Is the slowdown seen in the quarter just a pause or is it indicative of lodging entering the next phase of the cycle?

“Looking ahead, our results will be driven by two things: first, the trajectory of the global recovery and whether it regains its momentum in 2013; and second, our ability to use our high-end, global brands, to get more than our fair share of the long-term growth in global travel.”

- Frits van Paasschen, CEO

CONF CALL NOTES

- It's not clear if the deceleration is a temporary pause due to the upcoming election in the US, Chinese government changeover and Euro headwind or something more permanent

-

During the quarter, the Euro situation grew more tenuous with REVPAR up 3% held somewhat by the Olympics and in Asia.

- Underlying growth in NA was more like 7% if you adjust for a mid-week 4th of July and shift in the Jewish Holidays

- Africa & ME benefited from easy comps and strength in Dubai

- Would have generated $2MM of EBITDA from the 2 hotels sold in the quarter

- Some group bookings are on hold as customers take a wait and see approach to next year

- Looks like construction starts may accelerate, giving their business a boost

- Yet to see an existing hotel project stop from lack of financing

- Bulk of their development is in Tier 2 & 3 cities

- There has been a drop in Chinese government business which they believe is linked to the government changeover coming in November

- Despite decelerating growth, Chinese outbound travel is up and so is leisure travel

- They believe that US and China are more likely to resume growth than not

- They are working to de-risk HOT's business by reducing expenses. Their corporate headcount is 10% lower today than 4 years ago. They are also reducing their exposure to owned and increasing their fee based revenues which are more stable

- Completed the sale of the Sheraton Manhattan in the Q, with all 3 sales netting over $500MM in proceeds

- Their fees should make up 65% of their earnings going forward

- SPG consistently delivers over 50% of their occupancy.

- The slowdown in trends was most significant in Asia and mostly China this Q

- Estimate that the calendar impacted the quarter by about 150bps. Trend in the US is fine and stable as we enter 4Q, but given the elections and fiscal cliff approaching, its unlikely that things improve in 4Q.

- If demand trends pick up, then they should see a lot of rate growth

- Large groups are still a source of weakness

- Expect US to be at the upper end of the 4-6% guidance range

- They benefited from Olympics this Q. Europe RevPAR growth will be at the low end of their guidance range.

- Slow down in China was much sharper than the 8% they expected. Slowdown in China was across the board. Convinced that they will recover early next year with the government changeover.

- Expect Asia to be at the mid-to-low end of their guidance range

- Saudi and Gulf states continue to do well with the balance of the ME suffering from the events in the papers. Expect growth in the mid-point of the range.

- Argentina RevPAR declined 16% in 3Q and negatively impacted Latin American RevPAR by 450bps in the Q. The situation in Argentina is unlikely to get better any time soon. Mexico is showing strong signs of recovery with RevPAR up double-digits. Brazil, Chile and Peru have been impacted by the China slowdown but still growing.

- Their owned hotels underperformed their expectations. Currently have 53 owned and leased hotels. As a result of renovations and other issues, only 46 hotels were in the same store set. With 30% of this EBITDA coming from four cities Phoenix, Maui, New York and San Francisco, 20% of EBITDA from Europe with more than half coming from Italy and Spain and in London you get 90% of own EBITDA in Europe. Latin America accounts for another 20% of 2012 own EBITDA with 90% of this coming from three countries Mexico, Brazil and Argentina. Finally, Canada and Australia contributed 25% of worldwide owned EBITDA.

- Don't expect much improvement in their owned hotel performance through the balance of their year, but their cost control should be good. Hard to grow margins with their current RevPAR levels.

- Their base mgmt fees were impacted by FX

- Fee and other income line will be impacted by a difficult YoY comparison in 4Q but core growth will be similar to 3Q

- Expect to deliver another $10MM of EBITDA from Bal Harbour and expect to close over 70% of units by year end.

- Assets sales completed to date reduced 3Q EBITDA by $2.5MM and $8MM in 4Q

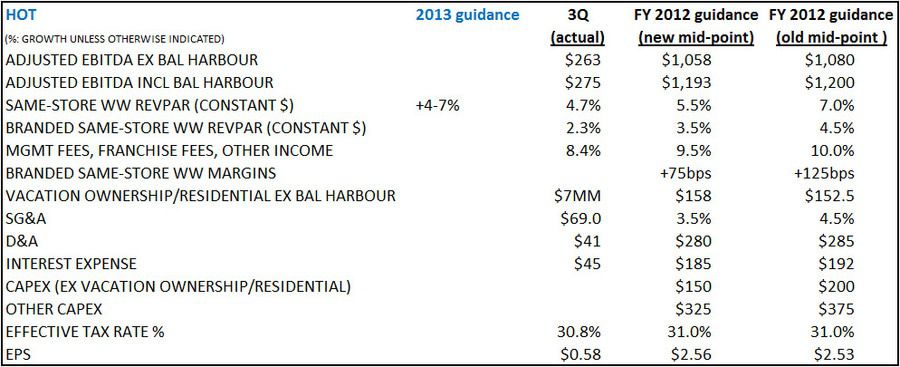

- Expect that the 2013 RevPAR range will be from 4-7% but current trends suggest something in the lower end of that range. An acceleration in the US and China would get them to the upper end of the range.

- Intend to maintain a leverage ratio of 2-2.5x so that they can maintain an investment grade rating

- They are going enhance segment reporting in their next filing to give more geographic disclosure

Q&A

- Net cash proceeds from the Sheraton Times Square? Little over $500MM for all 3 sales so Manhattan is in the high $200MM's.

- Development interest has increased so they don't see any slowdown in 2013 openings

- Argentina impacted international RevPAR by 450bps and Canada was the other big impact on NA

- Outside the US, there was no issue with hotel financing for M&A. In the US, there has been more financing for M&A than usual.

- OEH would benefit from reducing their overhead and reservations system. They have been in talks with them for 3 years.

- This is a stage in the cycle of where asset sales make sense

- Doesn't look like they made any incremental share purchases post their 2Q12 conference call. Won't comment on whether they were restricted. Given the volatility of their stock they are opportunitistic and like to buy when they are trading below intrinsic value

- They are planning on running VOI for cash but have no plans to spin it out and have ways of growing that business in an asset-light fashion

- Corporate negotiations are on hold until post elections but they are shooting for high single-digit increases since their occupancies are peak levels

- Think that in a few years they can get to 100 Alofts through conversions

- Group is pacing in the mid single digits for 2013. Early indicators are good. Outside NA group business is less important

- Capital needs over the next few years. This year, they will end up spending less money on capex than they initially planned as some projects got delayed and pushed into next year. Next year, they expect to spend a little more. Timeshare spend will not be a big number.

HIGHLIGHTS FROM THE RELEASE

- 2013: "Expects Bal Harbour to contribute approximately $30 million to $40 million in EBITDA, which is approximately $100 million lower than 2012. Asset sales completed to date will reduce 2013 EBITDA by approximately $20 million year over year and approximately $30 million on an annualized basis."

- “We delivered another solid quarter of EBITDA and EPS growth led by continued gains in both room rates and occupancy. Global RevPAR grew nearly 5% in constant currency, despite a deceleration in the global economy. In fact, occupancy rose in all regions and is now reaching or exceeding peak levels in many markets around the world.”

- EPS from continuing operations was $0.58

- Adjusted EBITDA was $275 million, which included $12 million of EBITDA from the St. Regis Bal

Harbour residential project. - WW SS Systemwide RevPAR (constant currency): 4.7% and 1.3% in actual dollars

- NA Systemwide RevPAR (constant currency): 5.3% and 4.8% in actual dollars

- "Originated contract sales of vacation ownership intervals and numbers of contracts signed decreased 1.2% and 3.8%, respectively, primarily due to lower tour flow partially offset by a slight increase in the average price of vacation ownership units sold. The average price per vacation ownership unit sold increased 1.8% to approximately $14,300, driven by inventory mix."

- In 3Q12, HOT "closed sales of 14 units at Bal Harbour and realized incremental cash proceeds of $59 million associated with these units. From project inception through September 30, 2012, the Company has closed contracts on approximately 64% f the total residential units available at Bal Harbour."

- In 3Q12, HOT signed 25 hotel management and franchise contracts (~4,800 rooms), and opened 20 (~ 6,500 rooms).

- Of the new contracts signed 18 are new builds and seven are conversions from other brands.

- Four properties (~800 rooms) were removed from the system during the quarter.

- "At September 30, 2012, the Company had approximately 370 hotels in the active pipeline

representing approximately 95,000 rooms" - "Starwood’s Board of Directors has declared the Company’s annual cash dividend of $1.25 per

share, an increase of 150% from the prior year." - "On October 24, 2012, the Company completed a securitization involving the issuance of $165.7

million of fixed rate notes. Starwood is contributing approximately $174.4 million in timeshare

mortgages resulting in an advance rate of 95% with an effective note yield of 2.02%. The proceeds from the transaction will be used for general corporate purposes and the pay down of the securitized vacation ownership debt related to its 2005 securitization." - "Special items in the third quarter of 2012, which totaled a benefit of $33 million (after-tax), primarily related to an income tax benefit on the sale of two wholly owned hotels."

- "Excluding special items, the effective income tax rate in the third quarter of 2012 was 30.8%"

- "Gross capital spending during the quarter included approximately $37 million of maintenance capital and $78 million of development capital"

- "During the quarter, the Company completed the sales of two wholly-owned hotels, the W Chicago -

Lakeshore and W Los Angeles - Westwood, for cash proceeds of approximately $244 million. These

hotels were sold subject to long-term management contracts." - In 3Q12, HOT "repurchased 1.6 million shares at a total cost of approximately $78.7 million. As of September 30, 2012, approximately $360 million remained available under the Company’s share repurchase authorization."