CRI beat and we’ll give them that. We went into the quarter and outlined in our CRI Black Book on 10/15 that we didn’t expect a miss due to an inflection in margins (i.e. product costs turn favorable), but that we expect the reality of our thesis – lack of product differentiation resulting in pricing/margin pressure – to play out more visibly in Q4 and into 1H F13. There is no change to our call. If the stock is up today on Q3 numbers, now is the time to short it. (please contact if you are interested in seeing the full details of our call and CRI Black Book)

- Wholesale numbers came in significantly lighter than expected offset in part by International results with stronger profitability driven by higher gross margins accounting for stronger EPS.

- Notably, CRI’s Q4 outlook calls for sales over 200bps higher than consensus, but EPS a penny lighter. This suggests significant margin weakness relative to expectations. If this is indeed related to sell-in at Carter’s wholesale (i.e. JCP) it suggests sales are coming at substantially lower margin. It also begs the question of what happens following sell-in when accounts start pressing CRI on margin at the same time.

- In addition to Q3 wholesale sales turning negative for the first time in 9 quarters, retail comps remain a concern. Both Carter’s and OshKosh decelerated meaningfully on a 2yr basis despite a more favorable setup and comps get much tougher over the next 2 quarters. Growth at retail continues to be driven almost entirely by lower productivity new store growth and e-commerce. Given the lack of product differentiation across channel, we expect this impact on owned-retail to continue.

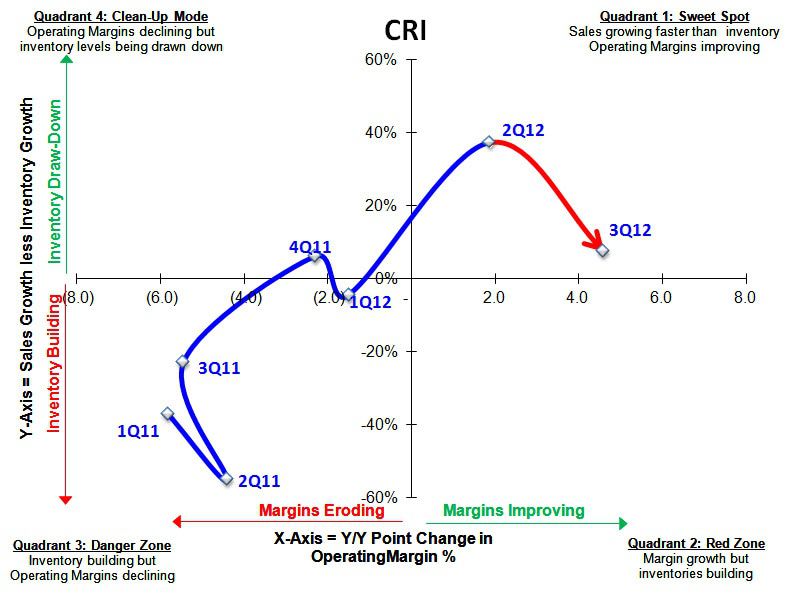

- Inventories were good though the sales/inventory spread turned down sharply in quadrant 1 reflecting the full integration of Bonnie Togs. Excluding BT, inventories were up +11% last quarter so the -3% inventory growth this quarter is sequentially positive.

- Given the mixed Q4 guidance, our primary focus on the call will be 1) how much of the incremental lift in Q4 sales is lower margin wholesale business, and 2) where are AUR trends shaking out now that the company has gone dark on disclosure just at its outlook would suggest that pricing is under fire.