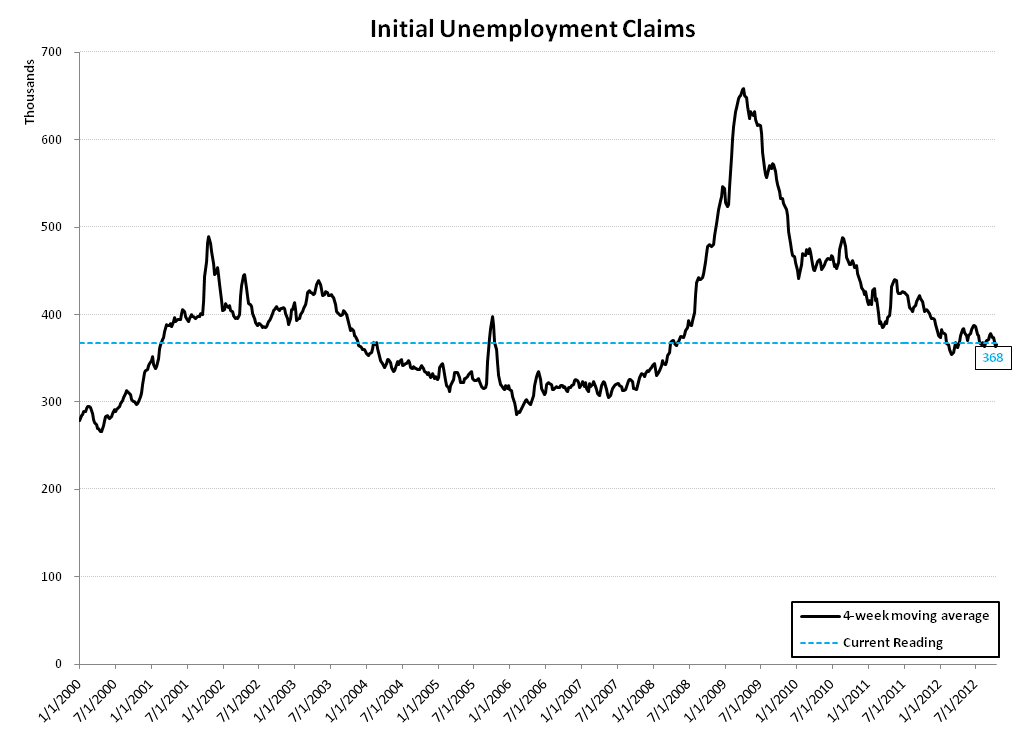

As we show in the first chart, the trend in claims since the start of September is lower. This is consistent with our expectation, and we would expect to continue to see claims move steadily lower through February 2013, owing to the faulty seasonal adjustment factors that have been warping the data for the last 3.5 years. The same distortion occurs in non-farm payrolls, incidentally. This perception of a steadily improving labor market should be a tailwind for credit-sensitive financials.

What's Really Going On?

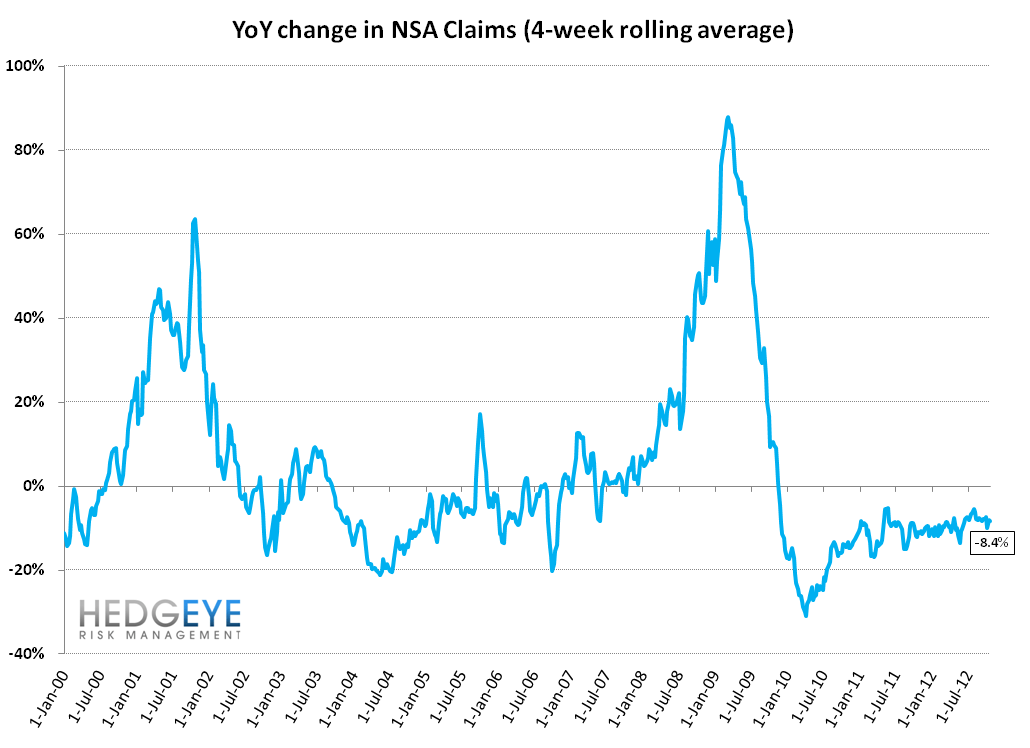

Looking past the distorted SA numbers, the reality is that the labor market is still improving in spite of the recent spate of headlines about sizeable layoffs in the private sector. We measure this by evaluating the YoY change in rolling non-seasonally-adjusted initial jobless claims. This morning's print brought that series to -8.4%, slightly worse than the prior week's print of -10%. A larger decline in YoY claims is, of course, better. We don't put too much emphasis on one or two or even three weeks of data, but if we see the 8.4% YoY change from this morning continue to converge toward zero at a rapid rate over the next 3-4 weeks, that will be indicative of a real problem starting to take hold in the labor market. Interestingly, the rest of the market will be unlikely to notice this since the SA tailwinds will appear to make the data go sideways.

The Data

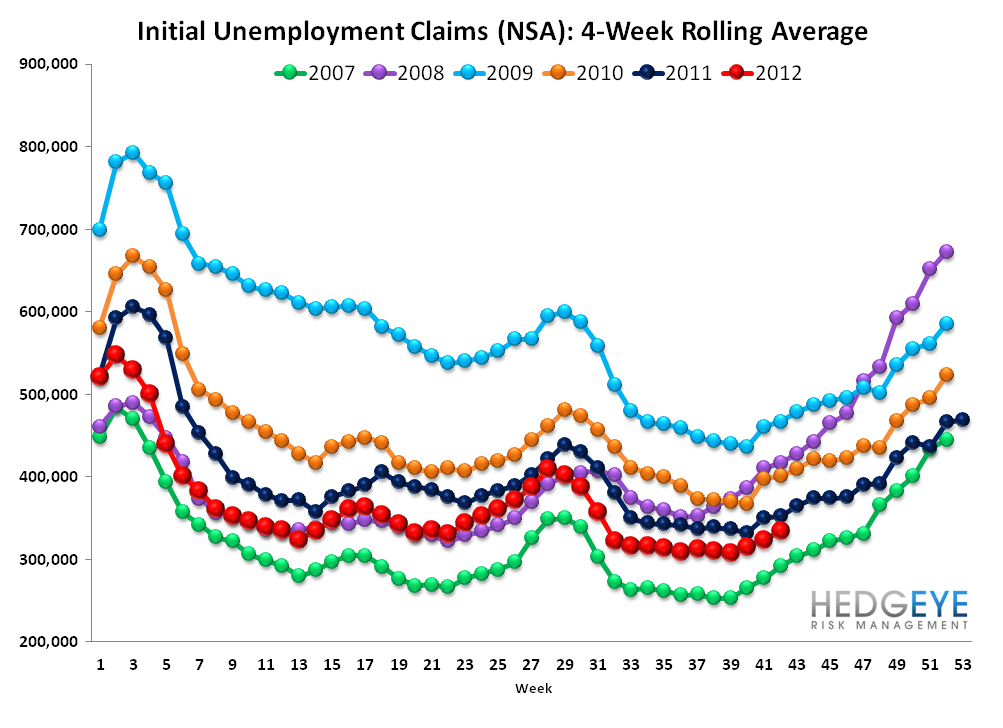

Last week initial claims fell 19k to 369k. After incorporating a 4k upward revision to the prior week's data, claims fell 23k. Rolling claims rose 1.5k WoW to 368k. The non-seasonally adjusted series fell 20k to 343k. The NSA YoY change was -8.4%.

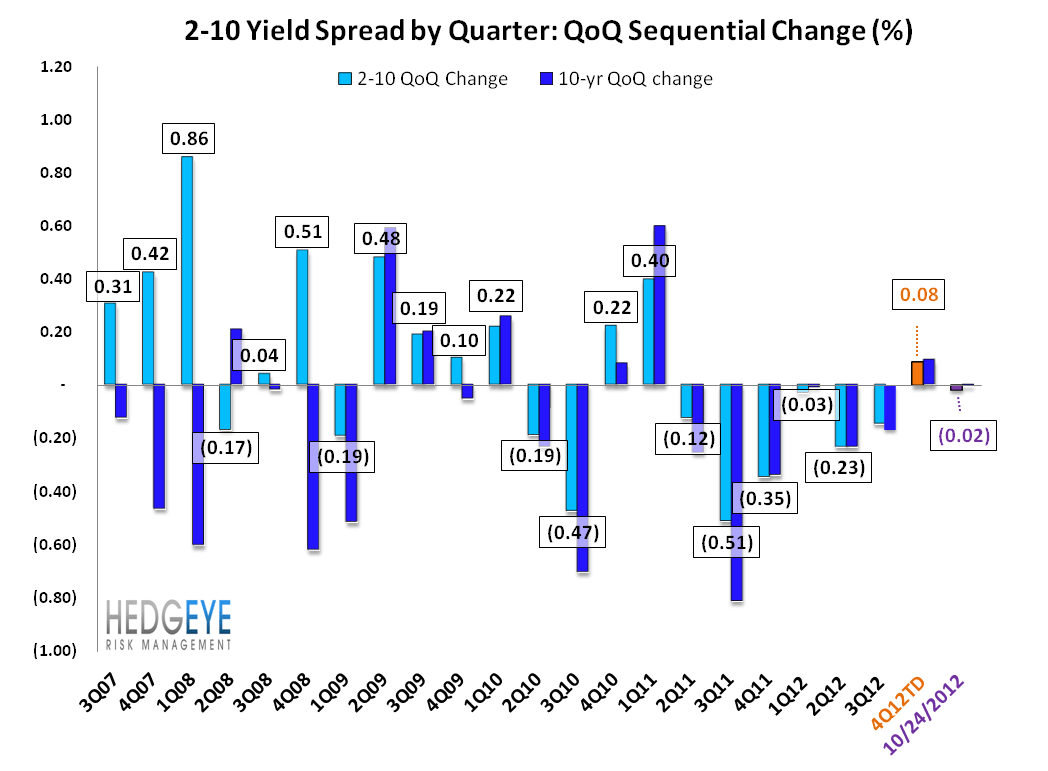

Yield Spreads

The 2-10 spread fell 4 bps WoW to 150 bps. So far 4QTD, the 2-10 spread is averaging 1.45%, which is up 8 bps relative to 3Q12.

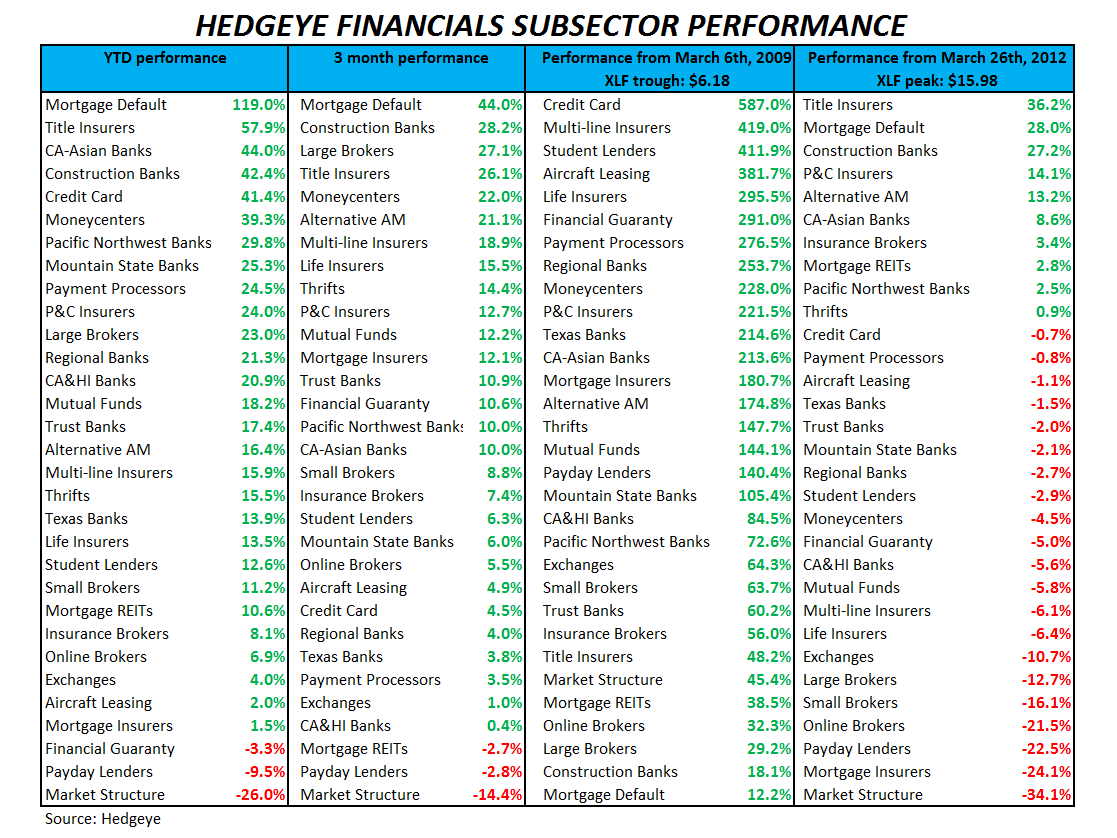

Financial Subsector Performance

The table below shows the stock performance of each Financial subsector over multiple durations.

Joshua Steiner, CFA

Robert Belsky